Blog

The average high-net-worth client pays somewhere between 15% and 23.8% on investment gains—a figure that compounds into millions over a career. Yet most advisors treat capital gains as a static compliance issue rather than a dynamic planning lever. That's a mistake. In 2025, with tax brackets adjusted for inflation and clients increasingly sophisticated about after-tax returns, capital gains strategy has become table stakes for modern wealth management.

This isn't about tax avoidance. It's about precision—structuring client portfolios to maximize wealth retention within a constantly shifting regulatory framework. Let's break down everything RIAs need to understand about capital gains tax, from the mechanics to the strategic implications.

The Two-Tier System: Why Holding Period Matters More Than Ever

Capital gains fall into two categories, and the distinction matters more than most investors realize.

Short-term capital gains apply to assets held for one year or less and are taxed as ordinary income at rates ranging from 10% to 37%. That top bracket hits quickly—single filers earning above $626,350 in 2025 face the maximum rate.

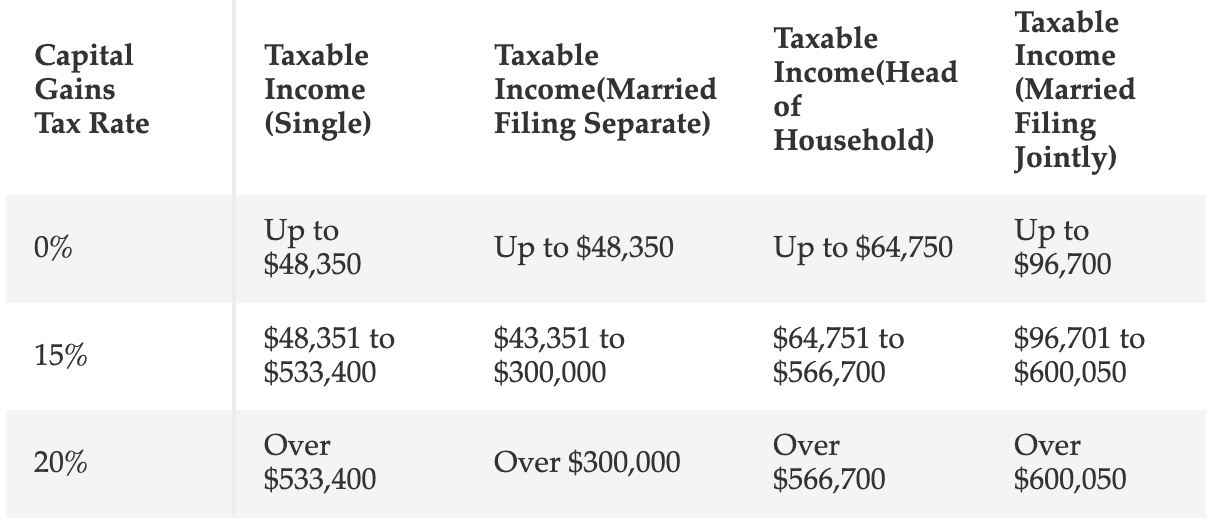

Long-term capital gains enjoy preferential treatment. For assets held longer than twelve months, the tax rate drops dramatically: 0%, 15%, or 20%, depending on taxable income. For 2025:

0% rate: Single filers with taxable income up to $48,350 ($96,700 for married filing jointly)

15% rate: Single filers between $48,350 and $533,400 ($96,700 to $600,050 for married filing jointly)

20% rate: Single filers above $533,400 ($600,050 for married filing jointly)

The delta between a 37% short-term rate and a 20% long-term rate represents a potential 17-percentage-point tax differential. On a $1 million gain, that's $170,000 in additional taxes—wealth that could compound for decades if properly retained.

Here's the strategic insight most advisors miss: these brackets aren't just about rates. They're about timing windows and income stacking. A client sitting just below the 15% threshold who realizes a large gain could vault into the 20% bracket—but if that same gain is strategically recognized across two tax years, they might stay in the 15% zone entirely. This is where automation and real-time tax modeling become invaluable.

The Net Investment Income Tax: The 3.8% Surtax High Earners Can't Ignore

Beyond standard capital gains rates, high-income clients face an additional 3.8% Net Investment Income Tax (NIIT) on investment earnings. Introduced in 2013 and never indexed for inflation, the NIIT thresholds remain fixed:

$200,000 for single filers

$250,000 for married filing jointly

$125,000 for married filing separately

The NIIT applies to the lesser of your net investment income or the amount by which your modified adjusted gross income (MAGI) exceeds these thresholds. For a single filer earning $300,000 with $75,000 in investment income, the NIIT applies to the lower figure—either the $75,000 in investment income or the $100,000 MAGI excess. They'd owe 3.8% on $75,000, or $2,850.

