Blog

Recency Bias in Portfolio Management: A Framework for Advisors Under Client Pressure

There is a particular kind of pressure that portfolio managers know well. A sector you hold conviction on has underperformed for eighteen months. The client calls. They have been reading the headlines. They want to know why you haven't rotated out. This is not a portfolio problem. It is a behavioral one, and it starts with recency bias.

Benjamin Graham warned decades ago that rational analysis is routinely displaced by emotion. What he described as market enthusiasm acting as an "artificial stimulant" is, in modern behavioral finance terms, largely a recency bias problem. For advisors managing sophisticated clients, understanding this bias (and knowing how to address it clinically) is as important as the underlying investment thesis itself.

How Recency Bias Distorts Client Perception of Sector Underperformance

The Availability Heuristic and Its Effect on Investment Decisions

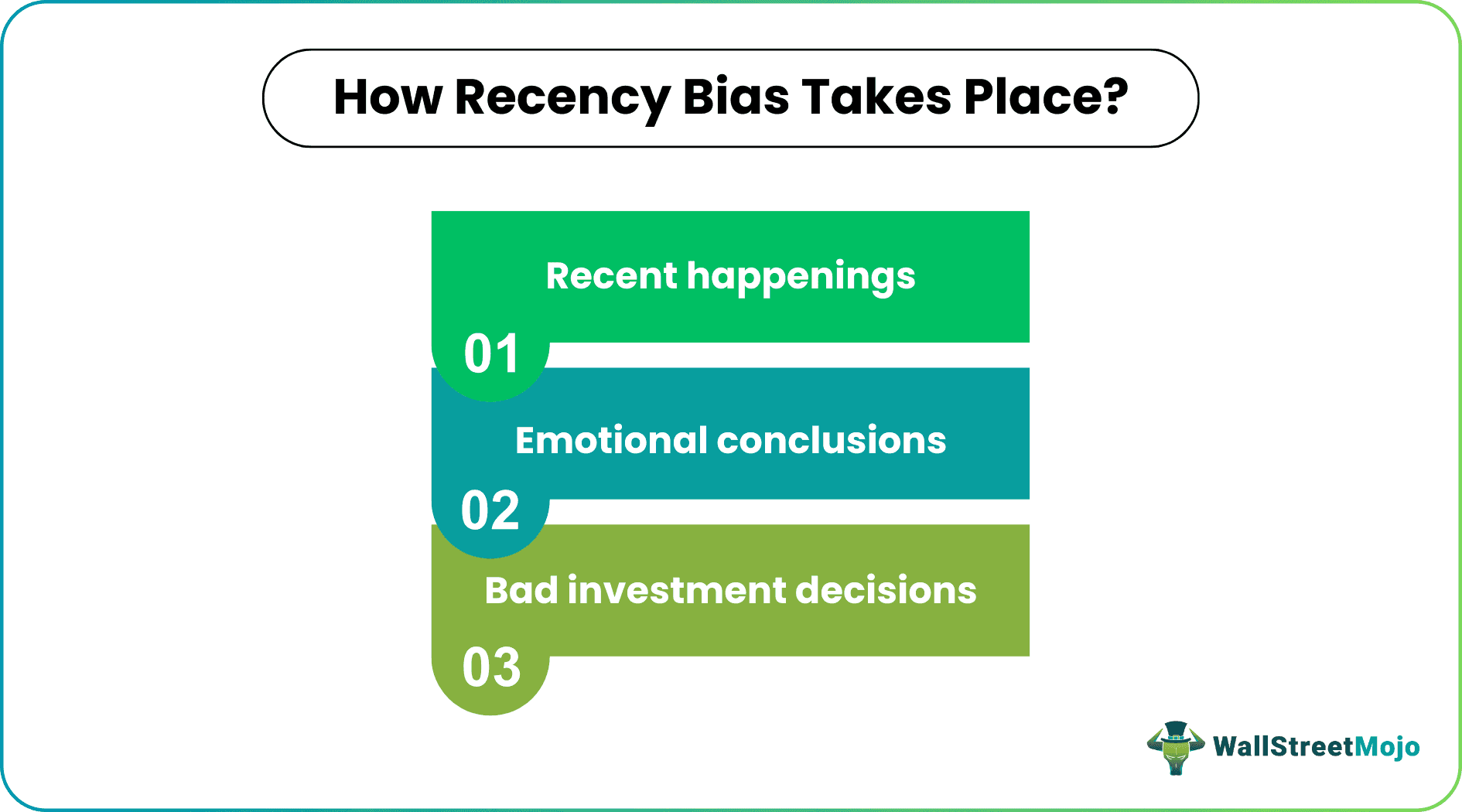

Recency bias is a derivative of what Daniel Kahneman identified as the availability heuristic, which is the cognitive tendency to assign weight more heavily to easily recalled information when making judgments. In investment decisions, this means recent performance dominates the client's mental model of a sector, regardless of whether that performance reflects structural reality or cyclical sentiment.

When technology stocks outperform for three consecutive years, clients do not experience that as a data point. They experience it as evidence. The underperforming sector, by contrast, accumulates a narrative of failure that feels permanent even when the fundamentals say otherwise.

Why Prolonged Sector Underperformance Recovery Is Invisible to Clients Anchored in Recent Returns

