Blog

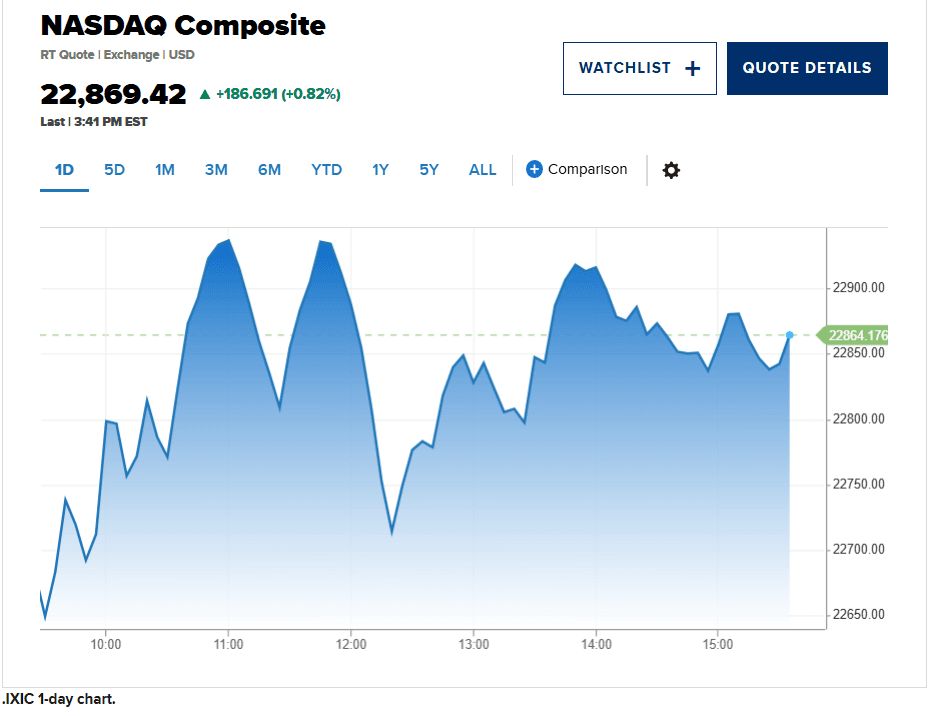

Friday’s landmark 6-3 Supreme Court ruling striking down the Trump Administration’s "Liberation Day" tariffs marks a significant turning point in the ongoing trade and investment narrative. The markets are responding positively to the news with a sigh of relief, with the S&P 500 jumping approximately 0.4% to 0.6%, while the Nasdaq Composite outperforming with a 1.1% jump, buoyed by tech hardware and semiconductor firms sensitive to import costs.

By ruling that the International Emergency Economic Powers Act (IEEPA) does not grant the Executive Branch unilateral authority to impose broad import levies, the Court has effectively dismantled the cornerstone of the current administration’s trade policy.

For portfolio managers and institutional allocators, this provides a rare moment of "forced" clarity. While the S&P 500 saw a modest relief rally and the dollar index dipped 0.2%, the long-term outlook remains clouded by the White House's immediate vow to pivot to alternative statutory tools.

President Trump has already signaled an intent to invoke Section 122 (Balance-of-Payments) and Section 301 (Unfair Trade Practices) to maintain the tariff regime, ordering a 10% global tariff to replace the duties struck down by US Supreme Court.

From Policy-Driven Relief to Structural Inflation

While the removal of broad-based tariffs typically suggests a disinflationary tailwind, the current macro environment is more nuanced. For portfolio managers and investment advisors, the 2026 SCOTUS ruling marks a transition from "policy-driven" inflation to "structurally sticky" inflation, requiring a pivot in how we model real yields and terminal rates.

1. The Fiscal-Monetary Conflict: "The Refund Stimulus"

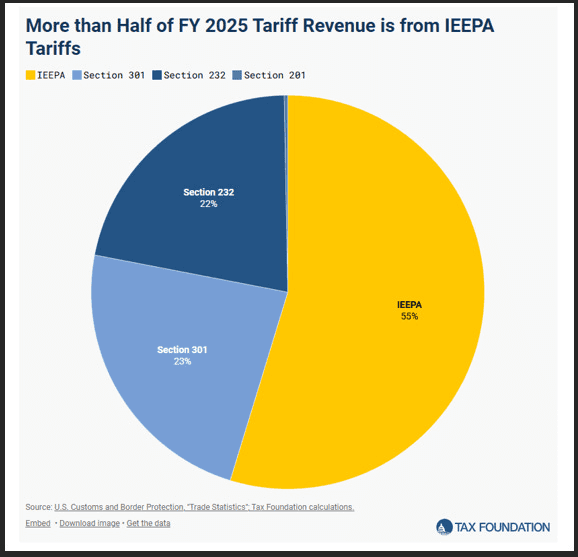

The most immediate macro risk is the $175 billion to $264 billion in unconstitutional tariff revenue that the Treasury may now be forced to refund. This is so significant because over half of the FY 2025 tariff revenue had come in from IEEPA.

For the private sector, this is effectively a massive, mid-cycle corporate tax rebate. Historically, such injections fuel capital expenditures and stock buybacks, which support equity valuations but complicate the Federal Reserve's path to 2%.

Losing $20 billion in monthly revenue forces the Treasury to increase auction sizes. This puts upward pressure on the term premium of the 10-year Treasury, potentially leading to a "bear steepener" where long-term rates rise even if the Fed attempts to cut the short end.

