Blog

Equity Risk Premium 2026: Are Stocks Still Worth the Risk?

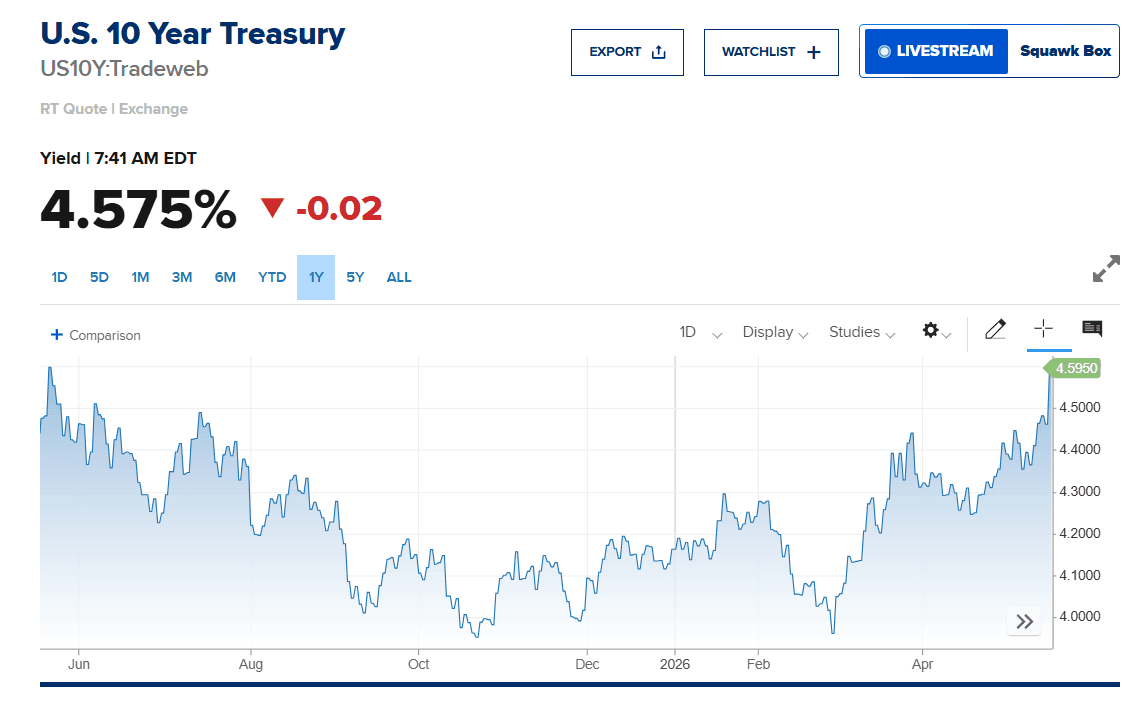

With 10-year Treasury yields above 4.5% and the S&P 500 trading near all-time highs, the equity risk premium has compressed to levels that should give every portfolio manager pause.

