Blog

The high-yield bond market took decades to become respectable. Private credit did it in fifteen years.

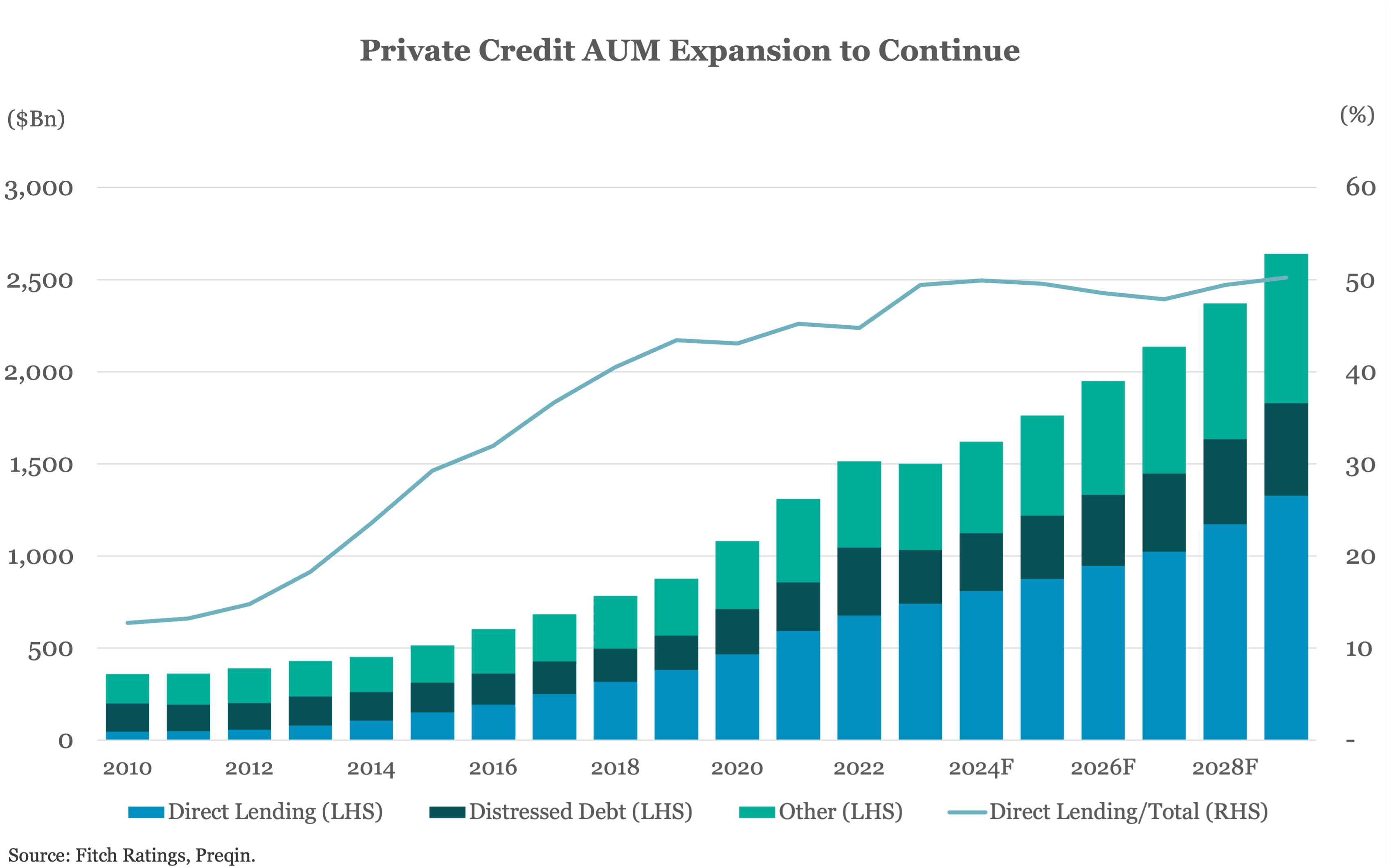

What began as a niche alternative for middle-market companies shut out of bank financing has evolved into a $3 trillion asset class projected to reach $5 trillion by 2029. Pension funds, insurance companies, and sophisticated family offices aren't just dipping their toes in—they're repositioning entire fixed-income allocations around private credit strategies. The question for RIAs isn't whether to understand this shift, but whether they have the infrastructure to deliver it effectively.

This isn't another hot alternative du jour. Private credit represents a fundamental restructuring of how corporate debt works, driven by regulatory changes, bank retreat from leveraged lending, and investor demand for yield that doesn't sacrifice quality. For advisors managing high-net-worth portfolios, the implications run deep.

