Blog

Gen Z Clients Demand a Different Playbook

How RIAs can adapt their strategies to capture the most proactive generation of savers since the 401(k) era began

The narrative around Gen Z and money has long centered on avocado toast memes and financial irresponsibility. The data tells a different story—one that should have every forward-thinking RIA reconsidering their approach to young clients.

Gen Z adults began investing and saving at an average age of 19, according to the 2024 Charles Schwab Modern Wealth Survey. That's six years earlier than millennials and sixteen years ahead of baby boomers, who started at 35. This generational shift represents more than precocity—it signals fundamentally different expectations about financial guidance, technology, and the advisor-client relationship.

A Generation Shaped by Economic Disruption

Gen Z entered adulthood witnessing their parents navigate the 2008 financial crisis, then faced their own trial with pandemic-era disruption. The result is a cohort approaching money with both urgency and skepticism.

According to Bank of America's 2025 Better Money Habits study, 72% of Gen Z took steps to improve their financial health over the past year, with 51% directing money toward savings. Yet the same study found that 55% lack emergency savings to cover three months of expenses. Bank of America's internal data analysis revealed that Gen Z's spending-to-savings ratio reached 1.93 in early 2025—nearly twice what they have in savings.

This tension between financial engagement and financial precarity creates a distinctive advisory opportunity.

The Retirement Paradox: Starting Early, Saving Less

The generational investment gap deserves careful examination. Research from the Investment Company Institute shows that Gen Z households with defined contribution plans have nearly three times more assets—adjusted for inflation—than Gen X households had at the same age in 1989. Automatic enrollment and improved plan design deserve much of the credit, but Gen Z's willingness to participate matters too.

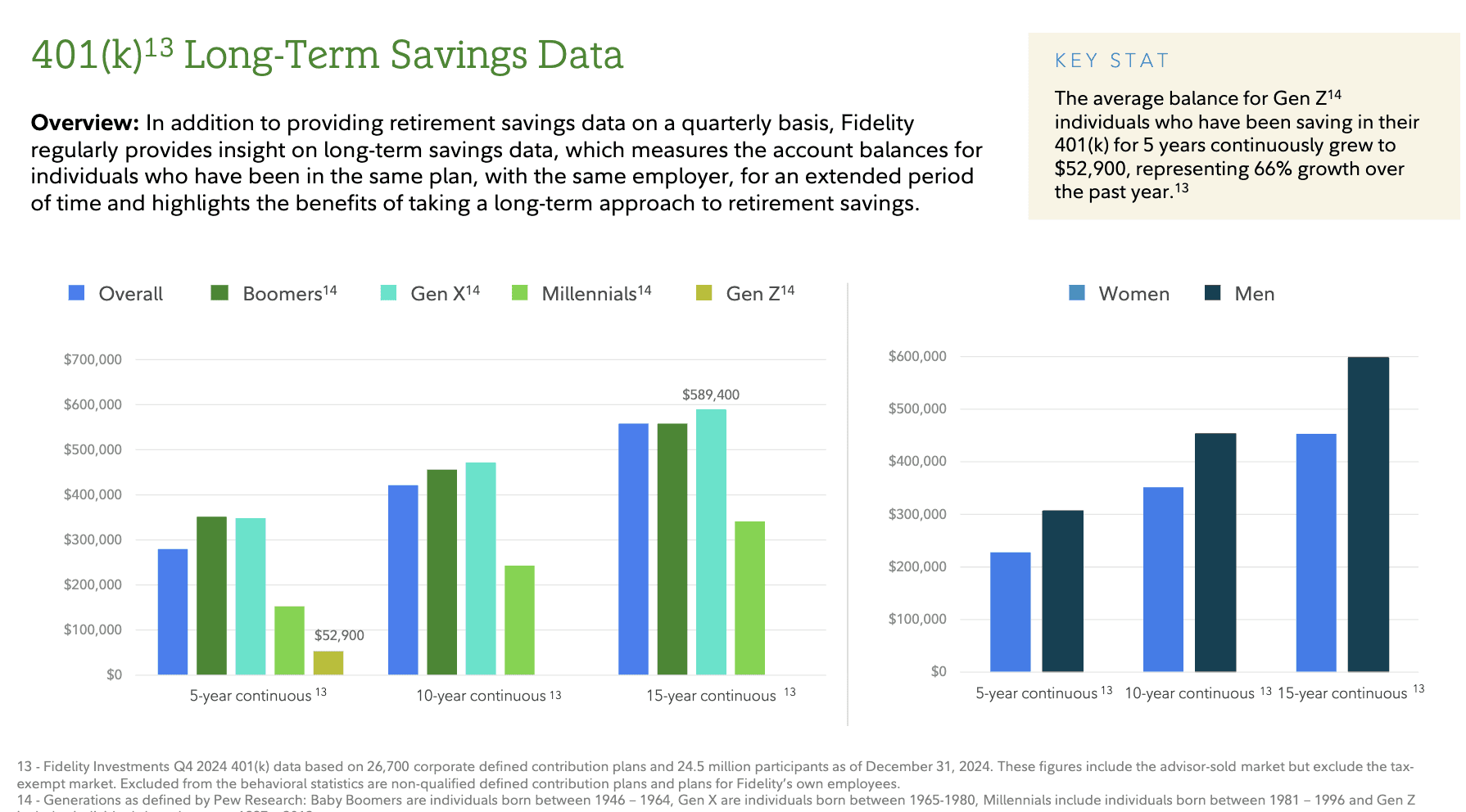

Fidelity's Q4 2024 retirement analysis showed that Gen Z individuals who have been saving in their 401(k) for five years saw their average balance grow to $52,900—a 66% increase over the prior year. The number of Gen Z Roth IRA accounts increased 71% year-over-year, with female Gen Z account ownership up 60%.

