Blog

The traditional 60/40 portfolio no longer delivers the income or diversification it once did. With yields on investment-grade bonds still below long-term averages and equity volatility testing conventional risk frameworks, high-net-worth investors are increasingly exploring income strategies beyond the public markets. Yet access to these alternatives—and the infrastructure to manage them efficiently—remains fragmented across the advisory landscape.

For registered investment advisors serving sophisticated clients, the question isn't whether to incorporate alternative income, but which vehicles offer genuine diversification and how to implement them without operational friction. Private credit expanded to approximately $1.5 trillion at the start of 2024, up from $1 trillion in 2020, while structured investment sales volumes hit a record $84.5 billion in 2024, a 42% year-over-year increase. These aren't niche plays anymore—they're structural shifts in how wealth is allocated and preserved.

REITs: Public Markets Meet Real Asset Exposure

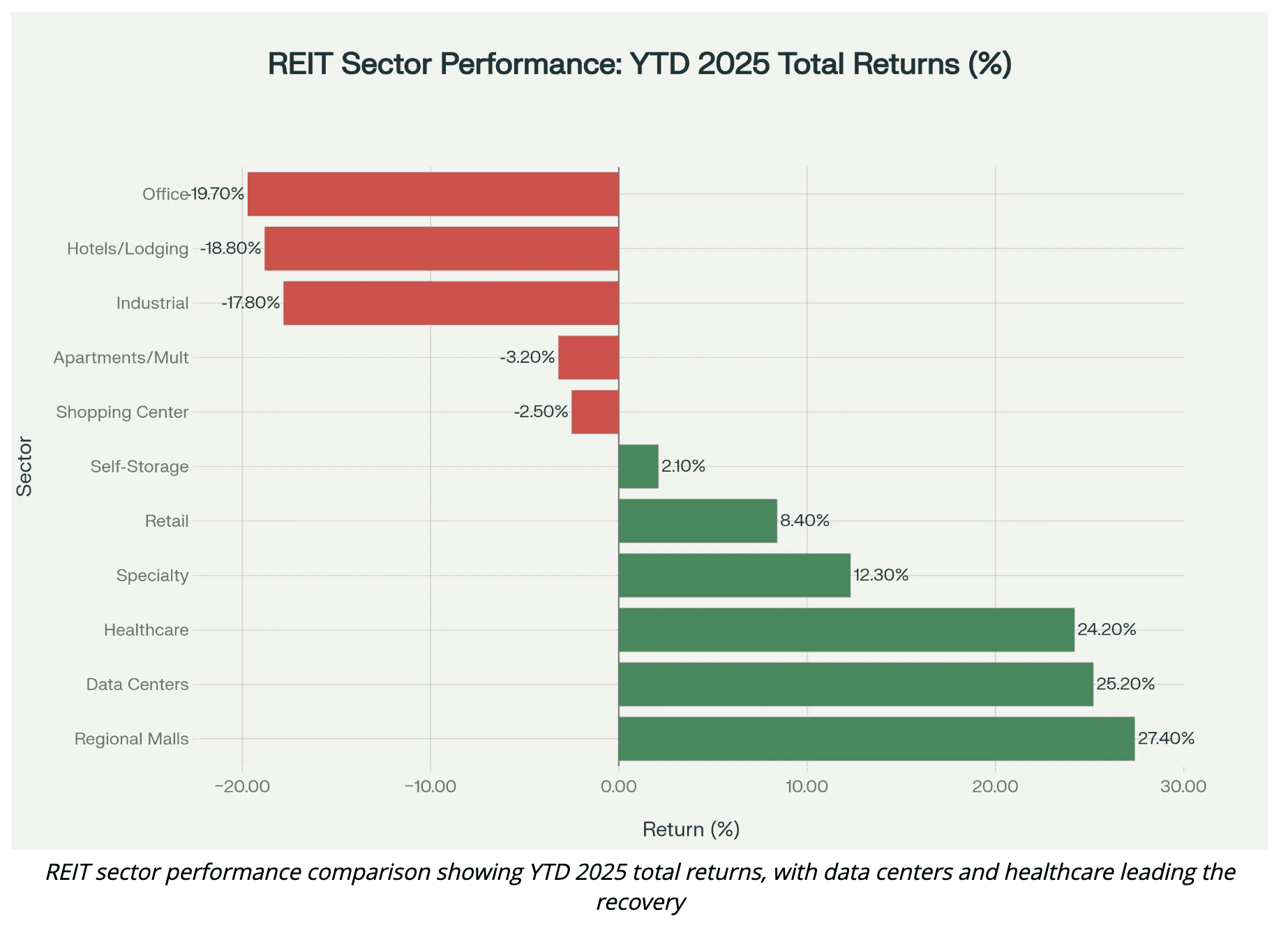

Real estate investment trusts offer something rare in alternative income: daily liquidity paired with exposure to hard assets. The FTSE Nareit All Equity REIT Index recorded a 14% total return through November 2024, outperforming private real estate by more than 17 percentage points as private valuations slowly adjusted to the higher rate environment.

But REIT performance varies dramatically by sector. Data centers posted 25.2% returns in 2024, while healthcare REITs delivered 24.2%. Industrial REITs, by contrast, faced headwinds from oversupply and tariff concerns, posting negative 17.8% returns. The dispersion matters: blanket REIT exposure misses the structural drivers creating opportunity.

What's working in 2025:

Strip retail centers benefit from limited high-quality space and strong demand

Data center REITs capitalize on AI infrastructure build-out

Single-family residential maintains pricing power as homeownership costs remain 50% higher than renting

The case for REITs in high-net-worth portfolios isn't just income. Institutional investors now use REITs in 60% of the largest North American portfolios, primarily for geographic and sector diversification that private holdings can't efficiently deliver. When Norges Bank Investment Management allocates 51% of its real estate exposure to public REITs, it's signaling something about liquidity, transparency, and operational efficiency that advisors managing complex client bases should note.

