Blog

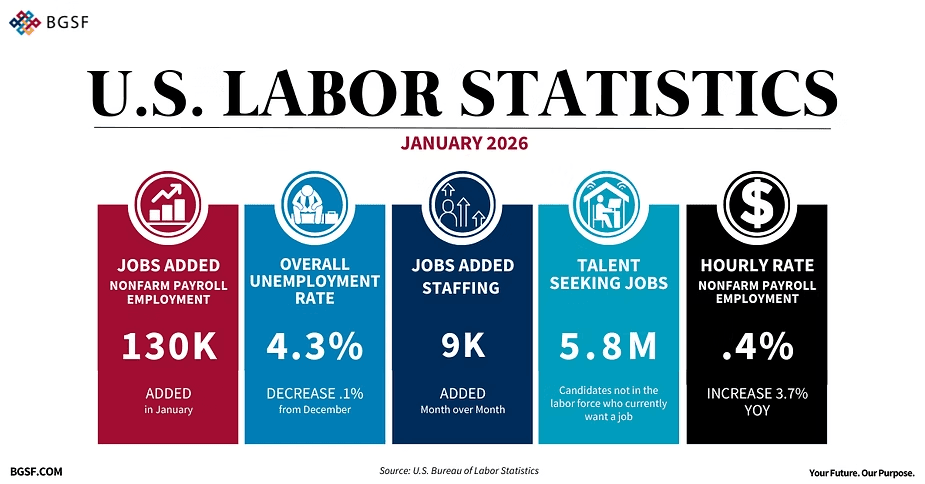

Earlier this week, the Bureau of Labor Statistics released the latest monthly Payrolls Employment Report for January, and the numbers surprised many analysts by coming in stronger than expected. Employers added a surprising 130,000 jobs to the economy, during the year, which was nearly double the 70,000 many economists expected. Moreover, the unemployment rate edged down to 4.3%, reinforcing the narrative of a labor market that, at least on the surface, continues to defy pessimistic forecasts.

Understandably, the market was looking confident about the prospects of the US economy, and as a result of this confidence, the recent gold rally that had been picking up finally lost momentum.

However, beneath the headline strength lies a far more nuanced picture.

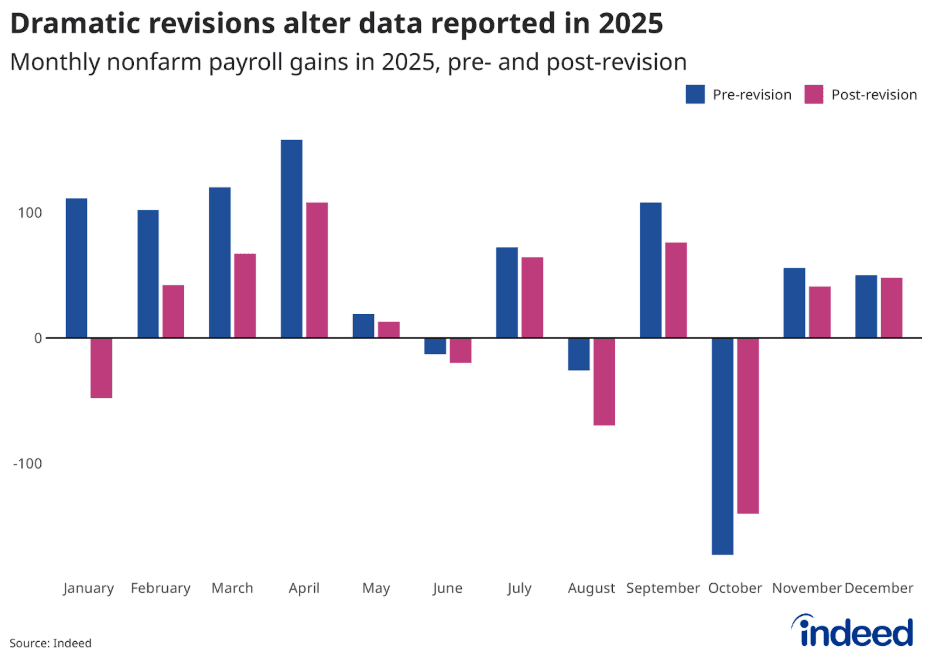

While 130,000 new jobs sounds like a robust recovery, the report also contained a massive data "trap": annual benchmark revisions slashed nearly 900,000 jobs from the previous year’s tallies (ending March 2025), revealing that the labor market was much softer in 2025 than we realized.

Furthermore, the January "beat" was almost entirely driven by a single engine. Of those 130,000 jobs, a staggering 124,000 came from the private sector—and nearly all of those were in healthcare and social assistance.

