Blog

SpaceX IPO: Tactical Positioning Ahead of the Filing

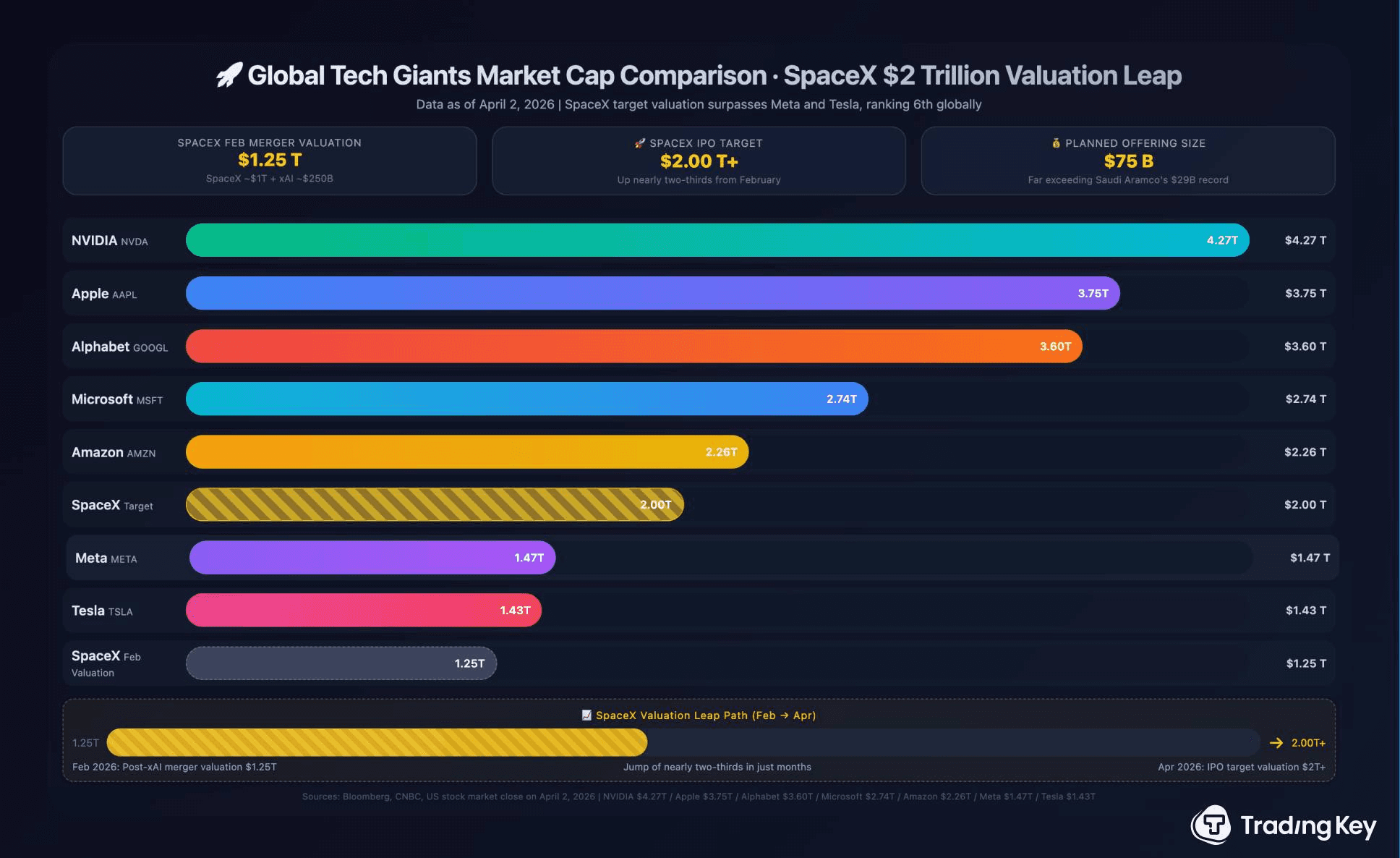

Earlier this week, SpaceX provided critical updates to its banking syndicate regarding the structure and timeline of its record-breaking IPO. While the headline figure—a projected $2.1 trillion valuation—is enough to command attention, the technical implications for institutional portfolio construction are far more profound. This is clearly shaping up to become a "Netscape Moment" for the space economy.