What the Equity Risk Premium Is Actually Telling Us in 2026

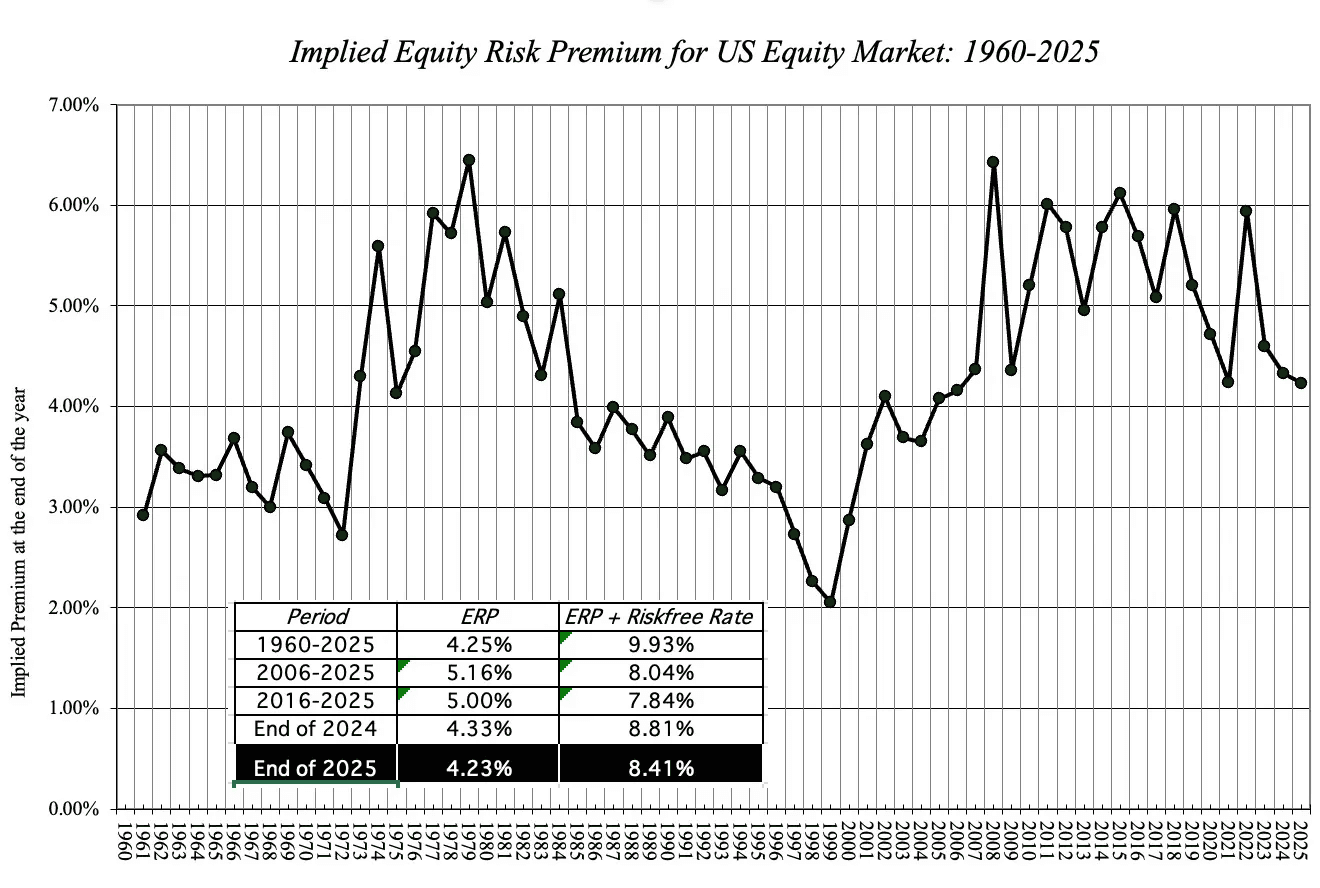

The equity risk premium, which is the excess return investors demand for holding equities over risk-free government bonds, is one of the most fundamental gauges of market valuation. It is not a sentiment indicator or a technical signal. It is a rational expression of whether the market is compensating you for the additional risk you are absorbing by owning stocks rather than Treasuries.

In 2026, that signal is deeply uncomfortable. Despite record earnings from a handful of large-cap technology companies and a relentless AI-driven narrative, the broader market's ERP has compressed to levels that are historically unusual and, in certain segments, has turned outright negative.

For investment professionals, the implication is straightforward: many parts of the U.S. equity market are no longer offering a meaningful premium over what you can earn, with considerably less risk, in government bonds.

"The market is not necessarily wrong to be optimistic. But optimism priced to perfection offers no margin of safety — and margin of safety is what separates investing from speculation."

S&P 500 Earnings Yield vs Treasury Yield: The Numbers Don't Lie

The simplest way to frame the ERP is through the lens of earnings yield — the inverse of the price-to-earnings ratio — compared to the prevailing risk-free rate. When the earnings yield of the S&P 500 significantly exceeds the 10-year Treasury yield, equities offer a meaningful premium. When the gap narrows or inverts, the risk/reward calculus changes materially.

Here is where we stand today:

A 10 basis point premium over risk-free government bonds is not compensation. It is, for practical purposes, nothing. And that figure represents the broad index average — the picture within specific sectors is considerably worse.

