Blog

High-net-worth clients are reshaping the advisory landscape. According to Cerulli Associates, total U.S. household wealth exceeded $90 trillion by year-end 2024—a 16% increase from the prior year—with HNW households controlling $49 trillion, or 54% of the total. For Registered Investment Advisors, this concentration of wealth at the top creates both immense opportunity and intensifying competition.

The stakes are considerable. Cerulli projects the HNW market will grow at 9.3% annually to surpass $30 trillion by 2028. Yet many advisors remain unprepared for the sophisticated planning these clients require. A recent Bank of America Private Bank study found that two-thirds of wealthy Americans work with multiple advisors—a signal that many HNW clients don't feel adequately served by any single firm.

The advisors who capture this market will be those who deliver comprehensive, coordinated strategies across tax optimization, estate planning, and wealth transfer—not just investment management. Here's what's driving HNW planning in 2025 and how forward-thinking RIAs are responding.

Estate Planning Gets a Second Wind After the OBBBA

For much of 2024, estate planners operated under a cloud of uncertainty. The Tax Cuts and Jobs Act's elevated exemptions—$13.99 million per individual in 2025—were scheduled to sunset at year-end 2025, reverting to approximately $7 million per person. Many HNW families rushed to execute gifting strategies before the window closed.

The One Big Beautiful Bill Act, signed into law on July 4, 2025, changed that calculus entirely. According to Morgan Lewis, the legislation permanently increased the federal estate and gift tax exemption to $15 million per person—$30 million for married couples—beginning January 1, 2026, with annual inflation adjustments going forward. Unlike the TCJA, there is no sunset provision.

But the urgency hasn't disappeared—it's shifted. As Mercer Advisors notes, many clients may still benefit from making strategic gifts now to lock in asset growth outside their estates. And with future administrations potentially reducing these exemptions, the prudent approach remains proactive planning.

For RIAs, this represents a pivotal moment to deepen client relationships through estate planning coordination. Firms that connect the dots between investment management, tax strategy, and estate design position themselves as indispensable—especially when clients are evaluating whether one advisor is enough.

Spousal Lifetime Access Trusts Remain a Core Strategy

Among the estate planning tools gaining traction with HNW couples, Spousal Lifetime Access Trusts (SLATs) continue to stand out. A SLAT allows one spouse to transfer assets into an irrevocable trust for the benefit of the other spouse, removing those assets from their combined taxable estate while retaining indirect access to them.

According to Charles Schwab, spouses can transfer up to the federal exemption limit—$13.99 million per individual in 2025, rising to $15 million in 2026—to a SLAT. The trust's assets, plus any future appreciation, remain outside both spouses' estates. For couples with estates exceeding the exemption threshold, this can translate to substantial tax savings.

The strategy requires careful execution. SLATs are irrevocable, meaning assets cannot be returned once transferred. Couples creating dual SLATs for each other must ensure the trusts are sufficiently different to avoid triggering the reciprocal trust doctrine, which could cause the IRS to disregard both trusts for tax purposes. Additionally, assets in a SLAT do not receive a step-up in basis at either spouse's death, creating potential capital gains implications for beneficiaries.

For RIAs, understanding these mechanics—and coordinating with clients' estate attorneys and tax advisors—is essential. The advisor who can facilitate these conversations becomes the central figure in the client's financial life.