2. Supply Chain "Hysteresis"

In physics, hysteresis is the phenomenon where a system does not return to its original state after the force acting on it is removed. We see this in global logistics today.

Sunk Costs of Diversification: Over the last year, firms have aggressively moved production to Vietnam, Mexico, and India. The capital expenditures (CapEx) required for this "China-plus-one" strategy are permanent. Businesses will not dismantle new, higher-cost supply chains just because a specific tariff was struck down.

Pricing Power: Having survived the "Tariff Shock of 2025," many firms have discovered they possess more pricing power than previously modeled. Expect companies to defend their margins rather than passing on "tariff savings" to consumers, making core inflation more resistant to downward shifts.

3. The "Shadow Tariff" Regime

From a macro-strategic perspective, the ruling creates a policy vacuum that the administration is already filling with less transparent tools.

Section 122 & 301 Pivots: By shifting to Section 122 (emergency surcharges), the administration maintains a 10% "floor" on imports. This creates a "rolling uncertainty" premium. For investors, this means volatility remains high as trade policy moves from broad, predictable mandates to localized, unpredictable executive actions.

Sector-Specific Divergence: While the IEEPA ruling aids consumer discretionaries (toys, electronics), the continued use of Section 232 for steel and semiconductors means the "Old Economy" industrials will still face high input costs.

4. Real Interest Rates and the "Neutral" Rate

The persistence of inflation despite the ruling suggests that the neutral rate of interest may be higher than pre-2025 levels.

Deglobalization is Inflationary: The long-term trend of "reshoring" is structurally more expensive than the era of peak globalization. If the "disinflationary impulse" of the SCOTUS ruling is offset by the "inflationary impulse" of fiscal deficits and supply chain fragmentation, real rates will likely remain "higher for longer."

Portfolio Implication: Advisors should remain wary of duration risk. The "SCOTUS bounce" in small caps and retailers may be short-lived if the bond market begins pricing in a more hawkish Fed reacting to the "Refund Stimulus."

Navigating Post-IEEPA Market Volatility

As the administration shifts towards its "Plan B" (Section 122 and 301 tariffs), the macro environment will essentially move from a deterministic trade-war model to a probabilistic legal-volatility model.

For portfolio managers and investment advisors, risk management must now account for a "jagged" disinflationary path. Below is the recommended guidance for navigating this transition:

1. Liquidity & Cash Management: The "Refund" Factor

The most significant operational risk is the sudden injection of $175B–$264B back into corporate balance sheets.

Guidance: Increase monitoring of cash-rich importers (Retail, Autos, Footwear). These firms may transition from "survival mode" to "expansion/buyback mode."

Action: Review credit limits for mid-sized importers. Fintech underwriting models that previously penalized these firms for "landed cost volatility" should be recalibrated to reflect improved cash flows.

2. Duration Risk: The Deficit "Bear Steepener"

Removing the IEEPA tariffs creates a massive revenue hole for the Treasury (approx. $20B/month).

Guidance: Prepare for a "bear steepening" of the yield curve. The loss of tariff revenue implies higher Treasury issuance to fund the deficit, which puts upward pressure on long-term yields.

Action: Maintain a short-to-neutral duration posture in fixed income. Do not chase the "relief rally" in bonds, as the fiscal deficit and the potential for a "Refund Stimulus" may keep the Fed from cutting rates as aggressively as the headline ruling suggests.

3. Policy "Whack-a-Mole" & Hedges

The administration’s pivot to Section 122 (the 10% "Balance of Payments" surcharge) means the "Tariff Zero" scenario is unlikely.

Guidance: Treat the SCOTUS ruling as a change in legal authority, not a change in protectionist intent.

Action: Maintain hedges in Precious Metals (Silver/Gold). Silver's 5.7% jump on the day of the ruling suggests it is being used as a hedge against the "Refund Stimulus" inflation and continued dollar volatility.

4. Sector-Specific Recalibration

The impact of the ruling is highly asymmetric. PMs should rotate based on "Land Cost Sensitivity."

The "Landed Cost" Winners: Overweight Retailers (XRT) and Home Improvement (LOW/HD), which face the highest direct relief from the removal of 25% IEEPA duties.

The "Infrastructure" Anchor: Maintain exposure to AI-linked Capex (Alphabet, Meta, Amazon). These firms are currently projected to spend $400B+ in 2026 on data centers; their growth is decoupled from trade law and provides a "beta" anchor against trade-war volatility.

5. Currency & FX Exposure

The U.S. Dollar (DXY) has seen immediate downward pressure as the "Tariff Premium" evaporates.

Guidance: Watch for a rebound in Emerging Market FX, specifically the MXN and CAD, which were disproportionately hit by the IEEPA "Emergency" declarations.

Action: Consider "Long EM / Short USD" tactical plays. If the SCOTUS ruling stabilizes trade relations with CUSMA partners (Mexico/Canada), the risk-on sentiment will favor these "nearshoring" proxies.

Takeaway

To navigate this complex, evolving landscape, portfolio managers and investment advisors should consider integrating automated strategies that can adapt in real time to policy shifts, tariff pivots, and liquidity fluctuations. Automated approaches allow for rapid recalibration across sectors, duration, and FX exposures, ensuring that portfolios remain aligned with both immediate relief rallies and the ongoing structural risks.

Book a demo with Surmount Wealth today to see how our automated tools can help your team respond quickly, hedge effectively, and capture opportunities in the post-IEEPA tariff environment.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.