Blog

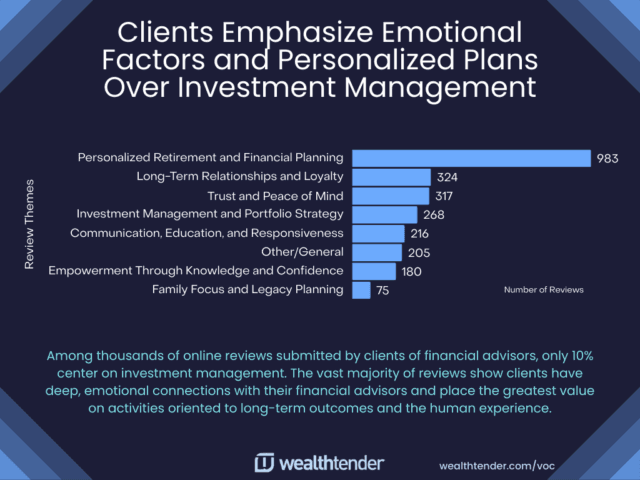

The retirement advice business is changing faster than most advisors realize. While you're focused on portfolio construction and withdrawal rates, new research from Wealthtender analyzing 2,568 client reviews found that 89% of what clients value centers on relationship quality, planning advice, and emotional factors—just 1 in 10 focus on investments or portfolio management.

That gap between what advisors emphasize and what retirees actually want creates both risk and opportunity. The advisors who close it will dominate the next decade. Those who don't will watch clients leave for competitors who figured it out.

The Data Everyone's Missing

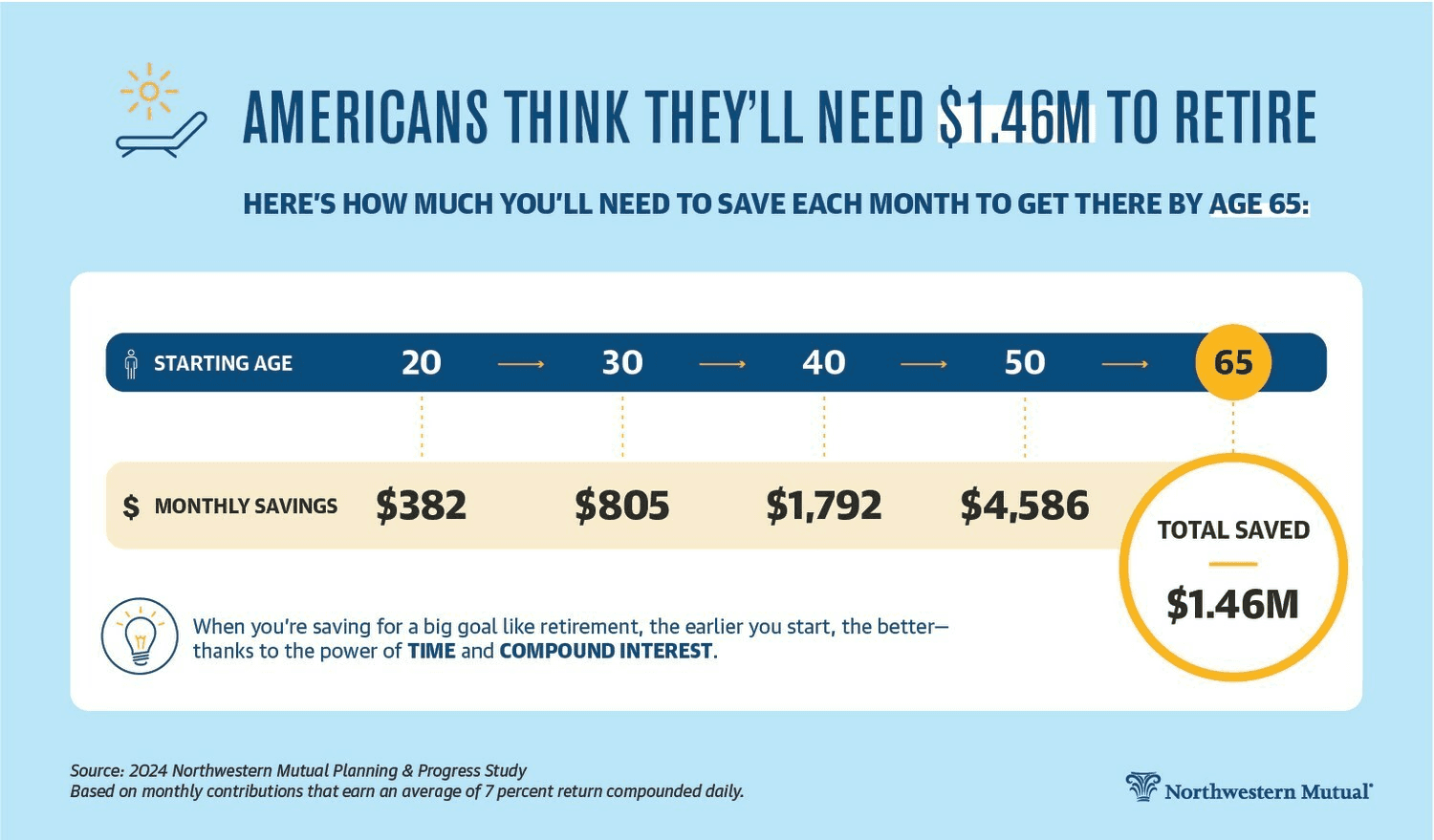

Northwestern Mutual's 2024 study revealed something striking: Americans with advisors expect to retire two years earlier than those without—at 64 versus 66. They've also saved twice as much: $132,000 versus $62,000. But here's what matters more: 75% feel financially prepared for retirement compared to just 45% without an advisor.

