Blog

Gold as the Sole Anchor: Analyzing Zero-Yield Assets in a Negative Real-Rate Environment

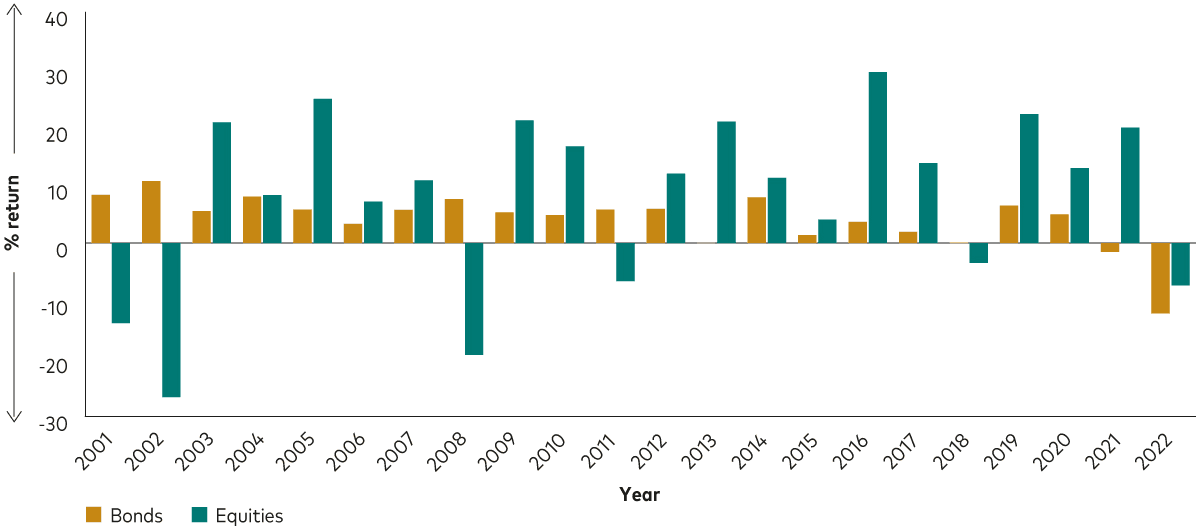

Recent studies, such as the one conducted by Vanguard UK, suggest that the traditional negative correlation between equities and high-quality bonds is undergoing a structural shift, frequently turning positive due to persistent inflation, high interest rate volatility, and fiscal policy concerns.

For over two decades, the negative correlation between equities and high-quality bonds was the holy grail of portfolio construction. It allowed advisors to promise clients a "free lunch": participate in equity upside while relying on a bond cushion that reliably inflated during growth scares.

However, increasingly, the empirical evidence seems to suggest that the cushion is fast getting evaporated.

The Correlation Flip

The "60/40" model was predicated on a disinflationary regime where the Federal Reserve had the "room" to cut rates whenever the economy faltered. In that world, bad news for stocks was good news for bonds. But in our current regime of fiscal dominance and persistent supply-side volatility, inflation has become the primary driver of both asset classes.

When inflation sits comfortably above the 3% threshold, the correlation between stocks and bonds tends to flip from negative to positive. We are no longer seeing a "flight to safety" in treasuries; instead, we are seeing a "flight from duration" as rising yields punish both equity valuations and fixed-income principal simultaneously. For the modern portfolio manager, this creates a "diversification desperation": if your hedges are falling in tandem with your risk assets, you aren't running a balanced portfolio—you are running a directional bet on lower volatility that isn't coming.

Defining the New "Safe"

In a world of positive correlations and falling real yields, the definition of a safe asset must evolve. We have moved from an era of Return on Capital to an era of Return of Purchasing Power.

Traditional fixed income, burdened by duration risk and a lack of inflation protection, is struggling to fulfill its mandate as a portfolio stabilizer. Consequently, institutional interest is rotating toward the only Tier-1 reserve asset that carries no counterparty risk and—crucially—no yield to be taxed away by inflation.

Gold, long dismissed as a "relic" of a previous century, is re-emerging not as a speculative play, but as the sole remaining anchor in an ocean of correlated volatility.

In this article, we will analyze why "zero yield" is actually a superior carry in a negative real-rate environment and how to tactically integrate gold into a modern, resilient mandate.