The Structural Forces Creating a Permanent Asset Class

Private credit didn't emerge from thin air. It filled a vacuum created by post-2008 banking regulations that made traditional bank lending to mid-market companies less economically attractive. Basel III capital requirements, Dodd-Frank stress testing, and liquidity coverage ratios collectively pushed banks toward lower-risk, more liquid lending. Middle-market businesses—defined loosely as companies with $50-150 million in EBITDA—suddenly faced a financing gap.

Private credit funds stepped in. The market grew from $46 billion in 2000 to roughly $1 trillion in 2023, with acceleration particularly pronounced after 2019. By 2025, the U.S. market alone has reached approximately $1.3 trillion, rivaling the size of both the high-yield bond and leveraged loan markets.

What makes this growth sustainable rather than speculative? Three factors:

Speed and certainty for borrowers. Private credit can close a $100 million financing in weeks, not months. For private equity sponsors executing buyouts or companies needing growth capital, that execution certainty is worth paying up for. Public bond markets require extensive disclosure, ratings processes, and syndication—all of which introduce timing risk that can kill deals.

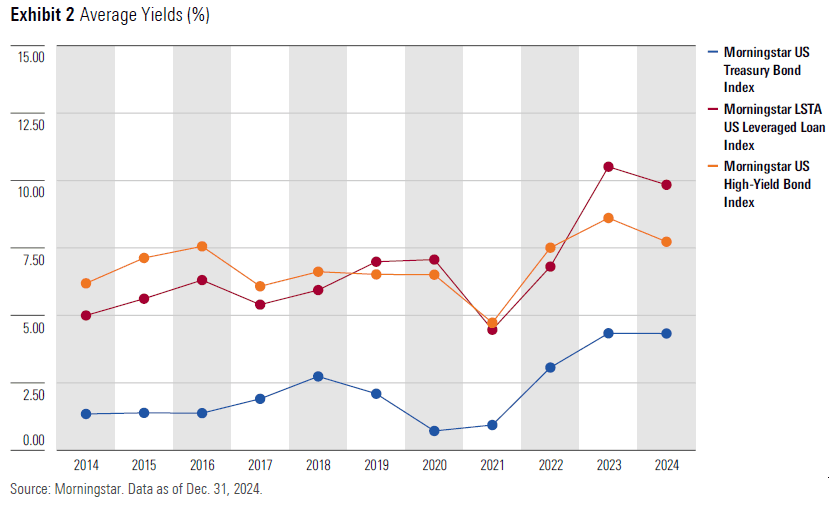

Floating-rate structure in a higher-rate world. Most private credit loans carry floating rates tied to SOFR plus a spread. When the Fed raised rates from near-zero to over 5%, direct lending returned 11.6% during rising-rate periods—outperforming its long-term average by 200 basis points. High-yield bonds, by contrast, suffered from duration risk.

Structural seniority and covenant protection. Private credit typically sits at the top of the capital structure as senior secured debt. Lenders negotiate detailed financial covenants, information rights, and control provisions that public bondholders can only dream about. When a borrower starts struggling, private lenders have contractual leverage to restructure proactively rather than watch from the sidelines.

The Return Profile: Illiquidity Premium or Complexity Tax?

Here's where advisor due diligence matters. Private credit currently offers yields in the 10-15% range, with a yield premium of approximately 226 basis points over comparable B-rated public loans—nearly double the historical average of 121 basis points since 2021.

That premium compensates for three things:

Illiquidity risk: Private credit investments typically lock up for 5-10 years with no secondary market liquidity

Complexity risk: Bespoke loan structures require specialized manager expertise to underwrite and monitor

Valuation opacity: Loans are marked based on manager assessments, not daily market clearing prices

