Blog

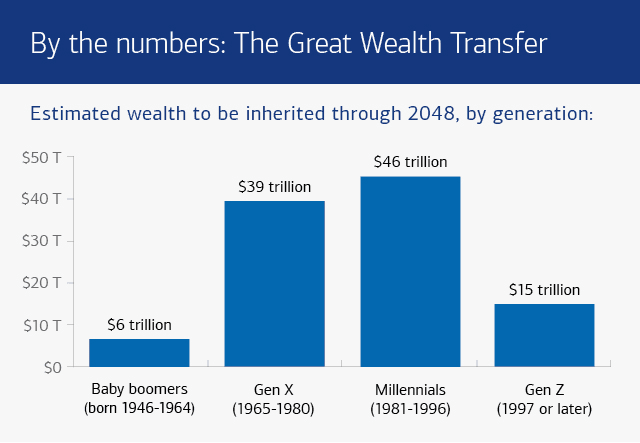

The numbers are staggering. Over $124 trillion will change hands between now and 2048 as Baby Boomers and older generations pass their wealth to heirs—the largest intergenerational transfer in history. For RIAs, this represents an unprecedented opportunity. But here's the catch: 81% of next-generation millionaires plan to fire their parents' advisors within a year or two of receiving their inheritance.

After decades of carefully managing your clients' portfolios, building trust, and delivering results, their children are statistically likely to walk away—taking trillions in AUM with them. The question isn't whether this wealth transfer will happen. It's already underway. The real question is: will your firm be positioned to capture it?

Why Younger Investors Reject Their Parents' Advisors

The data is brutally clear. Just 19% of affluent investors use the same advisor as their parents. More troubling? Over 90% of affluent investors who selected their own advisor didn't even consider their parents' advisor in the selection process.

What's driving this exodus?

Digital Deficiency

The primary reason young inheritors are abandoning their parents' advisors comes down to one word: technology. Nearly half of next-generation clients cite poor digital offerings and lack of services as their top complaints.

While Boomers are comfortable with quarterly statements and annual review meetings, Millennials and Gen Z grew up with:

Real-time portfolio updates on their smartphones

Instant communication via text and video

24/7 access to their financial data

Seamless digital experiences across all platforms

When 84% of Millennials and 82% of Gen Z consider app-based mobile banking a concrete expectation, your paper-based processes and quarterly PDF reports feel like relics from another era.

Different Investment Philosophy

Next-gen investors don't just want different technology—they want different investment strategies. 72% of Millennial and Gen Z investors believe it's no longer possible to achieve above-average returns solely with traditional stocks and bonds.

These investors are looking for:

Alternative investments: 88% of younger investors show more interest in private equity than Boomers

Cryptocurrency exposure: 47% of young investors hold cryptocurrency

ESG investing: 82% of Millennials consider a company's ESG track record when investing

Global diversification: Enhanced offshore investments in emerging wealth hubs

If your investment philosophy centers solely on the traditional 60/40 portfolio, you're already behind.