Private Credit: Floating Rates and Direct Lending Economics

Private credit has moved from institutional backwater to mainstream alternative in less than five years. The reason is structural, not cyclical: banks retreated from middle-market lending after 2008, and non-bank lenders filled the gap with better terms for borrowers and higher yields for investors.

Direct lending posted an annualized return of 10.5% in Q4 2024, beating high-yield bonds and leveraged loans even as the Federal Reserve cut rates. That performance stems from floating-rate structures that adjust as benchmark rates move, protecting real returns in ways fixed-income can't. For context, one of the largest private credit funds offered an annualized distribution rate of 10.4% in December 2024, compared with 8.2% for high-yield bond funds.

The appeal for advisors:

Floating rates provide natural inflation hedging

Senior secured positions offer downside protection during credit stress

Direct relationships with borrowers enable proactive portfolio management

But private credit isn't monolithic. Evergreen funds now have over $500 billion in AUM, targeting private wealth with semi-liquid structures. Meanwhile, opportunistic credit and specialty finance strategies saw significant inflows in 2024 as investors sought uncorrelated returns beyond traditional direct lending.

For RIAs building institutional-quality portfolios at scale, the challenge isn't finding private credit—it's integrating it efficiently. Subscription documents, capital calls, reporting across multiple fund structures: the operational burden compounds quickly. High-net-worth investors drove $48 billion into private credit markets in the first half of 2025, but many advisors still lack the infrastructure to manage these allocations alongside public holdings.

Structured Notes: Customizing Return Profiles in Volatile Markets

Structured notes combine bond mechanics with derivative overlays to deliver outcomes traditional securities can't: principal protection with equity upside, enhanced income with downside buffers, or participation in specific market scenarios.

U.S. structured note issuance volume increased more than 40% between 2023 and 2024, reaching $194 billion. That growth reflects demand for customization in portfolios where standard allocations no longer suffice. The products deliver: 660 out of 669 structured products that matured in 2024 generated positive returns, with structured notes achieving 7.49% average annualized returns over 2.81 years.