Zero Beats Negative Yield Any Day

The primary institutional objection to gold has historically been its lack of yield. In a disinflationary regime, where the "risk-free" rate provides a positive real return, the opportunity cost of holding a non-productive asset is high.

However, we have transitioned into a period of financial repression, or a macro-economic state where the government must systematically keep nominal interest rates below the rate of inflation to erode the real value of sovereign debt.

In this regime, the math for the "Safe Sleeve" of a portfolio fundamentally flips.

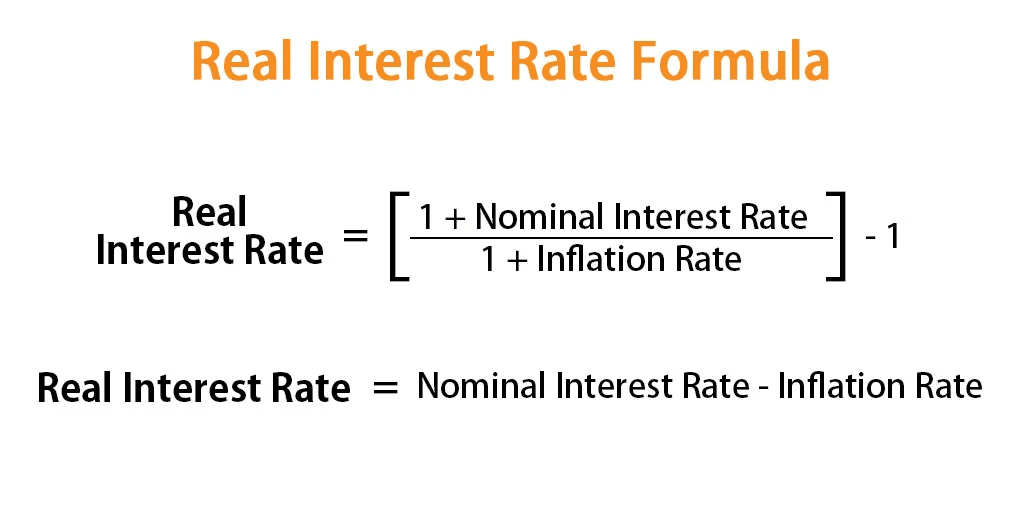

The Real Yield Equation

Professional allocators must look past nominal coupons to the Ex-Post Real Yield. The formula is straightforward:

When inflation is structural (3.5%–5%) and the 10-Year Treasury is capped by the Fed’s inability to allow a debt-service spiral, we enter a Negative Real Yield environment. If a bond yields 4% but inflation is 5%, the holder is guaranteed a 1% loss in purchasing power annually.

Suddenly, Gold’s 0% yield is no longer a liability—it is a 100 basis point outperformance over the "risk-free" alternative.

Duration Risk vs. The Zero-Duration Hedge

Bonds currently face a "convexity trap." If inflation remains sticky, yields must eventually rise to attract buyers, causing a decline in bond prices (duration risk). If the Fed intervenes to suppress yields (Yield Curve Control), the currency devalues (inflation risk).

Gold solves this dilemma because it carries zero duration:

In a hawkish shock: Gold may face temporary headwinds, but it does not have a "maturity" that can be repriced to zero.

In a dovish pivot: If the Fed chooses to "save the economy" over "saving the dollar," gold acts as the ultimate denominator of value.

The Institutional Floor: No Counterparty Risk

In an era of intensifying geopolitical friction and the "weaponization" of the dollar, the professional manager must account for Counterparty Risk. A Treasury bond is a promise from a government that is currently running a 7% deficit-to-GDP ratio. Gold is the only Tier-1 reserve asset that is not someone else’s liability.

As we move further into 2026, the "Math of Repression" suggests that the volatility of gold is a small price to pay for protection against the guaranteed mathematical decay of fixed income.

Key takeaway for the Investment Committee: We are not buying gold because we expect a "moonshot" in price; we are buying it because the "40" in our 60/40 has become a melting ice cube. Zero yield is a sanctuary when the alternative is a negative real return.