Federal Reserve governor Chris Waller said regarding this that "this does not remotely look like a healthy labor market".

The Rise of the Care Economy

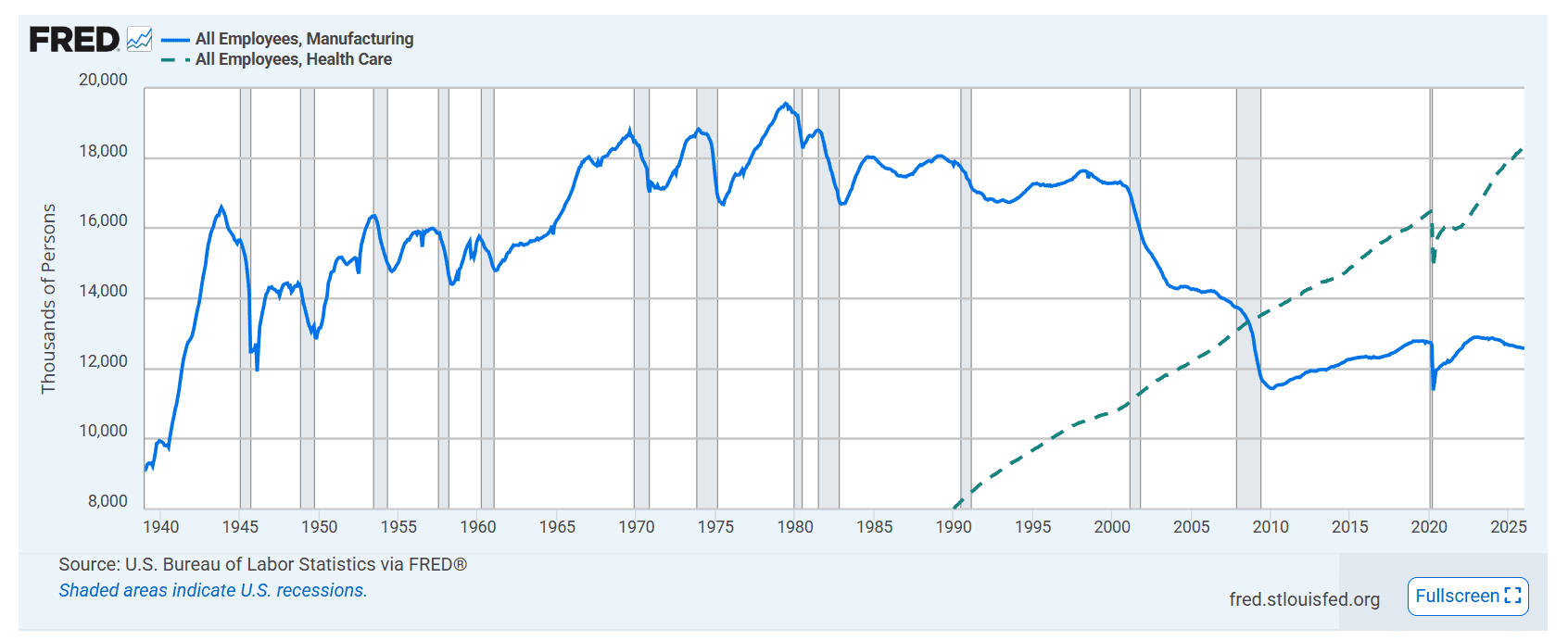

Perhaps one of the most widely discussed takeaways from the labor report was not just the numbers pertaining to the payrolls, but where those jobs are actually being created. An overwhelming 95% of the new job creation was attributed to the healthcare sector and related services, reinforcing a structural shift that has been unfolding for decades.

Currently, the gap between healthcare jobs (over 18.4 million) and manufacturing jobs (nearly 12.6 million) is at the widest it has ever been:

The rise of the care economy is not cyclical noise. It is demographic destiny. An aging population mechanically increases demand for medical services, long-term care, outpatient facilities, home health support, and the broader ecosystem that surrounds them.

Unlike manufacturing, where productivity gains often reduce labor intensity, healthcare remains structurally labor heavy. As a result, employment growth in this sector tends to be persistent rather than speculative.

However, this shift is far from an outcome of doom and gloom. As one of the most resilient sectors in the economy, healthcare acts as a significant "shock absorber" for the economy by providing stability, maintaining productivity, and driving employment during periods of economic downturn or crisis:

Stability over Scalability: A hospital’s profits are predictable but capped by beds and staff. A software firm's profits are high but depend on R&D, not physical factories.