The difference isn't the portfolio performance. It's confidence. Peace of mind. Clarity about whether their plan will actually work. That's what retirees are buying, even if they don't articulate it that way.

What Changed in the Last Year

Healthcare cost anxiety spiked. MFS research found that average healthcare costs for retired couples now range from $351,000 to $413,000—a figure that only 36% of pre-retirees feel confident managing. Meanwhile, Social Security's 2025 COLA came in at just 2.5%, down from 3.2% in 2024, leaving retirees questioning whether they can maintain purchasing power.

This creates a specific advisor opportunity: retirees don't need generic reassurance. They need someone to run the actual numbers showing how their portfolio handles rising Medicare premiums, potential long-term care costs, and inflation that consistently outpaces Social Security adjustments.

The Five Things Retirees Actually Care About

Proactive communication before they have to ask

Wealthy clients paying premium fees expect you to identify opportunities and risks before they surface. Morningstar research confirms this: high-net-worth retirees want advisors who anticipate tax law changes, flag market shifts, and update plans without waiting for annual review meetings.

This doesn't mean bombarding clients with market commentary. It means reaching out in September when you notice their portfolio could benefit from year-end tax-loss harvesting, not in December when it's too late to act optimally.

Transparency about what they're paying and why

Research shows 56% of clients cite transparency as extremely important when choosing an advisor. Retirees specifically want to understand not just the fee percentage but what services that fee covers and what value those services deliver.

The advisors winning here use service calendars showing every action they take throughout the year—quarterly rebalancing, tax-loss harvesting, RMD optimization, estate document reviews. When clients see twelve activities performed on their behalf, the 1% fee stops feeling expensive and starts feeling justified.

Plans personalized to their actual situation

Generic advice is the top complaint. Six in ten consumers report dissatisfaction with financial advice because it's "too generic/not personalized to my situation."

For retirees, personalization means acknowledging that a 65-year-old with a pension faces different risks than a 65-year-old without one. That someone planning to relocate to Florida needs different tax planning than someone staying in California. That a client with three adult children requiring financial support operates under different constraints than one whose kids are self-sufficient.

Help beyond just investment management

Only half of advisors offer estate planning or cash flow assistance, yet retirees consistently rank these among their top concerns. J.P. Morgan research found that 60% of retirees experience spending fluctuations of 20% or more during their first three years of retirement—exactly when most advisors are still treating them like accumulation-phase clients.

Retirees want advisors who help them figure out whether they can afford to buy a second home, how to structure gifts to grandchildren without derailing their own plan, and when claiming Social Security actually makes sense given their specific health and longevity expectations.

Someone who'll be there through their entire retirement

Here's an uncomfortable reality: 46% of current financial advisors say they're within 10 years of retirement, and 26% are already 65 or older. Retirees are hiring advisors to guide them through 20-30 year retirements, only to discover their advisor might retire first.

This creates a succession planning conversation most advisors avoid. Clients want to know: who takes over if you retire? Have you identified someone? Will that person understand my situation? The advisors addressing this proactively retain clients. Those avoiding it watch clients leave to find someone with a longer runway.

The Advisor Shortage Nobody's Talking About

While demand for retirement advice surges, advisor supply is contracting. Nearly 40% of advisors will retire within the next decade, controlling an estimated $10.4 trillion in assets. Meanwhile, younger advisors aren't entering the field fast enough to replace them.

This matters for retirees because the best advisors are increasingly selective about taking new clients. Survey data shows 97% of prospective clients interview multiple advisors and 96% research them online before deciding. The power dynamic is shifting—advisors with strong reputations can afford to be choosy while retirees face more competition for limited advisor capacity.

What This Means for 2026

The advisors thriving in 2026 will be those who recognized that retirement planning isn't about beating benchmarks—it's about delivering confidence that the plan will work. That requires:

Monthly or quarterly check-ins during market volatility rather than waiting for annual reviews. When markets drop 10%, retirees want to hear from you before they panic, not after.

Tax planning integrated into every decision, not treated as a separate year-end activity. BNP Paribas research found 58% of clients now track portfolio performance more closely, with tax efficiency ranking as a top concern.

Technology that enhances service without replacing human interaction. 85% of advisors report AI benefits their practice, but retirees still want a phone call when something important happens—they just also want the convenience of accessing documents digitally.

Clear succession plans documented and discussed openly. The firms winning long-term client relationships assign junior advisors to client relationships years before the senior advisor retires, creating continuity clients can count on.

The Bottom Line

Retirees aren't hiring you to pick stocks. They're hiring you to tell them whether their plan will work, to update it when life changes, and to prevent them from making expensive mistakes when markets get scary. Research confirms advisors are Americans' most trusted source for financial advice—twice as trusted as family members and 8x more trusted than social media influencers.

That trust isn't built on performance reports. It's built on answering the phone, explaining complex decisions in plain language, proactively identifying problems before they become crises, and delivering the confidence that lets clients actually enjoy retirement instead of worrying about whether their money will last.

The data is clear: retirees who work with advisors retire earlier, save more, and feel significantly more prepared. But they're increasingly selective about which advisors they hire. The ones winning in 2026 will be those who figured out that investment management is table stakes—the real value is everything else.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.