Integrating Gold into the Modern Portfolio

For the modern portfolio manager, the challenge of 2026 is not just seeking returns, but solving the diversification decay inherent in the traditional 60/40 split. If the "40" (fixed income) is now positively correlated with the "60" (equities) during inflationary shocks, the portfolio's realized volatility will consistently exceed its target. To restore the efficient frontier, we must pivot toward assets with a low-to-negative correlation to the entire stock-bond complex.

From Nominal Hedges to Correlation-Adjusted Diversification

In a regime of Fiscal Dominance, where central banks are forced to prioritize government solvency over inflation targets, gold functions as a unique "zero-yield" anchor. Unlike bonds, gold carries no duration risk and no counterparty risk.

When analyzing the current landscape, the implementation of a "10% Gold Shift" serves three primary institutional functions:

Volatility Dampening in Positive Correlation Regimes: Historical backtesting shows that during periods where CPI > 3%, the correlation between equities and Treasuries tends to flip positive. In these windows, gold often acts as the only liquid asset with a near-zero correlation to both, effectively lowering the portfolio's aggregate standard deviation.

The "Real Yield" Buffer: As we face a structural era of negative real yields—where nominal rates lag behind realized inflation to "inflate away" the debt-to-GDP ratio—the opportunity cost of holding a non-yielding asset disappears. In this context, gold's 0% yield is technically superior to a bond’s negative real yield.

Institutional Social Proof (The Central Bank Floor): We are seeing a historic shift in global reserves. When G7 central banks and emerging market peers increase their gold allocations, they are setting a structural "floor" under the price, transitioning gold from a speculative commodity to a Tier-1 Reserve Asset.

The Tactical Framework: The 50/30/20 or 55/35/10 Model

Moving forward, a "blind" 60/40 allocation is a recipe for uncompensated risk. Advisors should consider a migration toward a modified sleeve approach:

Allocation Component | Traditional 60/40 | The "Regime Shift" 55/35/10 | Rationale |

Equities | 60% | 55% | Slight reduction to account for higher equity risk premiums. |

Fixed Income | 40% | 35% | Reducing duration exposure in a rising/sticky rate environment. |

Gold / Real Assets | 0% | 10% | Creating a "Hard Anchor" to decouple from the stock-bond correlation. |

Conclusion: Gold as Insurance, Not Speculation

The transition to a 10% gold allocation isn't about "timing the market" or betting on a total currency collapse. It is a clinical, mathematical response to the fact that bonds have lost their hedging utility.

By integrating gold, advisors can offer clients a portfolio that is built for the structural reality of the late 2020s: a world where inflation is sticky, debt is high, and the old rules of diversification no longer apply.

To wrap up a high-level technical piece, your "Call to Action" needs to transition from the theoretical risk you just identified to a turnkey operational solution. Professional managers don't just want a thesis; they want a way to execute it without increasing their operational overhead.

Automating the Regime Shift

Identifying a structural shift in the equity-bond correlation is the first step; protecting a book of business against it is the second. For the modern Investment Advisor, the challenge isn't just knowing that the 60/40 is broken—it’s the manual burden of rebalancing into a new, complex "Inflationary Regime" model across hundreds of client accounts.

This is where Surmount Wealth changes the math.

Surmount Wealth provides the institutional-grade infrastructure to turn your market conviction into automated reality. Whether you are looking to deploy our Prebuilt Systematic Strategies—designed to thrive in positive correlation environments—or you want to build a Custom Automated Strategy based on your own proprietary indicators, our platform handles the heavy lifting.

Why Portfolio Managers are Scaling with Surmount:

Automate Any Thesis: Convert your view on negative real yields or gold-to-equity ratios into a live, rule-based trading strategy.

Remove Emotional Slippage: Replace manual "gut-check" trades with systematic execution that adheres to your risk parameters 24/7.

Institutional Scalability: Manage complex, multi-asset rotations (Equities, Gold, Commodities) with the precision of a quantitative hedge fund, but with the ease of a unified dashboard.

Dynamic Rebalancing: As correlations shift, your portfolio should too. Surmount allows for sophisticated triggers that traditional "static" platforms simply can’t match.

The 60/40 era is over. The era of the Systematic Alpha is here.

Don’t let your clients’ capital sit in a legacy model that history has already left behind. See how Surmount Wealth can automate your transition to the new macroeconomic reality.

[Book a Demo with the Surmount Team Today]

Join the vanguard of advisors moving from passive observers to systematic leaders.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.