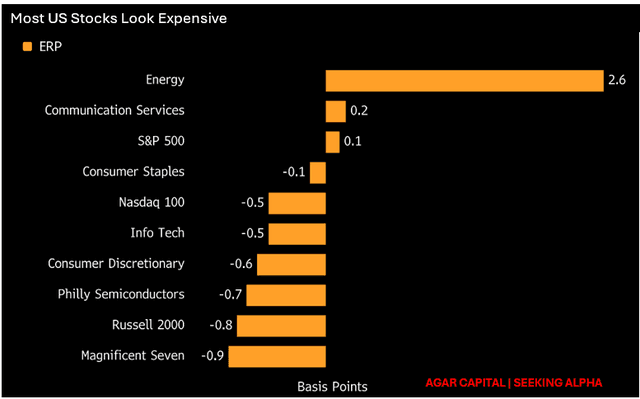

Where the Equity Risk Premium Is Negative

When you disaggregate by sector and market cap, the compression becomes more acute. In the Nasdaq 100, large-cap information technology, semiconductors, and the cohort of mega-cap growth names that dominate index weighting, the earnings yield has fallen below the 10-year Treasury yield. This is a dynamic made more visible when you examine what the growing divergence between cap-weighted and equal-weighted indices is signalling about concentration risk.

A negative equity risk premium does not guarantee an imminent correction. Overvalued markets have remained overvalued for extended periods throughout history — and as we've explored previously, even great businesses can be awful investments when the price paid leaves no buffer. What it does mean is that the buffer between current prices and a valuation-driven pullback is effectively gone.

Any negative surprise — a hotter-than-expected inflation print, a weak Treasury auction, an earnings miss from a heavily-weighted index constituent — can become a catalyst without needing to be catastrophic in its own right.

Equity Duration and Rising Rates: Why Growth Stocks Are Most Exposed

Understanding which parts of the market are most vulnerable requires borrowing a concept from fixed income: duration. In bonds, duration measures price sensitivity to changes in interest rates. The concept translates directly to equities, though it is less commonly applied in practice.

A stock whose value is derived primarily from near-term, current earnings — think a mature consumer staples company with stable, predictable cash flows — has low equity duration. Its valuation is anchored in the present. By contrast, a high-growth technology company whose current price reflects anticipated earnings five, ten, or fifteen years into the future has very high equity duration. The further out those cash flows lie, the more dramatically they are affected when the discount rate rises.

This is not a theoretical concern. In a standard DCF framework, the discount rate directly determines the present value of future cash flows. When 10-year Treasury yields move from 4% to 4.6% — as they have — the cost of capital embedded in every growth stock valuation increases meaningfully. The companies themselves have not changed. Their products, customer bases, and competitive positions remain intact. But the mathematical value of their future earnings, discounted at a higher rate, is lower.

The Philadelphia Semiconductor Index currently trades at approximately 25 times forward earnings against a 10-year historical average closer to 19 times. Sustaining that premium simultaneously requires high growth rates, near-flawless execution, and a stable interest rate environment. The removal of any one of those three conditions creates downside risk. The removal of more than one creates significant downside risk.

Defensive Portfolio Positioning 2026: What a Compressed ERP Demands

For portfolio managers, a near-zero or negative equity risk premium is not a sell signal in isolation. It is, however, a clear signal to be deliberate about where you hold risk, how much of it you hold, and what you are being compensated for bearing it.

The compressed ERP environment of 2026 favors a specific set of equity characteristics: companies with current profitability rather than projected future profitability, asset-light business models with pricing power, recurring revenue with high customer retention, and low sensitivity to capital expenditure cycles and commodity input costs.

These are not glamorous attributes. They do not attract the attention that AI infrastructure narratives attract. But in an environment where the cost of money is rising for reasons connected to inflation and fiscal pressure rather than simply economic strength, these characteristics represent genuine margin of safety — which is precisely what the broader index no longer provides.

Equity Allocation Strategy in a Rising Rate Environment

A practical reallocation framework for the current environment might involve three concurrent shifts: a reduction in overall equity allocation to reduce absolute market exposure; a rotation within equities away from high-beta, long-duration growth names toward profitable, cash-generative businesses with lower valuation multiples; and a measured increase in defensive sector exposure — healthcare, consumer staples, and select software businesses with the economic characteristics described above.

