Blog

For many years, the standard playbook for diversifying a 60/40 portfolio involved a 5% "sleeve" of commodities. Most advisors fulfilled this via broad-based indices like the BCOM or GSCI. However, treating commodities as a monolithic block is a fundamental misunderstanding of the underlying drivers of the space.

In fact, recent trends indicate that sector-level dispersion is fundamentally reshaping the "commodity sleeve" from a passive diversifier into a tactical requirement.

In equities, a "rising tide lifts all boats" (beta). In commodities, there is no such tide. Commodities are fundamentally heterogeneous, and for the sophisticated RIA, understanding this distinction is the difference between a hedge that works and a drag on performance.

The Myth of Synchronized Returns

A common mistake investors make is treating commodities as if they behave like equities, where broad macro forces move most assets in tandem. In equities, valuation multiples compress or expand together because companies share exposure to interest rates, liquidity conditions, and the equity risk premium.

Commodities operate differently. They are not cash-flow-producing assets. They are physical goods, each governed by its own production cycle, inventory levels, and end-market demand.

Above all, each commodity market is effectively its own ecosystem:

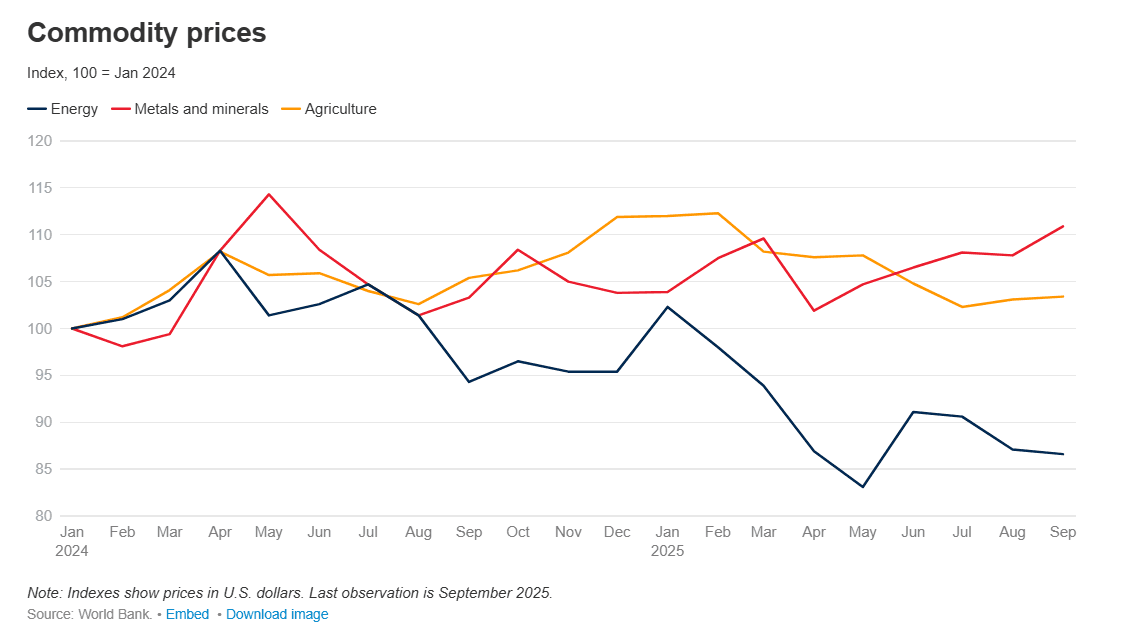

Energy markets respond to geopolitical disruptions, production quotas from OPEC+, U.S. shale output, and refinery capacity constraints. A pipeline disruption or a coordinated output cut can move oil sharply even if the rest of the commodity complex is flat.

Agricultural commodities such as grains are influenced by weather cycles like La Niña, soil conditions, fertilizer input costs, and export policies. A drought in Brazil or fertilizer shortages in Europe can tighten supply even when energy prices are declining.

Industrial metals such as copper and aluminum are heavily exposed to Chinese infrastructure stimulus, property activity, and long-term structural demand from electrification and EV adoption. Policy decisions in Beijing can create bull markets in metals while agriculture remains weak.

These forces are often unrelated and sometimes even contradictory.