Communication Style Mismatch

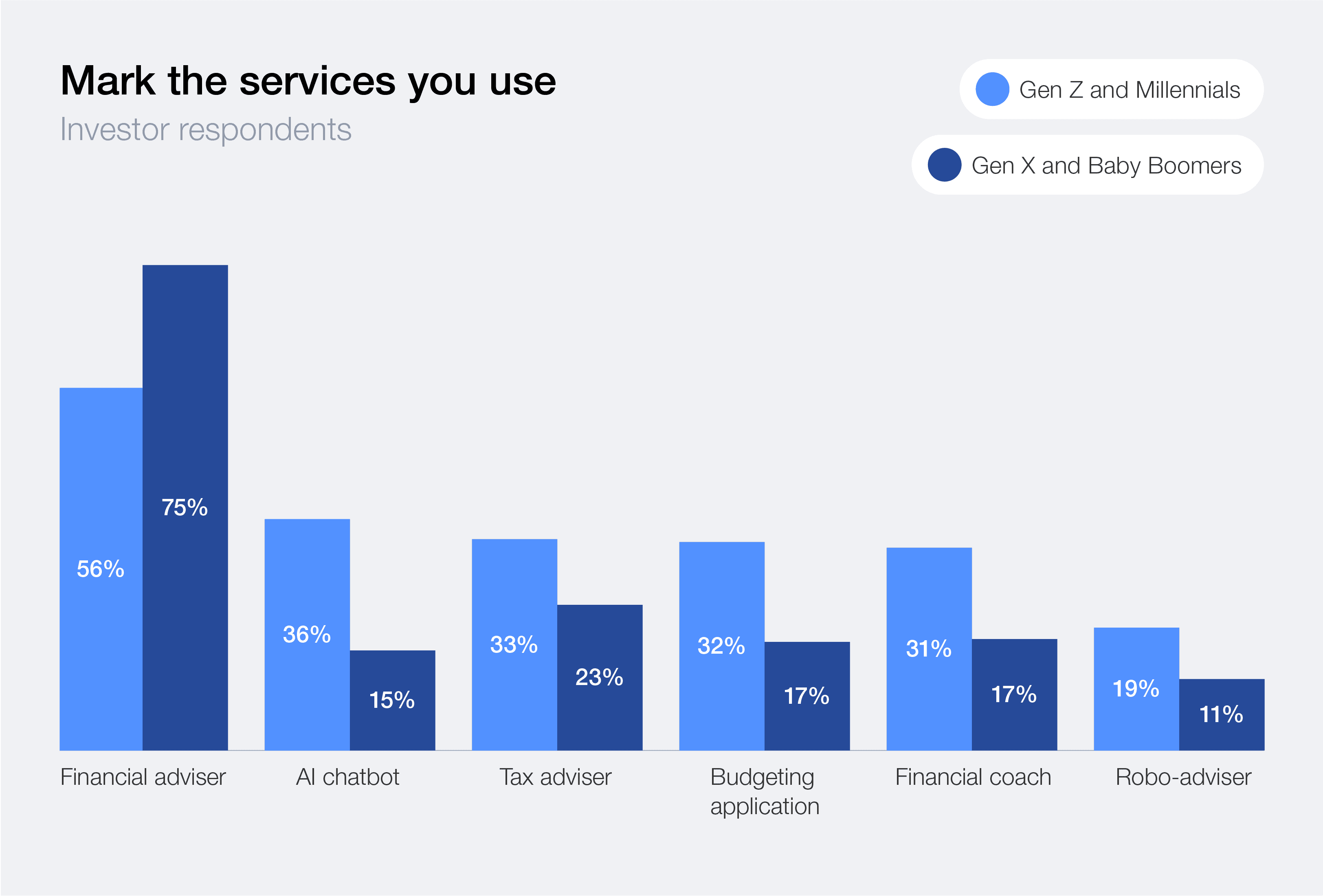

More than 70% of affluent Millennials have a secondary investment firm—they're hedging their bets and keeping their options open. Why? Often it's not about your performance; it's about how you communicate.

Younger clients want advisors who:

Understand their "why" before pitching products

Communicate through their preferred channels (text, video, app notifications)

Provide holistic life planning beyond just investment management

Demonstrate genuine interest in their unique goals and values

Traditional advisor communication—formal, scheduled, performance-focused—doesn't resonate with a generation that values authenticity and personalization.

The Digital Expectations Gap

Let's be specific about what next-gen clients expect from their digital wealth management experience:

Mobile-First, Always-On Access

65% of consumers now say the ability to do all their banking via mobile device is important—up from just 39% in 2018. Six in ten younger investors would switch financial services providers for a better mobile app experience.

Your younger clients aren't logging into desktop portals. They're checking their portfolios while standing in line for coffee, making investment decisions from their phones, and expecting instant responses to their questions.