The deeper problem is timing asymmetry. Prolonged sector underperformance recovery tends to be slow, uneven, and easy to dismiss in its early stages. Clients anchored in recent returns often miss the inflection point entirely because the signals that matter most (such as replacement cost dynamics, supply constraint data, re-leasing spread trends) are not headline news. They sit in earnings transcripts and investor presentations, not Bloomberg alerts.

This is precisely why sector rotation behavioral bias accelerates at the worst possible moment. Clients push hardest to exit just as the structural case is quietly strengthening.

Sector Rotation Behavioral Bias: When Clients Confuse Momentum for Fundamentals

Momentum is not a thesis. It is a condition. Advisors who allow clients to conflate the two will find themselves perpetually rotating into yesterday's trade. The advisor's role here is not to capitulate to recency-driven pressure but to slow the conversation down and reintroduce the distinction between price performance and fundamental value. That distinction is the foundation of everything that follows.

Mean Reversion vs. Broken Thesis

How to Defend an Underperforming Sector Allocation With Structural Evidence

Defending an underperforming sector allocation is not about stubbornness. It requires a clear, documented framework that separates sentiment from structure. The advisor should be able to answer one question precisely: has anything changed in the underlying investment thesis, or has only the price changed?

If the answer is the latter, the conversation shifts from defense to education. Structural evidence — rising replacement costs, declining new supply, improving re-leasing spreads — gives the client something to evaluate rather than simply a manager's conviction to either trust or distrust. Evidence-based portfolio management removes personality from the equation, which is exactly where it should not be.