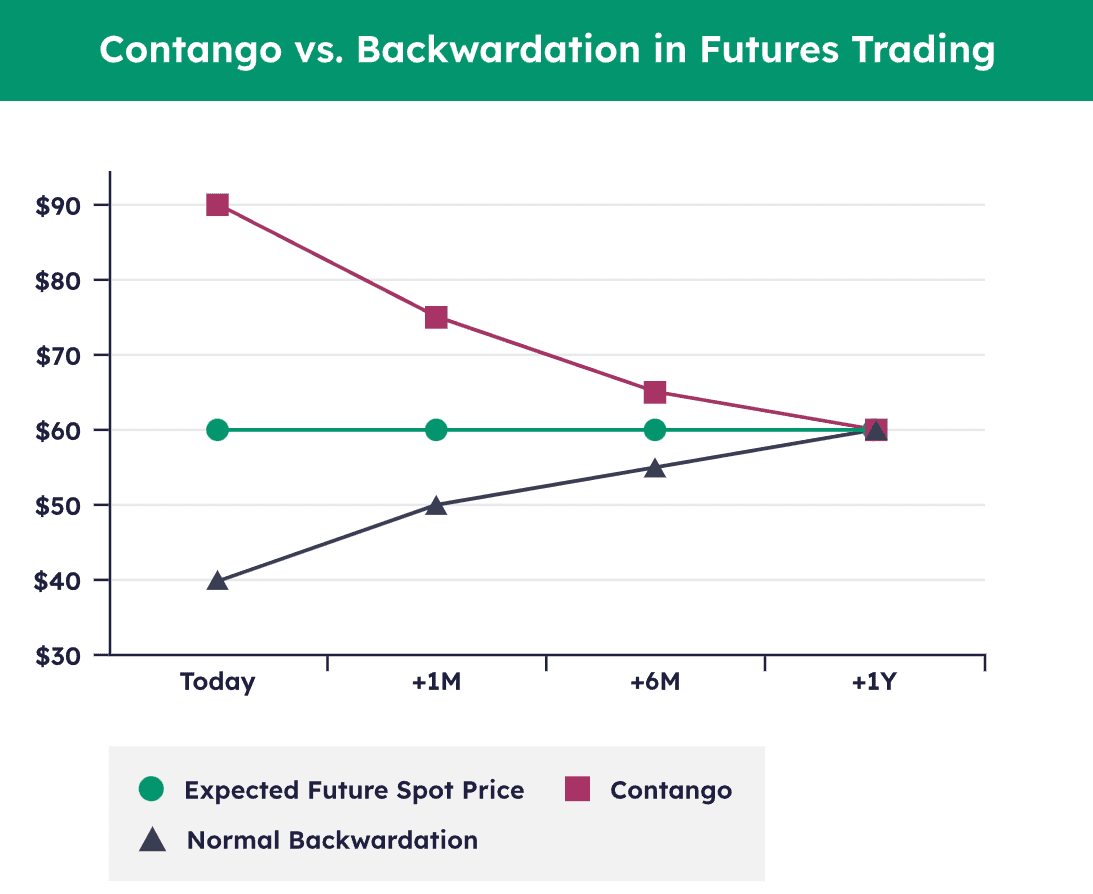

The Nuance of "Curve Carry" (Roll Yield)

When investing in commodities through futures, returns are not driven only by whether oil, gold, or copper goes up or down. A large part of performance often comes from the shape of the futures curve.

For portfolio builders, this is critical. You are not just buying “the commodity.” You are buying a contract that expires and must be rolled forward repeatedly. The economics of that roll can either help or hurt you.

Each commodity has a term structure, meaning prices for delivery at different future dates.

Backwardation

Backwardation occurs when near-term prices are higher than longer-dated futures prices.

Example: Spot copper = $4.20

3-month copper futures = $4.05

When the contract nears expiration, the futures price typically converges upward toward the spot price. If you hold and roll contracts in this environment, you can benefit from this convergence.

This positive roll return is called “carry” or “roll yield.”

Backwardation often reflects:

Tight supply conditions

Strong immediate demand

Inventory shortages

For investors, this environment can generate returns even if spot prices remain relatively stable.

Contango

Contango occurs when longer-dated futures are priced higher than the spot commodity.

Example: Spot gold = $2,000

3-month gold futures = $2,040

As the contract approaches expiration, the futures price typically drifts down toward spot. When rolling into the next contract, you are effectively selling lower and buying higher.

This creates a negative roll yield, sometimes described as a storage or financing cost.