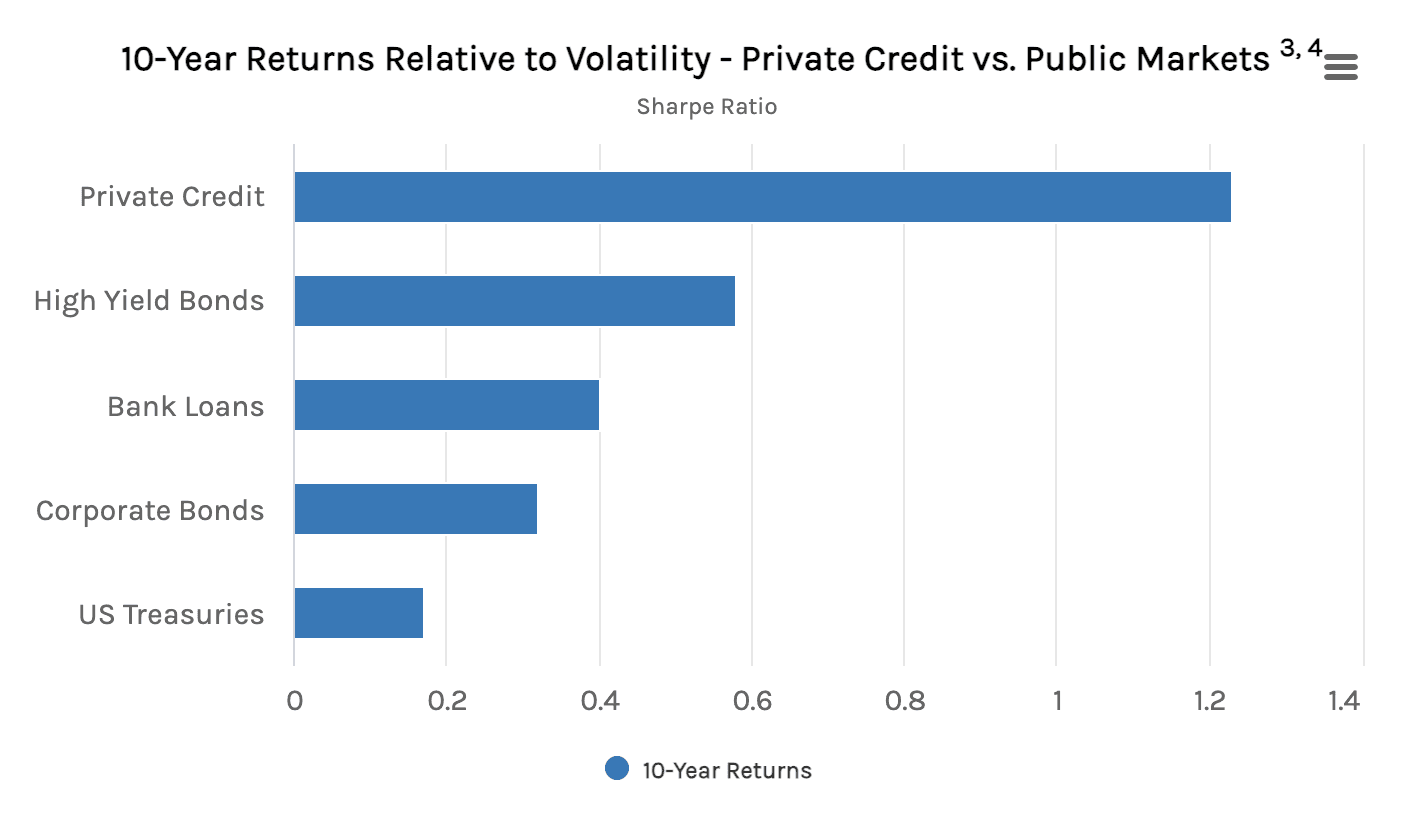

The relevant question isn't whether that premium exists—it's whether it's sufficient relative to the risks. Historical data shows private credit has outperformed high-yield bonds by approximately 150 basis points over the past decade, with meaningfully lower volatility. The Cliffwater Direct Lending Index, which tracks over 16,000 directly originated loans, demonstrates this pattern consistently across market cycles.

But context matters. Private credit borrowers show weaker fundamentals than public markets: interest coverage of 2.1x versus 3.9x for public companies, leverage of 5.6x versus 4.6x, and EBITDA margins of 14.9% versus 16.4%. These companies are riskier by design—that's why they can't access bank financing or public markets efficiently.

The trade-off is recoveries. Private credit recovery rates average 68% compared to lower recovery rates in unsecured high-yield bonds, largely due to senior secured positioning and active workout capabilities.

For high-net-worth investors, the calculus becomes: are you being compensated fairly for accepting illiquidity and complexity, given your portfolio's liquidity needs and risk tolerance?

Access Barriers and the Democratization Push

This is where the rubber meets the road for most advisors. Private credit has historically been available only to institutional investors and ultra-high-net-worth individuals through closed-end funds with $5-25 million minimums. The accredited investor standard—$1 million net worth excluding primary residence, or $200,000+ annual income—is the baseline, but practical access requires significantly more capital.

Recent innovations are changing that equation. Business Development Companies (BDCs) and interval funds now offer private credit exposure with minimums as low as $25,000-100,000, bringing the asset class within reach of a broader swath of accredited investors. BDCs, which must distribute at least 90% of income to shareholders, have grown rapidly to represent $500 billion of the private credit market.