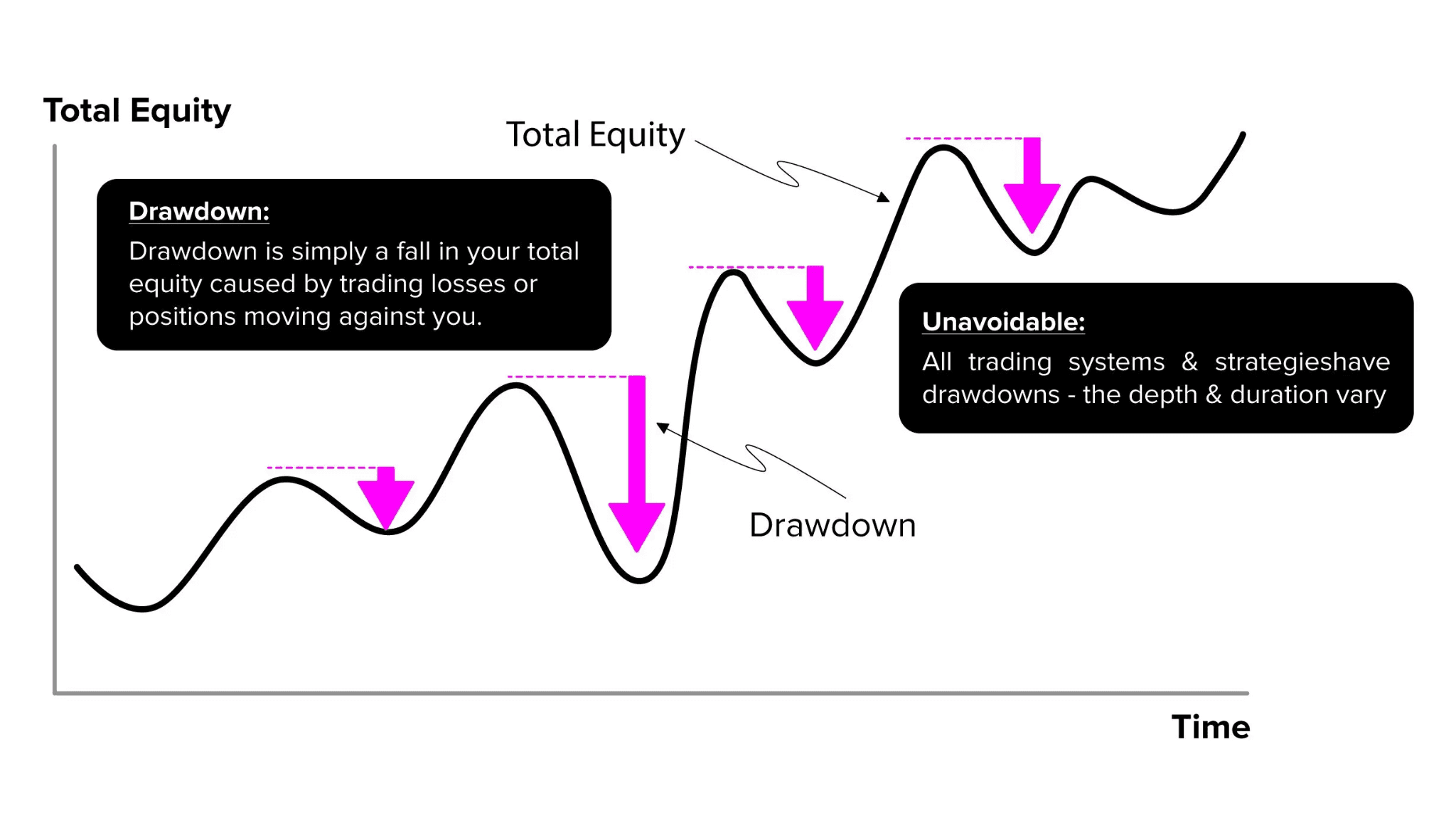

Distinguishing Cyclical Drawdown From Structural Breakdown in Client Conversations

This mean reversion approach is the analytical hinge of the entire framework. A cyclical drawdown is a price phenomenon driven by sentiment, capital rotation, or macro conditions that do not impair the long-term earnings trajectory of the underlying assets. A structural breakdown is different — it means the thesis itself is impaired, the competitive dynamics have shifted permanently, or the earnings model no longer holds.

Advisors who can articulate this distinction clearly (and back it with data) transform a client anxiety conversation into a rigorous investment review. That shift in framing protects both the relationship and the portfolio.

Evidence-Based Portfolio Management as a Bulwark Against Emotional Decision-Making

The most durable protection against recency bias — for both the advisor and the client — is a written investment framework established before performance pressure arrives. When the criteria for holding, adding, or exiting a position are documented in advance, the client's emotional state in month eighteen of underperformance carries less weight. The framework becomes the reference point, not the recent return chart.

Managing Advisor Conviction vs. Client Pressure Without Losing the Relationship

How to Explain Sector Underperformance to Clients Using Behavioral Language

Most clients respond better to behavioral framing than to valuation lectures. Rather than leading with price-to-NAV discounts or replacement cost multiples, begin by naming the bias directly. Explaining that recency bias is a well-documented cognitive pattern — one that affects professional investors and retail clients alike — normalizes the client's discomfort without validating the impulse to act on it.