Contango is common when:

Supply is ample

Storage costs are significant

Interest rates are elevated

In this case, even if the spot commodity is flat, the investor can lose money over time purely from rolling contracts.

Why This Matters More Than Spot Prices

Many investors focus on headlines like “Oil is up 15%” or “Gold is flat this year.”

But in futures-based investing, total return = spot return + roll yield + collateral return.

It is entirely possible for:

A flat commodity in backwardation to produce positive returns

A rising commodity in steep contango to generate disappointing ETF performance

This is why two commodity funds tracking the “same” sector can produce meaningfully different outcomes.

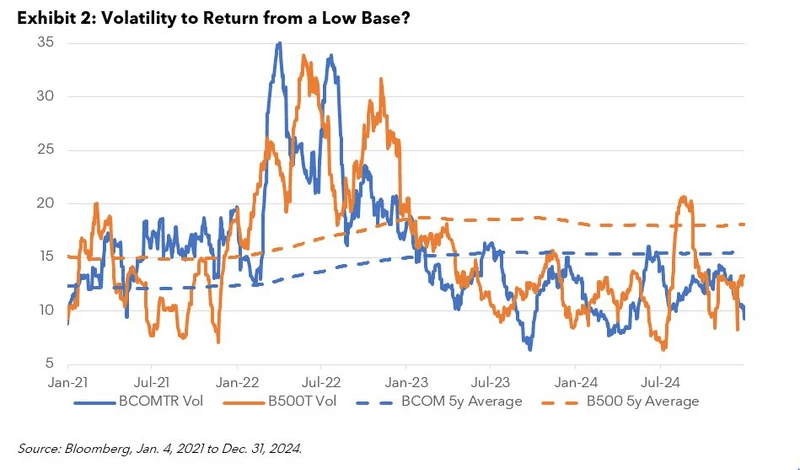

Volatility Management

For an investment advisor, the challenge is not whether commodities are volatile. They are. The challenge is how to structure that volatility so it works for the portfolio instead of against it.

A single commodity, whether gold, oil, or copper, can experience annualized volatility meaningfully higher than a broad equity benchmark like the S&P 500. Price swings of 20–30% above equity volatility are not unusual:

However, volatility at the component level does not translate linearly to volatility at the portfolio level.

When you combine commodities across sectors such as:

Precious metals

Industrial metals

Agriculture

Energy

you are blending assets that respond to different economic forces. Oil may rise due to geopolitical tension. Agricultural commodities may respond to weather shocks. Industrial metals move with manufacturing cycles. Precious metals react to real yields and currency stress.

Because these drivers are distinct, correlations within a diversified commodity basket are far lower than many investors assume. The result is that the standard deviation of the total sleeve is materially lower than the average volatility of its parts.

Building IRA-Ready Commodity Strategies with Precision and Purpose

In today’s macroeconomic regime—shaped by supply-side shocks, geopolitical fragmentation, and structural inflationary pressures—commodities are no longer optional but an essential component of a diversified retirement portfolio. Yet a “one size fits all” index is a blunt tool. Just as professional portfolio managers rotate across equity sectors based on structural and cyclical forces, commodity allocations in IRAs should be treated with the same level of scrutiny. Precious metals, industrial metals, energy, and even emerging alternative assets each play distinct roles in managing risk and capturing returns.

Diversification within commodities isn’t merely a defensive measure; it is the only way to access the full spectrum of the commodity risk premium. For IRA investors, this means thoughtfully blending sub-sector exposures to balance inflation protection, growth sensitivity, and cyclical positioning, while also preserving purchasing power over multi-decade horizons.

For financial advisors and RIAs looking to implement this level of precision in client portfolios, the challenge often lies not in strategy design but in operational execution—tracking multiple commodity exposures, managing futures contracts, and rebalancing systematically over time. That’s where infrastructure solutions like Surmount Wealth come into play. By providing the tools and platforms that allow advisors to build granular, diversified commodity allocations efficiently, RIAs can deliver more sophisticated, risk-aware IRA portfolios without adding operational complexity.

In short, commodities in retirement accounts should not be treated as a checkbox allocation. They require granular insight, thoughtful diversification, and the right infrastructure to turn strategy into execution. Advisors leveraging these capabilities can help clients capture the full spectrum of commodity returns while preserving stability and real purchasing power over the long term.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.