Blog

Tax drag is the silent portfolio killer that most advisors aren't addressing aggressively enough. While investment managers obsess over finding the next 50 basis points of return through security selection, they're leaving 100+ basis points on the table by ignoring tax optimization. The difference? Tax alpha is predictable, measurable, and achievable—even in bull markets.

For RIAs looking to scale their practice while delivering measurable value, automated tax-loss harvesting (TLH) isn't just a nice-to-have feature anymore. It's become table stakes. Here's why the numbers matter and how automation transforms this strategy from a year-end scramble into a daily competitive advantage.

The Tax Alpha Opportunity: Quantifying Real Outperformance

Let's start with what matters most: the actual numbers. Academic research and industry data consistently show that systematic tax management can add 1-2% in after-tax excess returns for equity portfolios annually. This metric—known as tax alpha—represents the difference between a portfolio's after-tax return versus its benchmark.

Recent studies paint an even more compelling picture:

Vanguard research found TLH alpha ranging between 0.47% and 1.27% depending on investor profile and implementation

AllianceBernstein's analysis showed automated tax management adding more than 90 basis points to after-tax returns in fixed income portfolios during certain years

BNY Mellon's S&P 500 TME strategy delivered 0.7% annualized tax alpha over 10 years—translating to $2 million additional wealth on a $10 million portfolio

The key insight? These aren't hypothetical returns. They're measurable, attributable, and defensible when explaining your value proposition to clients and prospects.

Daily Automated TLH vs. Manual Harvesting: The Frequency Advantage

Here's where automation creates separation. Traditional manual tax-loss harvesting—checking portfolios quarterly or, worse, only in December—misses the majority of opportunities that market volatility creates throughout the year.

The Math Behind Daily Monitoring

J.P. Morgan's analysis comparing daily versus monthly monitoring found that daily reviews provided approximately 30 basis points of additional annualized tax savings compared to monthly approaches. Consider what this means:

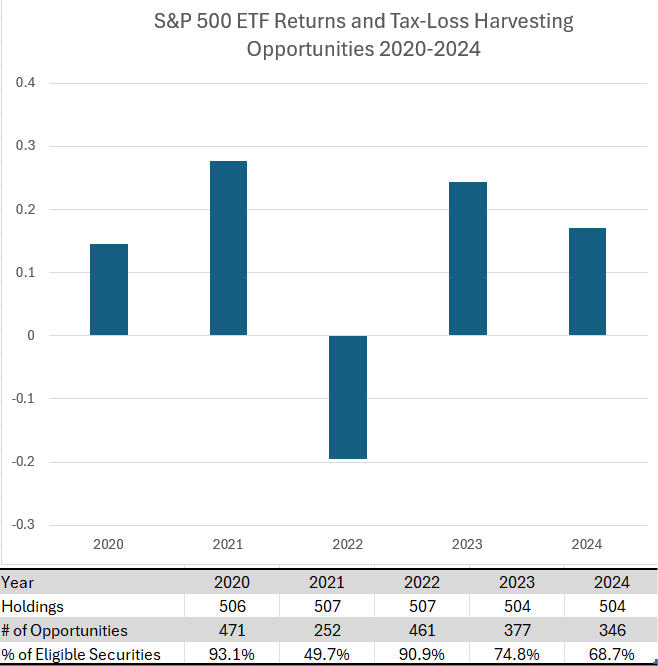

2023 example: The S&P 500 gained 26% for the year, yet 22% of stocks finished down 5% or more

Intra-year volatility: On a daily basis, 72% of S&P 500 stocks were down 5% or more at some point during 2023

Manual approaches simply can't capture these fleeting opportunities. By the time December rolls around, many losses have reversed. Municipal bond yields rarely peak in December—representing only 8% of peak months over the past 23 years—yet that's when most advisors look for harvesting opportunities.

Why Automation Matters Beyond Frequency

Daily monitoring is just the start. Automated platforms excel at:

Wash sale prevention: Tracking the 30-day window across all client accounts, including spousal accounts and IRAs

Real-time pricing: Using start-of-day pricing rather than stale end-of-day data

Trade optimization: Executing only when tax benefit exceeds transaction costs and tracking error

Scalability: Managing hundreds of client portfolios simultaneously without increasing overhead

AI-powered systems can identify up to 95% more opportunities than manual methods while maintaining IRS compliance automatically.

