Blog

Tariff Shockwaves: How Trade Policy Impacts Investment Portfolios in 2026

On February 20, 2026, the U.S. Supreme Court struck down a major portion of President Donald Trump’s sweeping global tariffs in a 6–3 decision.

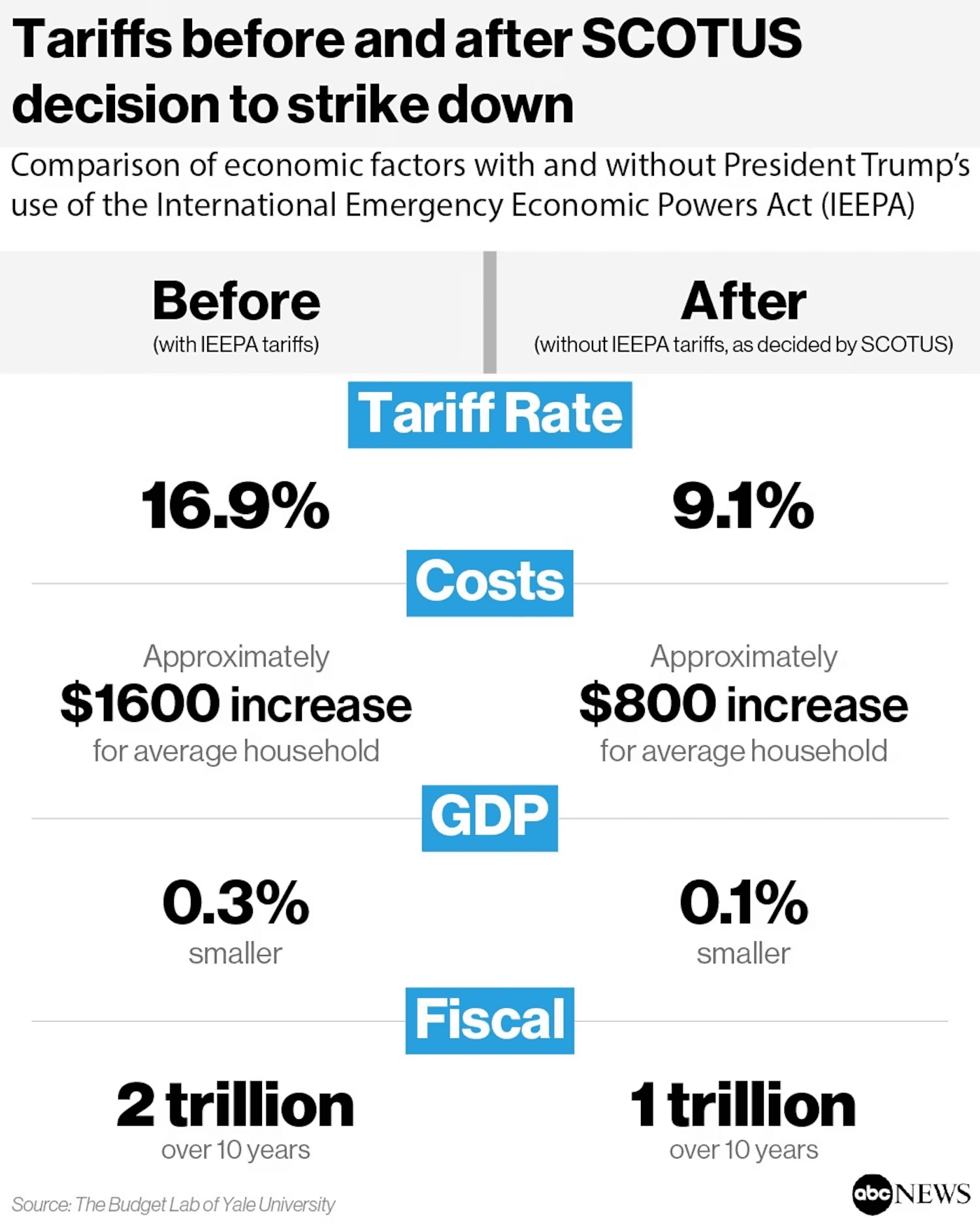

While the ruling temporarily lowered the effective tariff rate from roughly 17% to 9%, signaling a potential boost to corporate profits and consumer spending, new levies announced under a different statute are keeping the overall trade tax burden near prior levels.

For investors, this underscores a critical lesson: policy decisions can create sudden shocks in market expectations, and understanding the mechanics behind these changes is essential for positioning portfolios effectively.

However, on the other hand, the shift from IEEPA to Section 122 has created a "cliff effect" that is forcing a major rotation in investment strategies. While the Supreme Court decision provided a temporary sigh of relief for retail and tech stocks, the White House’s immediate pivot to a 15% global surcharge means the relief may be short-lived and more complex to navigate.