Between 2013 and 2021, the number of taxpayers subject to NIIT more than doubled—from 3.1 million to 7.3 million—with total collections jumping from $16.5 billion to $59.8 billion. That's the inflation penalty: as incomes rise nominally, more clients cross static thresholds without seeing real income gains.

For advisors, this creates opportunity. The NIIT doesn't apply to distributions from tax-deferred accounts like traditional IRAs and 401(k)s, nor does it touch Roth IRA withdrawals. This makes Roth conversions and strategic IRA distributions powerful planning tools for clients hovering near NIIT thresholds. Platforms that can model these interactions in real-time—showing clients exactly how a $50,000 Roth conversion impacts both current-year NIIT and long-term tax-free growth—deliver tangible, demonstrable value.

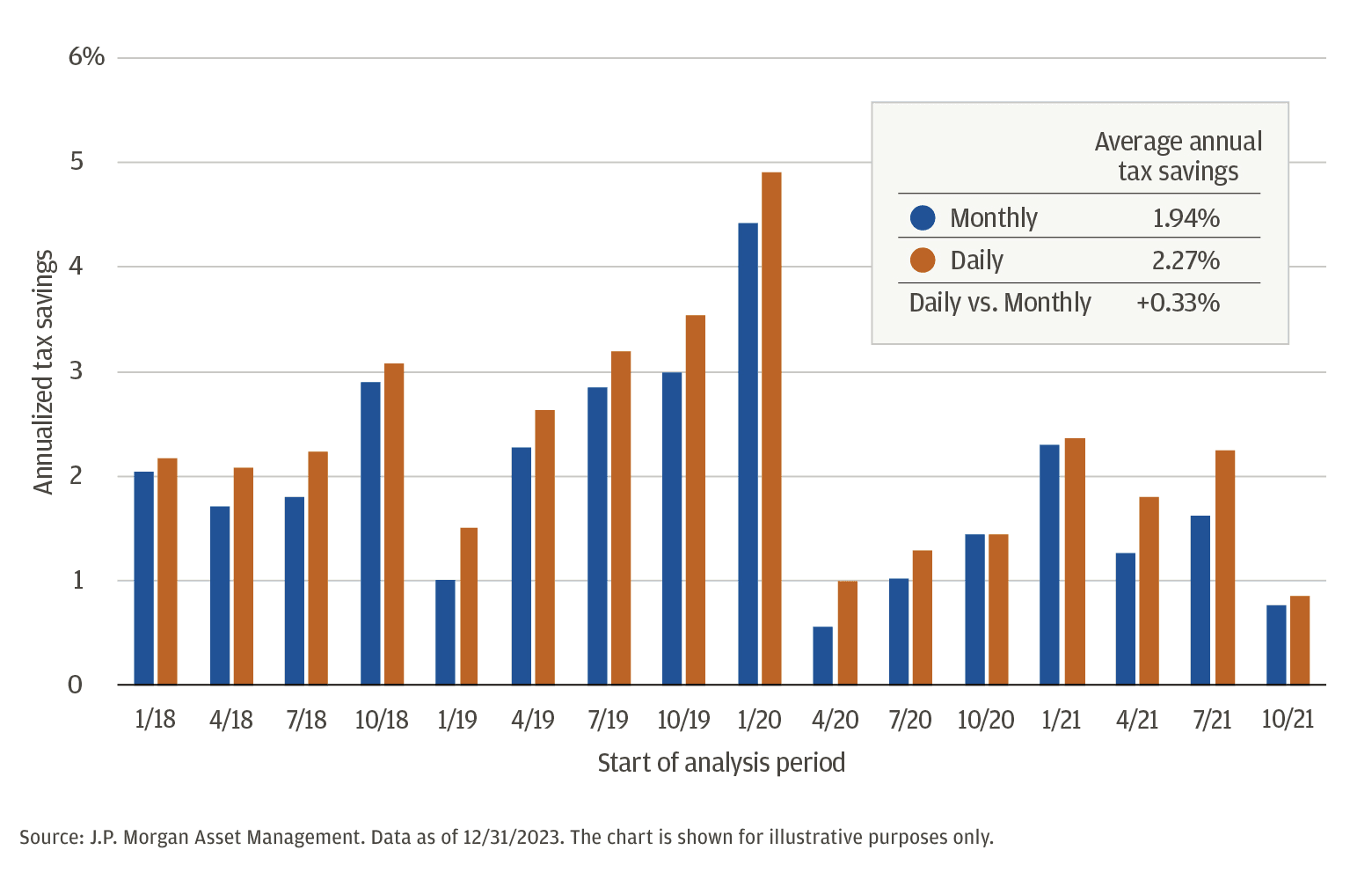

Tax-Loss Harvesting: From Year-End Scramble to Systematic Alpha

Tax-loss harvesting—selling depreciated securities to offset gains—has traditionally been an end-of-year exercise. But that approach leaves value on the table.