This positions the advisor as a behavioral coach as much as a capital allocator, which is increasingly where long-term client value is created.

When to Hold and When to Capitulate — A Decision Framework for Institutional Investors

Conviction is not unconditional. Advisors managing institutional investors need a pre-defined set of conditions that would genuinely warrant a thesis revision. These might include a sustained deterioration in sector fundamentals, a material change in the regulatory environment, or a re-rating of the risk premium that invalidates the original entry logic.

When none of those conditions are met, client pressure alone is not a sufficient reason to exit. Documenting this threshold in advance — and sharing it with the client — transforms capitulation from a relationship management tool into what it should be: a disciplined analytical conclusion.

Client Pushback on Underperforming Allocation — Scripts, Signals and Boundaries

When client pushback on underperforming allocation escalates, advisors need both language and boundaries. The language: "The price has moved against us, but the thesis has not changed. Here is the specific evidence I am monitoring." The boundary: distinguishing between a client who is processing anxiety and one whose risk tolerance has genuinely shifted. The latter requires a portfolio response. The former requires a conversation.

The advisor who can hold that distinction under pressure is not just managing a portfolio. They are managing the behavioral gap between what markets do in the short term and what well-constructed portfolios are built to deliver over time.

Stop Watching Behavioral Bias Erode Client Returns. Automate the Discipline Instead.

The framework described in this article only works if it is actually followed. That is harder than it sounds. Even the most rigorous advisors face moments where client pressure, market noise, or cognitive fatigue compromise the systematic discipline that separates long-term outperformance from reactive portfolio management.

This is exactly the problem Surmount Wealth was built to solve.

Surmount's platform lets advisors and portfolio managers build, deploy, and scale automated trade strategies (prebuilt or fully customized) that execute your investment thesis without emotional interference. The framework lives in the strategy. The discipline is enforced by the system. Client pressure becomes a conversation, not a trigger.

Prebuilt Strategies or Build Your Own — The Thesis Drives Everything

Whether you want to deploy a ready-made strategy or codify your own proprietary view of the market, Surmount gives you the infrastructure to do it. Any thesis. Any sector. Any set of entry, exit, and rebalancing conditions you define.

To make this concrete, consider a hypothetical strategy we might call the Contrarian Real Asset Re-rating Strategy (this is an illustrative concept only, not a live or offered strategy):

The strategy systematically allocates to real asset sectors exhibiting prolonged underperformance relative to a broad equity benchmark, weighted by a composite score of replacement cost trends, new supply data, and re-leasing spread momentum. Position sizing increases as valuation discounts widen, and the strategy enforces a rules-based hold discipline that ignores short-term price performance below a defined fundamental deterioration threshold. Rebalancing is triggered by thesis signals, not client sentiment.

That is the entire argument of this article — translated into an automated, executable strategy. No behavioral drift. No capitulation under pressure. No eighteen-month performance review derailing a three-year thesis.

This is what Surmount makes possible.

Why Advisors Are Moving to Automated Strategy Execution

Removes emotional decision-making at the execution layer, where it does the most damage

Scales your conviction across client accounts without manual rebalancing overhead

Documents the thesis in a way clients can see, understand, and hold you accountable to

Responds to signals, not sentiment — exactly what behavioral finance says portfolios should do

The Advisor Who Systematizes Wins. Book Your Demo Today.

The behavioral edge is real. But it only compounds if the infrastructure supports it. Advisors who systematize their highest-conviction ideas — rather than managing them manually under pressure — are the ones who deliver consistent, defensible outcomes over full market cycles.

See what your thesis looks like as an automated strategy.

👉 Book a Demo with Surmount Wealth Now — and bring your highest-conviction idea to the conversation. Their team will show you exactly how to turn it into a rules-based, automated strategy your entire book can benefit from.

Because the best investment framework in the world is only as good as your ability to execute it without flinching.