Blog

Most client review meetings follow a predictable script: portfolio performance versus benchmark, asset allocation pie charts, account balances. The advisor walks through slides. The client nods politely. But Vanguard's 2025 Advisor's Alpha research reveals that advisors who focus on behavioral coaching, tax management, and systematic rebalancing can add approximately 3% in net returns annually—yet most review meetings emphasize what clients understand least.

As fee compression intensifies and clients grow more financially literate, review meetings must justify not just what happened, but why it mattered for this particular household. This playbook reconstructs the client review around decisions that demonstrably impacted wealth.

Start With Life Changes, Not Market Commentary

The most productive reviews begin by documenting what shifted in the client's circumstances:

Did their daughter accept a graduate school offer, creating foreseeable tuition obligations?

Did they receive an early retirement package?

Has a parent's declining health introduced potential caregiving costs?

These changes dictate whether prior portfolio positioning remains appropriate. A client approaching age 70 faces different sequence-of-returns risk than the same client at 65. Documenting life changes creates an audit trail showing portfolio decisions responded to actual circumstances rather than generic market views—the essence of fiduciary duty.

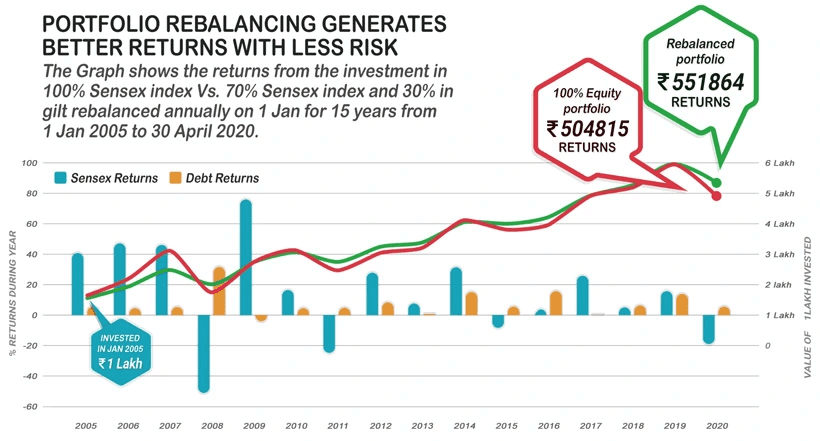

Rebalancing: Translate Discipline Into Dollar Impact

Most clients tolerate rebalancing explanations without grasping why it matters. The data that breaks through is specific dollar impact.

Present each rebalancing decision with three data points:

The triggering threshold breach

The specific action taken

The outcome versus doing nothing

Example: "Your target equity allocation was 60%. By November, growth stock appreciation pushed you to 68%. We sold 8% to restore balance at an average price of $X. Had we not rebalanced, that position would have declined by $6,000 in December's correction. The proceeds purchased small-cap value near its low, which recovered 18% in Q1."

Morningstar's 2024 Mind the Gap study found investors lost 1.1 percentage points annually—approximately 15% of total returns over a decade—due to poor timing decisions. Systematic rebalancing eliminates this behavior gap by enforcing discipline when emotions argue otherwise.

Tax-Loss Harvesting: Quantify the Deferred Asset

Tax-loss harvesting remains abstract because benefits accrue in future years. Translate paper losses into tangible value by calculating the deferred tax liability reduction.

Present harvesting with clear math:

Total losses harvested

Tax rate applied

Estimated tax asset created

Multi-year carryforward value

Example: "We harvested $22,000 in losses during August volatility. At your 32% combined rate, this created a $7,040 tax asset. We immediately reinvested in highly correlated positions, maintaining equity exposure while improving your after-tax position materially."

Research shows practices that systematically harvest losses add 0.8-1.2% annually to after-tax returns. For clients in high tax brackets approaching retirement, present a multi-year summary showing cumulative tax savings and carryforward positioning—reframing "losses" as valuable assets.

Withdrawal Sequencing: Prove Adaptive Management

For distribution-phase clients, demonstrate that withdrawal strategy adapted to market conditions rather than following rigid schedules.

Present a 12-month calendar showing:

Which asset classes funded distributions each month

The cost under mechanical pro-rata withdrawals

Dollar value preserved through tactical sequencing

Example: "When March volatility pushed equities down 8%, we drew from your stable value allocation rather than selling stocks at depressed prices. By May, when equities recovered, we replenished stable holdings by trimming appreciated positions. This dynamic sequencing preserved approximately $8,400 versus pro-rata withdrawals—your portfolio balance is $31,000 higher as a result."

This is the difference between strategic stewardship and mechanical automation. Clients understand preservation of capital in concrete dollar terms.

Performance Attribution: What Actually Drove Results

Standard benchmarking answers whether the portfolio kept pace—but doesn't explain what decisions specifically affected outcomes. CFA Institute research demonstrates over 90% of portfolio return variance comes from asset allocation decisions rather than security selection.

Present attribution clearly:

Total return versus benchmark

Breakdown by source (asset allocation, rebalancing, tactical tilts)

Acknowledge decisions that detracted from performance

Example: "Your portfolio returned 11.2% versus the 60/40 benchmark's 9.8%. Of that 1.4% outperformance: 0.9% came from disciplined rebalancing rather than chasing performance, and 0.5% came from overweighting small-cap value at historical valuation lows. Our international overweight cost 0.4% short-term, though we maintained it for long-term diversification benefits."

Transparency about trade-offs reinforces that portfolio management involves judgment, not infallible forecasting.

Goal Funding: Connect Portfolio to Life Outcomes

Investment portfolios exist to fund specific objectives. Yet most reviews present performance in isolation from goals, as if returns were the objective rather than the means.

For accumulation clients:

"Your retirement goal requires $2.8 million by age 65. Last year's performance combined with contributions increased projected balance to $3.1 million, creating a $300,000 buffer. This positions you to retire six months earlier, or maintain your timeline with reduced savings pressure."

For distribution clients:

"At your current $96,000 annual withdrawal rate, the portfolio maintains 92% probability of sustaining distributions for 30 years. Last year's performance improved this from 88%, providing additional cushion for future market stress."

Research shows clients who understand progress toward specific goals exhibit lower anxiety during volatility and higher plan persistence than those focused on relative performance metrics.

What This Framework Achieves

This reconstructed review meeting accomplishes three objectives simultaneously:

It makes value concrete. When clients understand rebalancing saved $X, tax-loss harvesting created $Y in deferred assets, and drawdown management preserved $Z during volatility, the value proposition becomes tangible rather than abstract.

It generates required documentation. Each review creates a record showing portfolio decisions served the client's specific circumstances—the essence of fiduciary compliance and SEC regulatory expectations.

It differentiates disciplined practices. In an environment where passive indexing provides low-cost market exposure, advisor value lies in behavioral coaching, tax optimization, and systematic rebalancing—precisely what this framework emphasizes.

The data clients actually care about isn't what happened to the S&P 500. It's what decisions you made on their behalf, why those decisions mattered given their circumstances, and how the portfolio moved them closer to funding the life they're building. That's the conversation worth having.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.