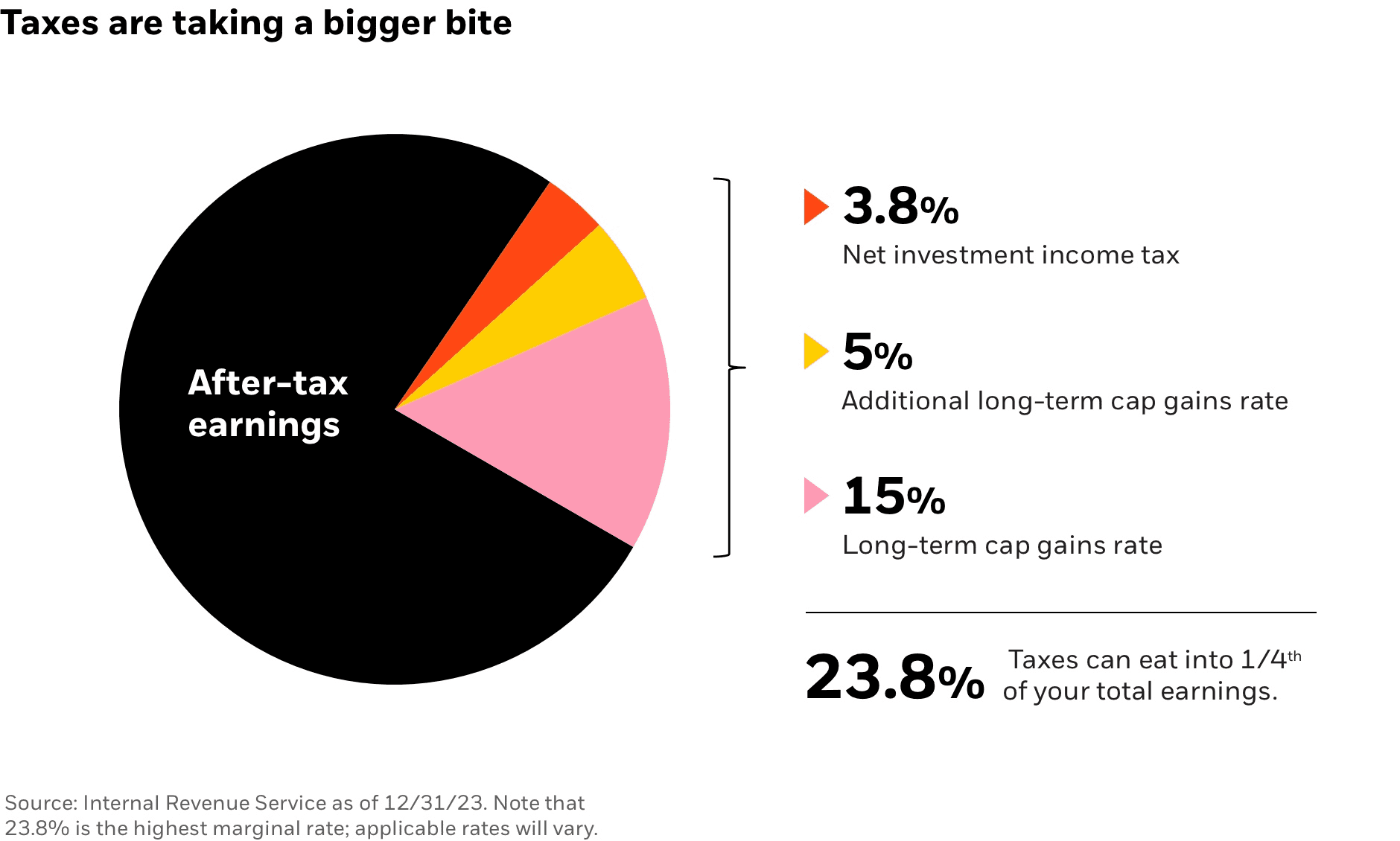

Regulatory Compliance: Navigating the Wash Sale Rule

The IRS wash sale rule is deceptively simple in concept but treacherous in execution. The rule prevents claiming tax losses if you purchase the same or substantially identical security within 30 days before or after the sale.

Key compliance considerations for automated systems:

The 61-Day Window

The wash sale rule creates a 61-day period (30 days before + day of sale + 30 days after) where purchasing substantially identical securities disallows the loss. This applies across:

All taxable accounts

Retirement accounts (IRAs, 401(k)s)

Spousal accounts

Different brokerages

The "Substantially Identical" Gray Area

What counts as substantially identical? The IRS has no clear definition, leaving room for interpretation:

Same stock = definitely identical

Different share classes of same company = often identical

Different ETFs tracking similar indexes = usually not identical

Active funds from different managers = typically not identical

Parametric uses trigger-based rather than calendar-based harvesting, executing trades only when they provide measurable benefit above transaction costs while monitoring tracking error continuously.

Consequences of Violations

Violating the wash sale rule doesn't eliminate the tax benefit entirely—it defers it. The disallowed loss gets added to the cost basis of the replacement security, effectively postponing the tax benefit until that security is sold. However, if the replacement is purchased in an IRA, the loss is permanently forfeited—a costly mistake.

Notable enforcement: The SEC fined Wealthfront $250,000 in 2018 when wash sales occurred in 31% of client accounts despite advertising their program would prevent them. Proper automation isn't optional—it's a compliance necessity.