For those unaware, in 1995, Netscape’s IPO signaled to the world that the internet was no longer a speculative sandbox for hobbyists, but a viable, scalable, and essential layer of global commerce.

Similarly, SpaceX’s transition to the public markets in 2026 validates "Space as a Platform."

For the professional investor, this event serves as the definitive bridge between venture-style "moonshots" and institutional-grade infrastructure.

The Shift from Speculation to Sovereign Utility

The institutional appetite for this IPO is rooted in the decoupling of SpaceX’s revenue from discretionary R&D. With Starlink now accounting for an estimated 65% of the firm's enterprise value, the company has successfully transitioned to a "Sovereign Utility" model. In an environment where the Fed funds market is pricing "higher-for-longer" through 2027, SpaceX offers a rare combination:

Defensive Moats: Deeply entrenched government contracts (SDA, NASA, and the NRO).

Aggressive Growth: The commercialization of the Starship HLS (Human Landing System) and the global rollout of the Direct-to-Device (D2D) constellation.

Re-weighting the Modern Portfolio

For years, professional managers have treated space as a sub-sector of Aerospace & Defense (A&D), often buried within legacy primes like Boeing or Lockheed Martin. The SpaceX listing forces a re-weighting. We are moving toward a reality where "Space" becomes a standalone vertical in the Global Industry Classification Standard (GICS).

As the "Halo Effect" takes hold, the immediate challenge for advisors is valuation benchmarking. With SpaceX likely to command a forward EV/EBITDA multiple that dwarfs traditional A&D peers, it creates a "valuation vacuum" that will inevitably pull up the multiples of high-quality, mid-cap space infrastructure names.

Investors who recognize this "Netscape-level" shift early are not just buying a stock; they are positioning for the birth of a new asset class.

Defending the $2 Trillion Multiple

One challenge that will increasingly become apparent is the valuation bifurcation between "Space 1.0" aerospace incumbents and the high-multiple "Space 2.0" platform companies. As such, defending a $2 trillion entry point requires moving beyond sentiment and into rigorous unit economics. This valuation would make SpaceX a part of the Magnificent Eight:

To justify these historic multiples in the current environment where the Fed is remaining hawkish, we must benchmark the sector against three specific technical pillars:

The Marginal Cost of Payload: From Scarcity to Commodity

The $2 trillion valuation is not built on "launching rockets," but on the fundamental collapse of the cost per kilogram to Low Earth Orbit (LEO).

Historically, the Space Shuttle operated at roughly $54,500/kg. Falcon 9 brought that toward $2,500/kg. With Starship’s full reusability reaching operational cadence in 2026, the target is moving toward sub-$200/kg.

When the cost of access drops by 90%, the addressable market for orbital manufacturing (e.g., Varda Space) and high-bandwidth constellations expands exponentially. If a company’s business model still relies on $5,000/kg economics, they are technically obsolete, regardless of their current backlog.

The LEO "Subscription" Pivot: Starlink’s Margin Profile

Advisors must view the sector through the lens of Operating Leverage. The most valuable space assets in 2026 are those that have transitioned from "Capex-Heavy Infrastructure" to "High-Margin Utility."

We are benchmarking the Revenue-to-Constellation-Replacement Ratio. Starlink has proven that once the initial "Shell" is deployed, the marginal cost of adding a subscriber is near zero, while the replacement cost of satellites is falling due to internal manufacturing efficiencies.

Compare this to terrestrial fiber providers. Space-based D2D (Direct-to-Device) avoids the "last mile" labor costs that are currently being inflated by the sticky wage data we saw in the recent ADP and Nonfarm Payroll reports.

The "Orbital Edge" and Latency Arbitrage

Finally, a $2 trillion multiple assumes a monopoly on the most valuable "real estate" in the digital economy: the lowest-latency path for global data.

By utilizing Inter-Satellite Laser Links (ISLL), space-based networks can transmit data in the vacuum of space 47% faster than through fiber optic cables.

This creates a "Latency Alpha" for high-frequency trading and sovereign defense communications. We benchmark companies like BlackSky (BKSY) and Satellogic (SATL) on their "Latency-to-Action"—how fast they can move from capturing an orbital image to delivering an AI-processed insight to a terminal.

Identifying Alpha in the Pre-Listing "Liquidity Vacuum"

While the SpaceX listing is likely slated for June 2026, institutional capital is already navigating a significant "liquidity vacuum." Because the IPO is expected to be heavily oversubscribed (with a massive retail carve-out and sovereign wealth fund allocations) many mid-market portfolio managers risk being shut out of the initial pricing.