Seamless Integration & Automation

25% of Gen Z and 22% of Millennials want digital solutions integrated with digital wallets and wearable devices. They expect:

Automatic savings and investment features

Instant fund transfers

Integration with budgeting and financial wellness apps

Real-time notifications about portfolio changes

Hybrid Advisory Models

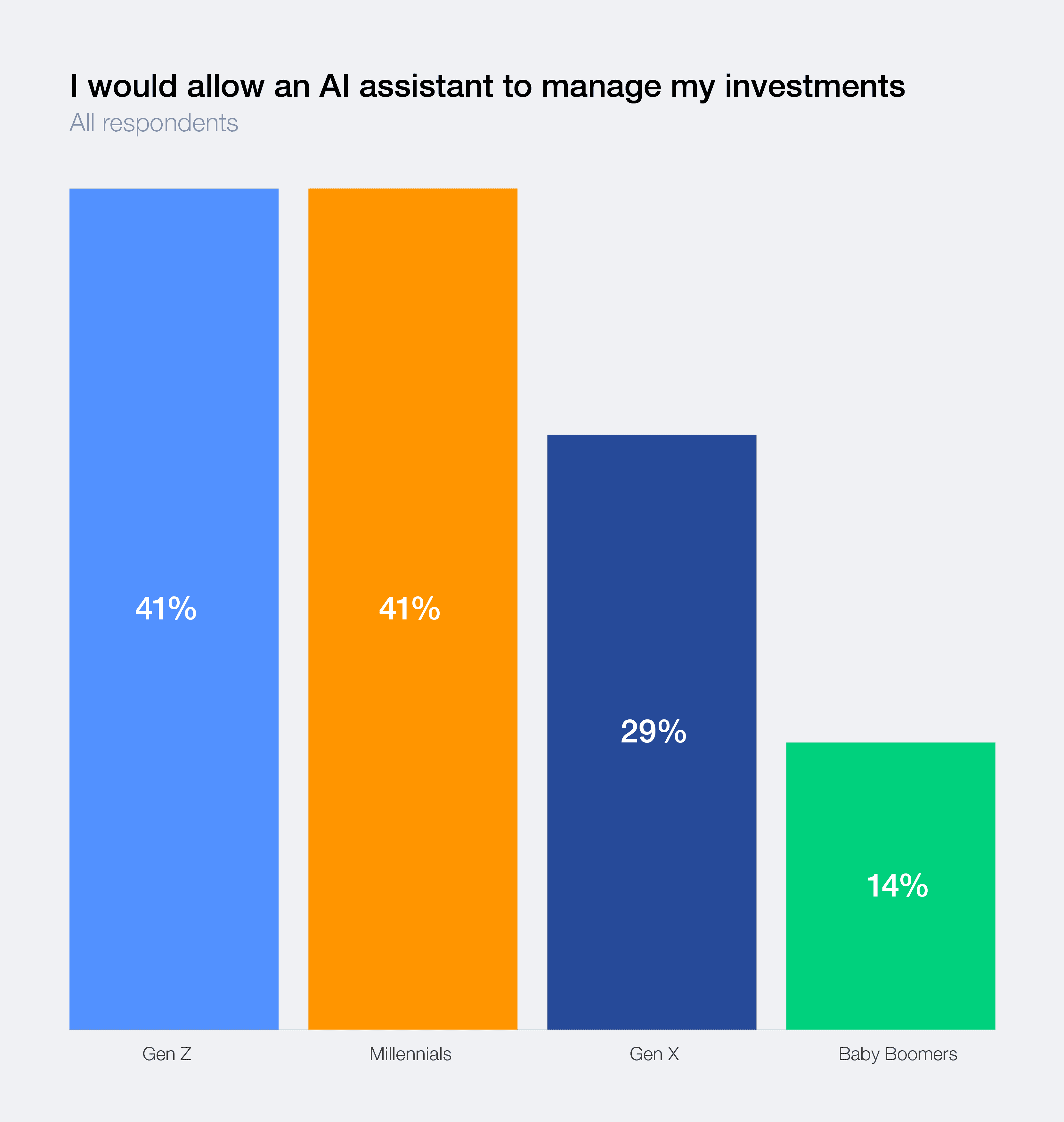

Despite their digital preferences, younger investors still value human connection—but on their terms. Nearly 65% of Millennials and Gen Z believe a financial advisor is important for financial success. However, 51% of Millennials are twice as likely as older generations to consider using a robo-advisor.