The rationale for maintaining some technology exposure is not naive optimism about AI. It is recognition that not all technology carries equivalent duration risk. A software company generating stable, recurring revenue with minimal capital requirements and strong pricing power behaves, in many respects, more like a value stock than a growth stock. Its valuation is grounded in present and near-term cash flows, not in a projected future that a rising discount rate can erode.

Healthcare and consumer staples deserve attention not as exciting ideas, but as positions that restore premium to a portfolio. Their earnings yields, relative to current Treasury levels, offer the kind of spread that the broad index no longer provides. Their P/E ratios, relative to historical norms, leave room for valuation support rather than valuation risk.

How Systematic Portfolio Management Changes the Equation

The analysis above identifies a coherent, defensible portfolio posture for the current environment. The harder question, for most investment professionals, is execution. "Tactical shifts in allocation — reducing high-beta technology exposure, rotating into defensive sectors, maintaining discipline around rebalancing thresholds — require a level of systematic rigor that is difficult to sustain manually across a broad client book."

This is where algorithm-driven portfolio management becomes genuinely useful, not as a replacement for professional judgment, but as a mechanism for executing that judgment with precision and consistency.

Surmount Wealth is built for exactly this environment. The platform allows investment professionals and self-directed investors to apply institutional-grade allocation strategies and rebalancing logic to existing brokerage accounts — without requiring fund transfers or bespoke coding. Strategy libraries can be configured to respond to the kind of macro signals discussed in this piece: changes in yield spreads, sector rotation signals, valuation threshold triggers. The result is a portfolio that behaves with the discipline the current market demands, consistently and at scale.

In a market where the margin of safety has compressed to near zero in many segments, the ability to act systematically — rather than reactively — is not a technical advantage. It is a risk management imperative.

Frequently Asked Questions

What is the equity risk premium in 2026?

The equity risk premium (ERP) is the excess return equities are expected to deliver over the risk-free rate, typically the 10-year Treasury yield. In 2026, with Treasuries yielding 4.5–4.6%, the S&P 500 ERP has compressed to approximately 0.1% — effectively zero — meaning equities are barely compensating investors for the additional risk they carry over government bonds.

Is the equity risk premium negative right now?

For the broad S&P 500, the equity risk premium in 2026 is marginally positive at roughly 0.1%. In higher-valuation segments — Nasdaq 100, large-cap semiconductors, and mega-cap technology — the ERP is negative. Investors in those segments are currently accepting lower expected returns than U.S. Treasury bonds offer, without the capital safety that government bonds provide.

How do rising Treasury yields affect stock valuations?

Rising Treasury yields increase the discount rate in DCF models, which reduces the present value of future cash flows and compresses justifiable valuation multiples. The effect is sharpest on long-duration growth stocks — companies whose current price reflects earnings projected five to fifteen years out. A move from 4% to 4.6% on the 10-year Treasury meaningfully erodes the value of those distant cash flows, even when the underlying business has not deteriorated.

What is equity duration and why does it matter when rates rise?

Equity duration measures how sensitive a stock's valuation is to interest rate changes, mirroring the duration concept in fixed income. Low equity duration stocks — profitable consumer staples or healthcare companies valued on current earnings — are relatively insulated from rate moves. High equity duration stocks — growth and semiconductor names valued on future cash flows — face significant valuation pressure when rates rise, making them the most exposed segment in the current environment.

What does defensive portfolio positioning look like when the ERP is compressed?

When the equity risk premium is compressed, defensive portfolio positioning in 2026 means rotating toward companies with current profitability, asset-light business models, recurring revenue, and strong pricing power. Healthcare and consumer staples with below-average P/E ratios currently offer a meaningful earnings yield spread over the risk-free rate — something the broad index no longer provides. The objective is not to exit equities entirely but to restore genuine premium back into the portfolio.

How should equity allocation strategy change in a rising rate environment?

In a rising rate environment driven by inflation rather than economic strength, equity allocation strategy should prioritize reducing duration risk across the portfolio. Practically, this means trimming high-multiple growth exposure in semiconductors and speculative AI-adjacent names, while rotating into sectors where valuations are grounded in current cash flows. Healthcare, consumer staples, and profitable software businesses with stable recurring revenue currently offer an equity risk premium the broader market does not. Valuation discipline becomes an active risk management tool.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.