Tariff Investment Impact Across Markets

Trade policy does not move through the economy evenly. Its transmission mechanism cuts across asset classes, sectors, and geographies at different speeds. This is becoming increasingly evident with the recent SCOTUS ruling on tariffs.

For portfolio managers, the first step is to understand the most immediate impacts of this reversal:

1. The 150-Day "Regulatory Clock"

Unlike the previous tariffs, which were open-ended, Section 122 carries a mandatory 150-day expiration date unless Congress intervenes.

Market Impact: This has introduced a "volatility window." Analysts expect a surge in front-loading (accelerated importing) as companies race to beat the potential July 2026 expiration or a subsequent legal challenge.

Investor Strategy: Portfolios are shifting toward companies with high inventory turnover and "light" supply chains that can pivot before the 150-day window closes.

2. Sector-Specific Divergence

The new Section 122 regime is not a carbon copy of the old one. It includes strategic exemptions and overlaps that create clear "winners" and "losers":

The Protected: Most products already covered by Section 232 (Steel and Aluminum) or USMCA (Mexico/Canada) remain largely insulated from the new surcharge, making these sectors "safe havens" for trade-sensitive capital.

The Exposed: Consumer electronics and apparel—which previously benefited from country-specific "deals"—now face a flat, non-negotiable 15% floor. This is a significant blow to margin-heavy retail giants.

3. The "Refund" Tailwinds

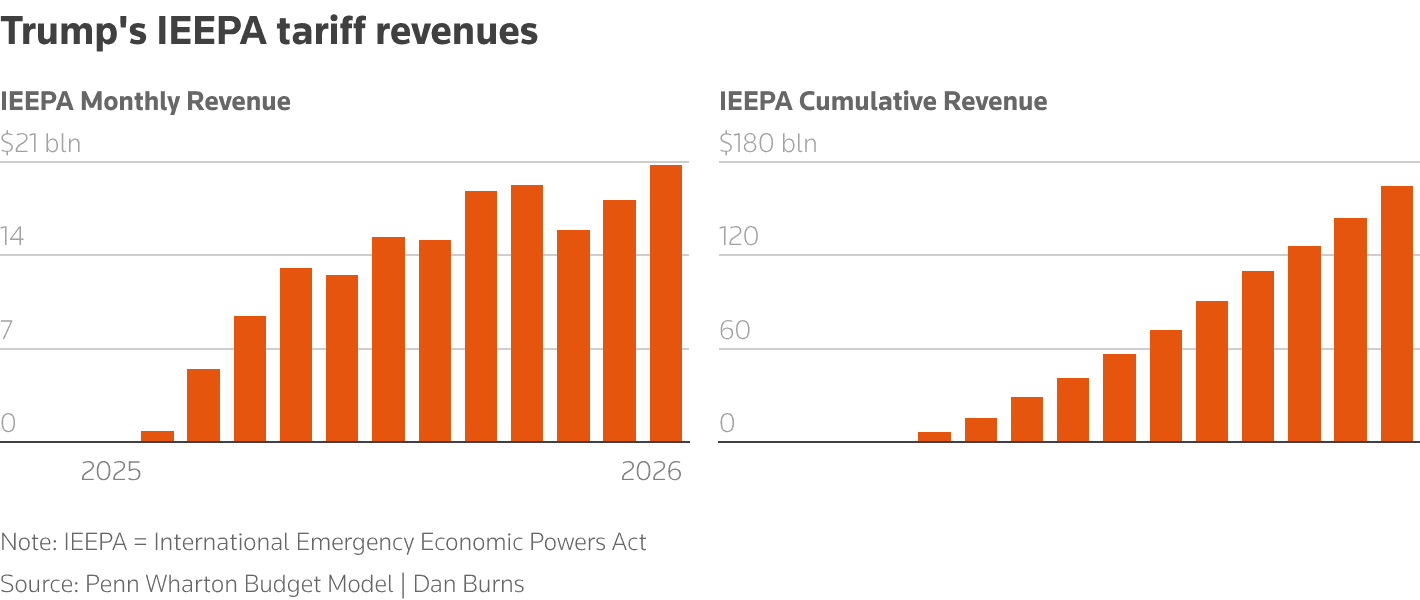

The SCOTUS ruling didn't just stop future taxes; it potentially invalidated over $175 billion in collected duties from 2025.

The Opportunity: Large-scale importers (like Walmart or Target) may soon see massive one-time cash inflows from federal refunds.

The Risk: The administration has signaled it will contest the refund process, meaning these "assets" on corporate balance sheets are currently tied up in litigation.

These shifts are resulting in a complex investment landscape that rewards granular analysis over broad macro assumptions. What appears to be a single trade policy adjustment is, in practice, a series of asynchronous shocks moving through earnings, working capital cycles, and sector leadership.