Real Case Study: $250,000 in Losses Harvested in a Volatile Year

Theory is useful, but actual implementation reveals the true power of systematic tax management. O'Shaughnessy Asset Management documented a compelling case study from 2020—an ideal year for tax-managed strategies due to extreme volatility.

The Setup

Account size: $1,000,000 US Large Cap Direct Index portfolio

Market environment: S&P 500 up +5.4% early 2020, crashed to -31.1% in March, rallied to close +20.8%

Strategy: Continuous monitoring and opportunistic harvesting

The Results

Over the course of 2020, 22 opportunistic trades generated $254,208 in realized losses—representing 25% of the portfolio value. For a high-tax-bracket investor with equivalent short-term gains elsewhere, this translated to over $100,000 in tax savings in a single year.

Critical finding: The bulk of harvesting occurred approaching the March low. An advisor using a year-end-only approach would have captured $0 in losses, as the market finished strongly positive. Even quarterly harvesting would have yielded only $80,000 to $202,000—significantly less than the continuous approach.

Dollar Impact Across Tax Scenarios

Let's translate these percentages into actual wealth preservation:

$1 million portfolio scenario:

Conservative 0.5% annual tax alpha = $5,000/year in tax savings

Moderate 1.0% annual tax alpha = $10,000/year in tax savings

Aggressive 1.5% annual tax alpha = $15,000/year in tax savings

Over 10 years with reinvestment and compounding, even 0.7% annualized tax alpha creates $2 million in additional wealth on a $10 million starting portfolio.

Tax Alpha Calculator: Building Your Business Case

For RIAs evaluating platforms, understanding the ROI requires personalization. Here's a framework for calculating expected tax alpha for your client base:

Key Variables That Drive Tax Alpha

Client profile factors:

Tax bracket: Higher marginal rates = greater benefit

Capital gains profile: Short-term gains (taxed as ordinary income) create more value than long-term

Contribution patterns: Regular contributions maintain harvesting opportunities as new shares provide fresh tax lots

Account size: Larger portfolios can harvest more losses in absolute dollars

Implementation factors:

Monitoring frequency: Daily > Monthly > Quarterly > Annual

Direct indexing vs. ETFs: Individual securities provide exponentially more harvesting opportunities

Reinvestment: Tax savings reinvested in the portfolio compound over time

Simple ROI Formula

Example calculation: Client: $5M portfolio, 37% federal + 13.3% CA state tax rate, active trading generating short-term gains

Tax Alpha = 1.0% × 1.3 × 1.2 = 1.56% = $78,000 annual value

If your platform fee is 0.35%, the net value delivered is still 1.21% or $60,500 annually. That's a compelling business case.

Platform Cost Justification

At scale, automation pays for itself rapidly:

100 clients × $2M average AUM = $200M AUM

1% average tax alpha = $2M annual client value

Platform cost at 0.10% = $200K

Net client value delivered: $1.8M annually

This measurable ROI differentiates your practice and justifies premium fees.

Why Surmount Wealth Delivers Superior Tax Alpha for RIAs

Scale and personalization historically existed in tension—until now. Surmount Wealth's platform enables RIAs to deliver institutional-grade tax management to every client without exponentially increasing operational burden.

Built for Modern Advisory Practices

Automated daily monitoring across all client portfolios identifies tax-loss harvesting opportunities in real-time without manual review.

AI-powered portfolio construction through Vyser creates custom models and tax-loss harvesting strategies tailored to each client's unique tax situation, goals, and constraints.

Unified client dashboard aggregates AUM across custodians, providing complete visibility into tax optimization opportunities whether accounts are held at Schwab, Fidelity, Interactive Brokers, or elsewhere.

Tax-aware rebalancing automatically incorporates harvesting opportunities during portfolio rebalancing, capturing losses while maintaining target allocations.

Compliance Built In

Wash sale monitoring across all accounts—including external holdings—ensures IRS compliance automatically. The platform tracks the full 61-day window and prevents violations that could trigger penalties or audit risk.

The Competitive Advantage

In a commoditized market where investment returns have converged, tax alpha provides defensible differentiation. Cerulli Associates research found that customized tax management is no longer optional but expected by wealth management clients.

Surmount positions your practice to meet this expectation at scale, enabling personalized portfolios for every client while maintaining the operational efficiency required for growth.

The Bottom Line: Tax Alpha is the Last Free Lunch

Market returns are largely outside your control. Fees compress annually. But tax alpha? It's a reliable source of measurable outperformance that you can deliver consistently.

The data is clear:

100+ basis points of annual tax alpha is achievable with proper implementation

Daily automation captures 30+ bps more than periodic manual approaches

Compliance automation eliminates wash sale violations and audit risk

Measured ROI provides concrete justification for platform costs

For RIAs serious about scaling while delivering personalized, high-value service, automated tax-loss harvesting isn't just another feature—it's the foundation of a modern, competitive practice.

The question isn't whether tax alpha matters. It's whether your platform enables you to capture it systematically across your entire client base.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.