However, two data points complicate this encouraging narrative. First, Nationwide's 2024 Advisor Authority survey found that 14% of Gen Z investors don't expect to retire at all—a higher percentage than non-retired members of older generations. Second, only 20% of Gen Z are actively saving for retirement, according to TIAA's 2024 research.

The picture that emerges is a generation that starts early when prompted by employer plans and automated systems, but struggles to maintain consistent savings behavior amid competing financial pressures.

The Digital-Native Client Experience

Gen Z's information consumption patterns differ fundamentally from previous generations. The FINRA Foundation and CFA Institute's 2023 research found that 82% of Gen Z investors in the U.S. began investing before age 21, with 25% starting before they turned 18. Crucially, they learned about investing primarily through social media (48%), internet searches (47%), and parents or family (45%).

Nationwide's research puts the social media reliance in stark generational context: 42% of Gen Z investors access financial information through social media, compared to just 16% of Gen X and 5% of baby boomers. YouTube ranks highest among specific platforms at 60%, followed by Instagram, TikTok, Twitter, and Reddit.

This creates a challenge for advisors. A SmartAsset survey on marketing trends found that 97% of financial advisors never use TikTok, and 82% never use Instagram. The platforms where Gen Z consumes financial content are precisely where advisors have minimal presence.

Yet the opportunity is substantial. Nationwide found that 67% of Gen Z investors do not currently pay to work with a financial professional. For a generation that craves financial guidance but distrusts traditional gatekeepers, the advisor who can meet them where they already are has a significant competitive advantage.

What Gen Z Actually Wants from Advisors

Despite their digital orientation, Gen Z doesn't want to eliminate human advisors—they want to augment them. According to research from Nasdaq and TIFIN, 65% of millennials and Gen Z believe a financial advisor is important to achieve financial success, compared to 56% of baby boomers. More notably, 66% want to consolidate more assets with their primary advisor versus just 19% of boomers.

The difference lies in expectations. Gen Z wants comprehensive, whole-life advisory experiences, with 85% specifically requesting some form of behavioral coaching on financial decision-making. They seek personalization at a level previous generations rarely demanded.

Goldman Sachs Asset Management's 2024 retirement survey identified specific service gaps Gen Z wants filled: 37% seek emergency savings support as their most-wanted plan enhancement, followed by professional financial planning and advice services (36%) and retirement strategy education (28%).

The insight for RIAs is clear: Gen Z doesn't want simpler services—they want broader ones that address their actual challenges.

The Great Wealth Transfer Stakes

The business case for cultivating Gen Z clients extends beyond their immediate assets. Cerulli Associates projects that $124 trillion will transfer through 2048, with millennials inheriting $46 trillion over the next 25 years—the largest share of any generation. Gen X will inherit significantly in the next decade ($14 trillion), creating an immediate pipeline as well.

Yet Cerulli's research also warns that family meetings and regular communication are the most effective wealth transfer strategies for retaining assets across generations. Advisors who wait until clients pass away to engage their children will lose those assets—the research suggests fewer than 20% of affluent investors stick with their parents' advisors.

According to a recent Fortune analysis, the share of millennial and Gen Z clients at high-net-worth-focused firms grew from 8% in 2021 to 25% by 2024. The industry is already shifting, and the firms capturing these relationships early will benefit from decades of compounding assets.

Values-Based Investing: Opportunity Amid Volatility

Gen Z's relationship with sustainable investing deserves nuanced understanding. A 2025 Morgan Stanley survey found that 99% of Gen Z investors report interest in sustainable investing, with 80% planning to increase allocations versus 31% of boomers.

However, enthusiasm has cooled from its 2022 peak. Stanford Graduate School of Business research showed that in 2022, 44% of young investors thought it "extremely important" for investment companies to influence environmental priorities; by 2024, that dropped to 11%. Economic pressures made returns more urgent than values alignment. Advisors should frame sustainable investing as compatible with strong returns rather than requiring a trade-off.

Practical Implications for Advisory Firms

Embrace automation as table stakes. Gen Z expects digital account access, automated savings features, and real-time portfolio visibility. The question isn't whether to offer these capabilities—it's how to layer human advice effectively.

Address the full financial picture. Gen Z's most pressing concerns aren't retirement—they're emergency savings, student debt, and housing affordability. New York Life's 2025 Wealth Watch data shows Gen Z has the most ambitious savings goals ($22,374 average) and earliest target retirement age (60), but the highest cost-of-living barriers.

Leverage their early start. According to Charles Schwab, an investor contributing $5,000 annually starting at 19 could accumulate approximately $500,000 more by retirement than someone starting at 25. Illustrating compound returns helps Gen Z clients see the value of advice even with modest current balances.

Prepare for fee sensitivity. With Gen Z spending nearly twice their savings and facing student loan burdens (average $22,948 in 2024), fee structures matter intensely. Subscription-based models and transparent pricing appeal to a generation that researches everything before buying.

The Firms That Will Win

Gen Z represents both the smallest current assets and the longest investment horizon of any client segment. RIAs who view them only through near-term profitability will miss the opportunity; those who build scalable systems to serve younger clients efficiently will capture the great wealth transfer.

The winning firms will share several characteristics: digital-first infrastructure that reduces cost-to-serve, holistic planning that addresses emergency savings and debt alongside investments, transparent fee structures, and authentic presence in channels where Gen Z learns about money.

Most importantly, they'll recognize that Gen Z wants partners who respect their agency while providing expertise they know they lack. That requires rethinking not just marketing, but the entire advisory relationship.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.