Common structures for high-net-worth portfolios:

Growth notes offer leveraged upside participation (e.g., 150% of S&P 500 gains) with hard or soft downside protection

Income notes provide fixed coupons even in sideways markets, with protection levels that preserve principal unless specific thresholds are breached

Market-linked CDs deliver FDIC insurance up to standard limits while offering equity-linked returns

The appeal for sophisticated investors is surgical: you can dial in precise exposure to volatility, interest rates, or specific equity outcomes without taking directional bets. During the market turbulence of late 2018, income note yields spiked as banks sold options at elevated volatility premiums—exactly when investors wanted yield most.

But complexity cuts both ways. Structured notes are debt obligations of issuing banks, introducing credit risk that doesn't exist in direct equity or bond holdings. Early redemption typically isn't available, and secondary market liquidity varies. Banks also bake margins into the structure's terms through conservative assumptions, making issuer selection and competitive bidding processes critical.

For RIAs managing multiple client portfolios with varying risk tolerances, structured notes offer mass customization—if the operational infrastructure exists to execute, monitor, and rebalance efficiently.

Building the Infrastructure for Alternative Income

The opportunity in alternative income isn't access—platforms and products proliferate. The constraint is implementation. RIAs lag wirehouses in alternatives adoption, with only 3.35% of national RIA client assets allocated to alternatives versus higher percentages at wirehouse competitors.

Why? The biggest hurdles include operational support shortages, reporting complexity, and indexing preferences. Put differently: advisors know alternatives belong in portfolios, but managing subscription documents, capital call waterfalls, illiquid position tracking, and consolidated reporting across multiple custodians creates friction that scales poorly.

This is where infrastructure matters more than product selection. Modern advisory platforms need to:

Aggregate alternative positions alongside public holdings in unified reporting

Automate capital call funding and distribution reinvestment

Track illiquid valuations with transparent methodologies

Support tax reporting across diverse alternative structures

Enable rebalancing that accounts for liquidity constraints

Platforms like iCapital and CAIS have grown rapidly by solving exactly these operational problems, but many RIAs still cobble together alternative allocations using tools designed for public securities.

Surmount Wealth approaches this differently: by treating alternative income as a core portfolio component, not an afterthought. When REITs, private credit, royalties, and structured notes sit alongside equities and bonds in the same data-driven infrastructure, advisors can build truly customized portfolios without operational overhead scaling linearly with complexity. The platform handles position tracking, performance attribution, and client reporting whether you're allocating to Vanguard index funds or evergreen private credit vehicles.

The Opportunity Ahead

The case for alternative income in high-net-worth portfolios has never been clearer. Traditional fixed income doesn't deliver the yield or diversification clients require, equity volatility tests conventional risk frameworks, and inflation remains structurally higher than the decade following the financial crisis.

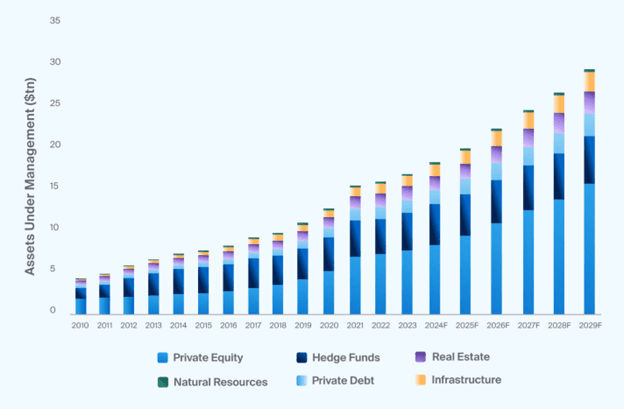

Alternative investments are projected to grow from $18 trillion in 2024 to nearly $29 trillion by 2029. National RIAs expect the share of clients with alternatives to jump to 35% in 2026, with weighted average allocations rising to 15%. The advisors who thrive won't be those with the most exotic products—they'll be those with infrastructure that makes alternatives as operationally seamless as ETFs.

The question for every RIA managing sophisticated wealth: does your platform support the portfolio construction you know your clients need, or are you constrained by technology built for a simpler era? Alternative income isn't the future of wealth management—it's the present. The only question is whether your firm can deliver it efficiently.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.