To hedge this risk, smart investors may initiate a tactical rotation into a "SpaceX Proxy Basket." These are publicly traded entities that share high technical and fundamental correlations with SpaceX’s core revenue drivers: launch dominance, satellite-to-cellular (D2D), and orbital infrastructure.

The Launch Vertical: Rocket Lab (RKLB)

As the only other Western entity consistently launching payloads at scale, Rocket Lab serves as the primary "scarcity play" for launch services.

Investors are laser-focused on the Neutron rocket's inaugural flight path. Neutron is designed specifically to capture the medium-lift market—the "sweet spot" for satellite constellation deployment that SpaceX’s Falcon 9 currently monopolizes.

If Neutron achieves a successful static fire or flight milestone ahead of the SpaceX IPO, expect a significant multiple expansion as RKLB is repriced from a "small-launch" provider to a "global launch" alternative.

The Direct-to-Device (D2D) Beta: AST SpaceMobile (ASTS)

Starlink’s partnership with T-Mobile has validated the "satellite-to-unmodified-phone" market. However, for investors seeking a pure-play focused entirely on this multi-trillion-dollar telecom convergence, ASTS is the high-beta proxy.

The main technical driver for this company is the commercial rollout of their BlueBird satellites later this year.

As Starlink nears its public debut, the market will look for a "comparable" to justify Starlink’s valuation. ASTS stands to benefit from this valuation "mark-to-market," as it possesses the most significant proprietary IP and spectrum filings to compete in the D2D space.

The Backdoor Equity Play: EchoStar (SATS)

For advisors requiring a more conservative, value-oriented entry, EchoStar remains a sophisticated technical play due to its balance sheet. The company also holds a historical 2% equity stake in SpaceX.

As SpaceX’s valuation moves from a private $250 billion mark to a public $2 trillion target, the "embedded value" within SATS could potentially exceed its own current market cap. Professional managers are treating SATS as a liquid, deep-value call option on the SpaceX IPO itself.

The Growth-Resilience Leader: Satellogic (SATL)

While not a direct competitor in launch, Satellogic represents the "downstream" beneficiaries of lower launch costs.

SATL’s 5-year CAGR of 42% in sales growth and its 200-day MA support make it a technical standout. Even more critically, its lower cost-to-orbit (driven by Starship) dramatically improves the IRR of Satellogic’s earth-observation constellation. It is the "software" play to SpaceX’s "hardware" revolution.

The Strategy

One winning approach to take is to use the current volatility to build "Halo" positions. If the economy remains resilient as the PMI data suggests, these proxies should catch the rising tide of the SpaceX liquidity event well before the first ticker symbol "SPACE" prints on the tape.

Automate Your SpaceX Thesis with Surmount Wealth

The "SpaceX Halo" presents a generational opportunity, but high-conviction ideas are only as good as their execution. In a market where the Fed may stay "higher for longer" and volatility is the only constant, manual trading is a liability.

Surmount Wealth provides the institutional-grade infrastructure to turn the insights from today’s blog into a systematic, rules-based reality. Whether you want to capitalize on the proxy trade or build a defensive "Sovereign Space" basket, Surmount gives you the tools to lead:

Automate Any Thesis: Use our intuitive, AI-driven strategy builder to translate complex macro views—like the correlation between SpaceX milestones and RKLB price action—into automated trades.

Pre-Built or Custom Strategies: Choose from our marketplace of professional, data-driven strategies or build a bespoke portfolio tailored to your clients' specific risk tolerances and tax needs.

Unified Account Management (No ACAT Required): Connect and manage your clients' external accounts at Fidelity, Schwab, or Goldman Private Wealth without the paperwork of a full transfer. Monitor and rebalance your entire book from a single dashboard.

Systematic Discipline: Remove the emotional friction of 24/7 markets. Our platform monitors your rules-based strategies around the clock, executing rebalances, stop-losses, and entries with surgical precision.

Stop Watching the Opportunity—Capture It.

The SpaceX IPO won't wait for your manual orders. Modernize your practice and deliver the software-driven experience your professional clients expect.

[Book a Demo with Surmount Wealth Now] and see how we help you scale personalized, automated wealth management in a fraction of the time.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.