Macroeconomic Ripple Effects of Tariffs

According to the Budget Lab at Yale, the Supreme Court ruling reduced but did not eliminate the macro drag from tariffs, and that the ultimate economic impact hinges on whether the new Section 122 tariffs expire or become permanent.

As already mentioned above, before the ruling, the effective tariff rate was about 16%, the highest since the 1930s. After the Court struck down IEEPA-based tariffs, it dropped sharply to about 9%.

However, the new 15% Section 122 tariffs pushed the rate back up to 13.7%. This means that:

The legal reversal reduced the most extreme scenario

But overall trade policy remains historically restrictive

Investors should not interpret the ruling as a full normalization

If Section 122 expires, the rate falls back near 9%. If extended, the regime remains structurally tight. The overall implication is that the ruling reduced tail risk but did not remove the trade policy overhang.

In a more long-term macro sense, however the key impacts are much more nuanced:

Inflation Impact Is Smaller Than Headlines Suggest, But Persistent

According to the Budget Lab research, assuming the Fed “looks through” tariffs:

If Section 122 expires: price levels rise about 0.5%–0.6%

If extended: price levels rise about 0.8%–1.0%

That translates to a $600–$800 annual real income hit per household under expiration, or $1,000–$1,300 if extended.

So while the inflation shock is not catastrophic, it is meaningful and regressive.

Implication: Tariffs add modest but sticky inflation pressure, complicating rate-cut narratives.

Growth Drag Is Real but Not Recessionary

The research suggests:

Unemployment rises about 0.3 percentage points by end-2026

Long-run GDP is 0.1%–0.2% smaller

Near-term fiscal refunds from repealed IEEPA tariffs partially offset 2026 damage

In other words:

This is a slow bleed, not a collapse

Growth is shaved, not shattered

The bigger impact is structural reallocation, not cyclical contraction

Implication: Trade policy contributes to a mid-cycle slowdown dynamic rather than triggering a downturn.

The Real Story Is Sector Reallocation

Tariffs create winners and losers domestically:

Manufacturing output rises roughly 2%

Construction falls 2%–3%

Mining and agriculture decline modestly

Services absorb part of the crowd-out effect

The net result is that the economy shrinks slightly overall, but capital shifts toward protected sectors.

Implication: Equity allocation matters more than aggregate exposure. Sector selection becomes critical.

Revenue Gains Are Large but Growth Offsets Them

Over 10 years:

~$1.1 trillion in dynamic revenue if Section 122 expires

~$1.9 trillion if extended

However, slower growth partially offsets the gross revenue gains.

This highlights a key policy tradeoff, which is that tariffs function as a significant fiscal tool, but at a measurable growth cost.

Distributional Effects Are Regressive

Lower-income households bear a larger burden relative to income:

Bottom decile burden is roughly 3x the top decile as a share of income

This increases political sensitivity and policy instability

Implication: Political pressure to modify tariffs likely increases over time, raising policy volatility risk.

Overall, while the risks of a recession may be overblown, there is definitely persistent margin pressure, mild inflation friction, sector dispersion, and policy volatility premia to deal with.

Strategic Portfolio Responses to Trade Policy

Right now, we aren’t faced with a crisis environment, but instead are dealing with a persistent policy-friction regime marked by modest inflation pressure, mild growth drag, sector dispersion, and elevated policy volatility.

As such, the current environment seems to favour quality equities with durable margins and strong balance sheets with minimal debt. In addition to that, firms with domestic revenue exposure and pricing power, as well as businesses less reliant on import-heavy supply chains could stand to win disproportionately.

Similarly, it is important to keep in mind that tariffs are redistributive, at their very core. Long-run modelling indicates that:

Manufacturing modestly benefits

Construction and mining contract

Broader services absorb second-order effects

As such, it is important to tilt toward advanced manufacturing and domestic industrial beneficiaries, but also to be cautious on construction-sensitive segments, especially those exposed to higher input costs. Service sectors insulated from goods inflation could enjoy higher margins in the longer run.

Another way to play this dynamic could be through an increased (but selective) global allocation. Global modeling suggests:

Canada, China, and Mexico face larger long-run output hits

Some free trade partners experience marginal gains

Global GDP is slightly lower overall

For global portfolios:

Evaluate supply-chain realignment beneficiaries

Hedge currency exposure where trade balances may shift

Avoid blanket emerging market de-risking; dispersion matters

In a market shaped by tariff uncertainty, modest growth drag, and elevated policy volatility, timely adjustments across sectors, asset classes, and geographies are critical. Automated strategies can help portfolio managers and advisors respond instantly to shifting effective tariff rates, inflation signals, and earnings surprises, removing the lag that comes with manual rebalancing.

Take advantage of this environment—book a demo now with Surmount Wealth to see how automated, policy-aware strategies can keep your portfolio positioned for opportunity while managing downside risk.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.