The Result: We see fewer "boom-bust" spikes in Capex (Capital Expenditure). Economic growth becomes slower, steadier, and less prone to the dramatic "V-shaped" recoveries of the past.

Similarly, as we saw in 2024 and 2025, even as the private sector cooled, government spending (especially through Medicare/Medicaid and infrastructure bills) acted as a floor for employment. In a service-heavy economy, the government effectively "subsidizes" the labor market through social transfers.

As the US labor market is continuously dominated by the healthcare sector, it would essentially become less sensitive to global commodity price shocks and more sensitive to global interest rate differentials.

The "Service-Alpha" Strategy

For an investor, the goal is to shift from "timing the cycle" to "positioning for persistence."

Lower Volatility, Higher Multiples: Companies in the "Care Economy" (Healthcare, Education, Specialized Services) often trade at higher P/E multiples because their earnings are seen as a "bond-like" utility. In a 2026 environment of fluctuating rates, these are your anchors.

The "Human Capital" Hedge: Since these sectors are labor-intensive, look for firms with the best retention metrics. In a secular labor shortage, the company that keeps its nurses and engineers wins, regardless of the Fed’s next move.

Watch the "Service PMIs" over "Manufacturing PMIs": Traditional investors still obsess over the ISM Manufacturing Index. Modern investors should prioritize the Services PMI. If Services stay above 50, a "technical recession" is unlikely to feel like a "real-world" depression.

The reason the "recession of 2025" never fully materialized—despite high rates—is partially due to this employment shift. You cannot "fire" the person caring for an aging population as easily as you can shut down a car plant. This structural "stickiness" is the new foundation of U.S. economic resilience.

Positioning for Structural Resilience

In an economy increasingly anchored by services, healthcare expansion, and structurally persistent demand, resilience is no longer optional.

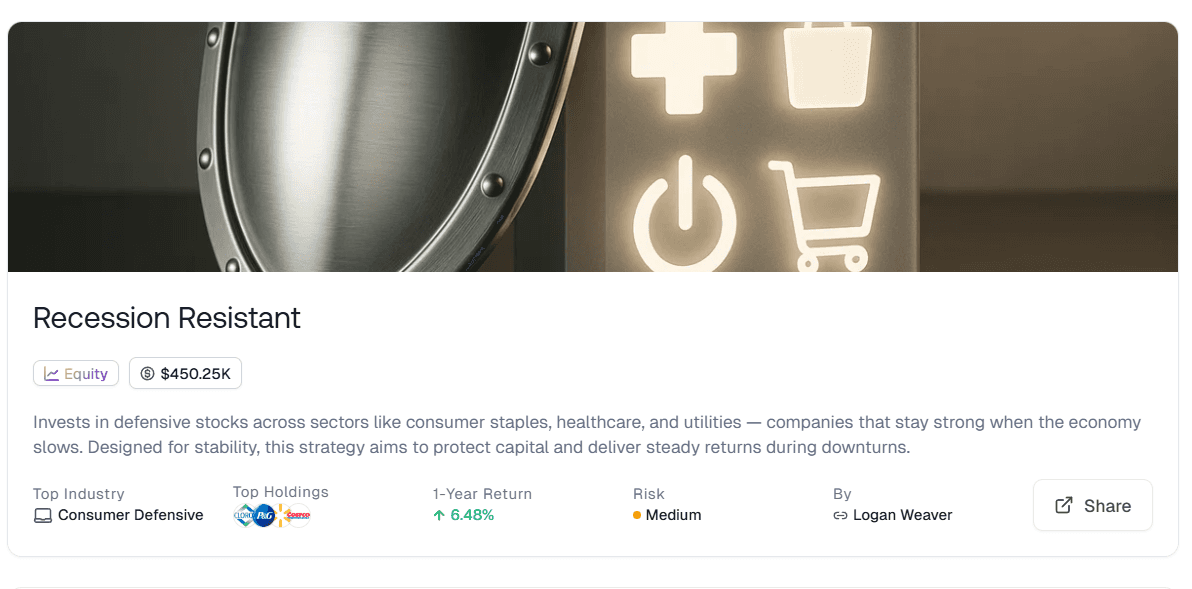

Surmount’s Recession Resistant Strategy aligns with this new reality by emphasizing durability over speculation and consistency over cyclicality. As growth becomes steadier and less boom driven, portfolios must adapt to sectors that benefit from demographic momentum and essential spending patterns.

This approach is not about chasing rallies but about compounding through uncertainty. By prioritizing quality balance sheets, dependable cash flows, and diversified defensive exposure, the Surmount Strategy positions investors to stay invested confidently, regardless of the next headline or macro shock.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.