Research from J.P. Morgan found that daily tax-loss harvesting generates approximately 30 basis points of additional annualized tax savings compared to monthly monitoring. Over a decade, that compounds into meaningful wealth preservation. The difference comes down to market volatility: intra-month dips that recover by month-end are invisible to quarterly or annual scans but can be captured with continuous monitoring.

The mechanics are straightforward but require discipline:

Losses offset gains of the same type first (short-term losses against short-term gains, long-term against long-term)

Excess losses can offset up to $3,000 of ordinary income annually

Unused losses carry forward indefinitely

The wash sale rule prohibits repurchasing the same or substantially identical security within 30 days before or after the sale

Here's where systematization matters. A client in the 37% bracket who harvests a $10,000 short-term loss saves $3,700 immediately. If that $3,700 is reinvested at 6% annual returns, it compounds to over $6,600 in 10 years—wealth created purely through tax efficiency, not market timing or alpha generation.

Yet manual tax-loss harvesting is labor-intensive and error-prone. Modern platforms that automate continuous loss monitoring, ensure wash sale compliance, and immediately reinvest proceeds into similar (but not identical) exposures can transform this from a sporadic tactic into a consistent value driver. For RIAs managing dozens or hundreds of client accounts, automation isn't a luxury—it's the only scalable approach.

Special Rules That Create Planning Opportunities

Beyond the standard framework, several special rules create strategic openings for sophisticated advisors:

Qualified Small Business Stock (QSBS) under Section 1202 allows non-corporate taxpayers to exclude up to 100% of gains on certain small business stock held for more than five years. The exclusion caps at the greater of $15 million (for stock issued after July 4, 2025) or 10 times the adjusted basis. For founders and early-stage investors, this can eliminate federal capital gains tax entirely on successful exits—a potential savings of up to 23.8%.

Collectibles and real estate face special treatment. Gains on art, coins, and antiques are taxed at a maximum 28% rate. Unrecaptured Section 1250 real estate depreciation is taxed at 25%. These rates apply regardless of holding period, creating planning complexity for clients with diverse asset bases.

Primary residence exclusions allow taxpayers to exclude up to $250,000 of gain ($500,000 for married couples filing jointly) on the sale of a principal residence, provided they've lived in the home for at least two of the past five years. This benefit doesn't just apply once—it can be used repeatedly throughout a lifetime, making strategic home sales a legitimate wealth-building tool for high-net-worth clients in appreciating markets.

Where Technology Meets Tax Strategy

Here's the reality: capital gains optimization at scale requires infrastructure that most advisors don't have. It's not enough to know the rules—you need systems that can:

Monitor portfolios continuously for loss-harvesting opportunities

Model multi-year tax scenarios with variable income streams

Coordinate capital gains realization with Roth conversions, charitable giving, and retirement distributions

Track cost basis across multiple accounts and asset types

Ensure wash sale compliance automatically

This is where modern RIA infrastructure separates leaders from laggards. Surmount Wealth's platform doesn't just track these variables—it automates the heavy lifting. Advisors can set client-specific tax rules, monitor portfolios in real-time for optimization opportunities, and execute tax-aware rebalancing without the manual calculations that typically bottleneck tax-smart strategies.

Source: Kiplinger

The competitive advantage isn't just better technology, it's demonstrable better outcomes. Clients who see their after-tax returns systematically exceed benchmarks understand the value proposition viscerally. They're not paying for generic portfolio management; they're paying for precision tax engineering that compounds over decades.

The Strategic Takeaway

Capital gains aren't a once-a-year compliance exercise—they're a continuous optimization opportunity. The advisors who thrive in the coming decade will be those who can demonstrate consistent, measurable after-tax alpha through systematic tax management.

For RIAs, that means moving beyond spreadsheets and year-end scrambles toward infrastructure that makes tax optimization automatic, scalable, and provable. The math is simple: a 1% annual improvement in after-tax returns compounds to a 28% wealth differential over 25 years. That's not theory—that's what separates great advisors from average ones.

The clients who recognize this aren't looking for another passive index fund. They're looking for partners who understand that wealth preservation is as important as wealth creation—and who have the tools to deliver both.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.