But accessibility doesn't equal suitability. These structures come with management fees typically ranging from 1.5-2.0% annually, plus performance fees of 20% above hurdles. Compare that to 0.03-0.10% for index bond ETFs. The question becomes whether after-fee returns justify the cost and complexity.

For RIAs, this creates both opportunity and obligation. Clients who qualify for private credit access expect advisors to conduct meaningful due diligence—not just on the underlying credit strategy, but on manager selection, fee structures, liquidity terms, and portfolio fit.

The Risks That Keep Allocators Up At Night

No discussion of private credit is complete without acknowledging the concerns raised by regulators and skeptics. The Federal Reserve has flagged several potential stability issues:

Opacity and mark-to-market challenges. Unlike public bonds that trade daily, private credit valuations rely on manager assessments. When markets dislocate, there's potential for valuation lag—or worse, valuation manipulation. Jeffrey Gundlach has drawn parallels to pre-2008 CDO markets, calling private credit "the Wild West" of finance.

Deteriorating underwriting standards. With $3 trillion in committed but undeployed "dry powder" across private credit funds, managers face pressure to deploy capital. Competition for deals can lead to covenant-lite structures, aggressive leverage, and weaker documentation—exactly what happened in leveraged loans before the 2008 crisis.

Interconnectedness with banks. Banks aren't retreating from private credit—they're changing their exposure. Many provide credit lines to private credit funds, creating indirect leverage and potential contagion pathways if credit quality deteriorates.

Liquidity mismatch potential. While most private credit is structured with long lock-ups, newer interval funds and semi-liquid vehicles create potential for redemption pressures during stress periods. Unlike banks with FDIC backstops, private credit funds facing capital calls during market dislocations have limited buffers.

These aren't theoretical concerns. They're structural vulnerabilities that sophisticated allocators actively monitor and model. For RIAs, the implication is clear: private credit belongs in portfolios, but with appropriate sizing, diversification, and manager selection discipline.

Where Private Credit Fits in Modern Portfolio Construction

The asset allocation question for RIAs managing $5-50 million portfolios is straightforward: how much private credit, which strategies, and through what vehicles?

Research from firms like Wellington Management suggests institutional investors with long-term capital (pensions, endowments) allocate 10-15% to private credit to maintain consistent yield enhancement while managing liquidity risk. High-net-worth individuals with shorter planning horizons might target 5-10%, with higher allocations in more liquid structures like BDCs.

The selection matrix should consider:

Strategy type: Direct lending (senior secured) offers lower returns with better downside protection; mezzanine and distressed strategies offer higher returns with more risk

Manager quality: Track record matters enormously in private credit—experienced managers with disciplined underwriting significantly outperform

Fee structures: Net returns after fees should meaningfully exceed public market alternatives to justify illiquidity

Portfolio integration: Private credit should complement, not replace, traditional fixed income—it serves a different liquidity and risk function

This is where modern RIA infrastructure becomes non-negotiable. Managing private credit allocations at scale requires:

Continuous manager due diligence and monitoring

Client-specific liquidity modeling to ensure allocation sizing fits individual circumstances

Performance tracking that accounts for the J-curve effect and time-weighted returns

Tax-aware positioning, since private credit generates ordinary income rather than qualified dividends

Surmount Wealth's platform addresses these requirements systematically. Rather than forcing advisors to build bespoke private credit monitoring workflows, the infrastructure handles manager tracking, liquidity modeling, and client-specific allocation recommendations automatically. When a client asks about private credit exposure, advisors can pull instant reports showing how current allocations fit their liquidity profile, risk tolerance, and return objectives.

The competitive advantage isn't just having access to private credit—it's having the infrastructure to deploy it thoughtfully at scale across dozens or hundreds of client relationships without manual spreadsheet work.

The Strategic Takeaway

Private credit represents a permanent structural shift in how mid-market companies access capital and how sophisticated investors generate fixed-income returns. This isn't a cyclical trade or a momentum play—it's a fundamental reallocation of corporate debt from bank balance sheets to institutional portfolios.

For RIAs, the opportunity is clear but demands execution discipline. Clients with appropriate wealth levels and liquidity profiles can benefit from private credit's yield premium and structural protections. But delivering that exposure effectively requires infrastructure that most advisors don't have: manager due diligence capabilities, liquidity modeling tools, and portfolio integration frameworks that work at scale.

The firms that thrive in this environment won't be those who simply gain access to private credit funds. They'll be those who can deliver private credit exposure systematically, with appropriate sizing, manager selection, and ongoing monitoring—all while managing the liquidity and complexity trade-offs inherent to the asset class.

That's not a product offering. It's an infrastructure question. And infrastructure is exactly what separates advisors who talk about alternatives from those who actually deliver value through them.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.