The winning formula? Tech-enabled human advice that combines:

Digital tools for routine tasks and information access

Human advisors for complex decisions and life planning

Video conferencing instead of in-person meetings only

Text and chat for quick questions

How to Serve Boomers and Their Kids Simultaneously

Here's where it gets tricky. You can't alienate your profitable Boomer clients while courting their children. The solution isn't choosing between generations—it's creating a multi-generational service model.

Start Family Meetings Now

89% of high-net-worth firms say conducting family meetings and maintaining regular communication among family members is a key best practice. But you need to start these conversations before the wealth transfer happens.

Action steps:

Invite clients' adult children to annual reviews: Make it routine, not special

Host next-gen education workshops: Offer sessions on topics relevant to younger investors (student debt management, first-time home buying, crypto basics)

Create touch points with heirs: Even small interactions build familiarity and trust

Facilitate wealth transfer conversations: Many families avoid discussing money—you can be the catalyst

The goal is relationship building, not account management. When 90% of heirs don't even consider their parents' advisor, your job is to become the exception by establishing a relationship before the inheritance.

Invest in Technology That Serves All Generations

You need a tech stack that delivers:

For Boomers: Clean, simple interfaces with optional traditional statements and phone support

For Millennials/Gen Z: Mobile apps, real-time data, integrated planning tools, and digital communication

The key is flexibility. Vanguard reports that two-thirds of users of their digital-only advisor offering are Millennials or Gen Z (average age 37), while users of their hybrid offering average age 57. Both segments exist in your client base—and increasingly within the same family.

Build a Multi-Generational Team

73% of advisors believe Millennials and Gen Z require different engagement than Boomers and Gen X. Your solution? Team diversity.

Consider:

Hiring younger advisors: They naturally connect with peer clients and understand digital-first communication

Creating mentorship programs: Pair experienced advisors with tech-savvy newcomers

Specializing service teams: Some advisors focus on legacy clients while others build next-gen relationships

Leveraging different communication styles: Let team members engage with clients through their preferred methods

Expand Your Service Offering

Next-gen clients want more than investment management. They're seeking:

Holistic financial planning: Tax strategies, estate planning, insurance, debt management

Life coaching elements: 85% of Millennials and Gen Z want behavioral coaching for support and accountability

Impact investing options: Sustainable and ESG-focused portfolios

Alternative investment access: Private equity, venture capital, crypto (where appropriate)

Concierge services: Some firms now offer medical concierge, education advisory, and cybersecurity advice

The Surmount Wealth Advantage for RIAs

The great wealth transfer creates an existential question for RIAs: adapt or become obsolete. The firms that will thrive are those that can simultaneously serve multiple generations with distinct needs, communication preferences, and investment philosophies.

This is precisely where Surmount Wealth's platform becomes invaluable for forward-thinking RIAs. Rather than choosing between serving your profitable Boomer clients and capturing next-gen wealth, Surmount provides the technology infrastructure that enables both.

Why RIAs Choose Surmount:

Unified technology platform that delivers sophisticated digital experiences younger clients demand while maintaining the personalized service Boomers expect

Flexible communication channels supporting everything from traditional quarterly reviews to real-time app notifications

Advanced portfolio management tools enabling everything from traditional 60/40 allocations to alternative investments and ESG strategies

Scalable infrastructure that grows with your firm as you expand your multi-generational client base

Client portal technology providing the 24/7, mobile-first access that's non-negotiable for younger investors

The wealth transfer isn't coming—it's here. By 2030, 30% of wealthy individuals will have received their inheritance. By 2035, that number jumps to 63%. Your window to build relationships with next-gen wealth is closing rapidly.

The firms that will capture their share of this $124 trillion transfer are those investing now in the technology, team structure, and service models that resonate with Millennials and Gen Z—without abandoning the clients who built their practices.

About Surmount Wealth: Surmount Wealth provides cutting-edge technology solutions that empower RIAs to serve multi-generational clients with sophisticated digital experiences and comprehensive wealth management tools. Learn how we can help your firm capture next-generation wealth at surmountwealth.com.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.