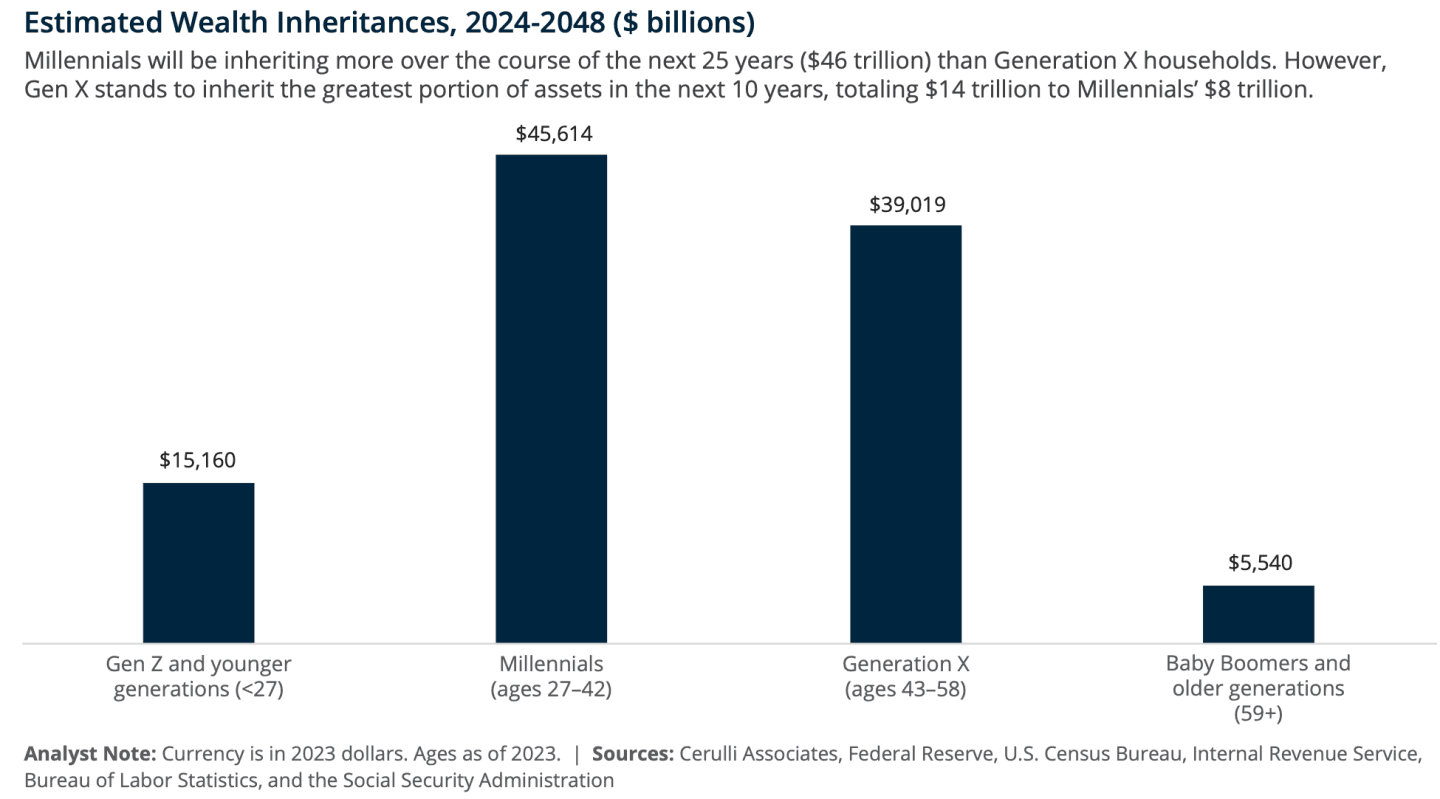

The $124 Trillion Wealth Transfer Demands Multi-Generational Planning

The Great Wealth Transfer is no longer a future event—it's underway. Cerulli projects that $124 trillion will transfer through 2048, with $105 trillion flowing to heirs and $18 trillion to charity. More than half of this total—$62 trillion—will come from just 2% of households: the high-net-worth and ultra-high-net-worth.

The implications for advisory firms are significant. According to Fortune's analysis of Cerulli data, Gen X will inherit nearly $1.4 trillion per year over the next decade, while millennials will ultimately receive the largest share at $45.6 trillion. Younger women will inherit $47 trillion over the next 24 years, fundamentally shifting the demographics of wealth decision-making.

Developing relationships with clients' spouses and children has become a top long-term growth strategy among HNW practices. Nearly 89% of firms surveyed by Cerulli in 2024 cited family meetings and regular communication among family members as a key best practice. The firms that fail to engage the next generation risk losing those relationships entirely when assets transfer.

This is where technology and scalable service models become critical. Advisors cannot hold individualized family meetings with every client household without infrastructure that makes personalization efficient. Platforms that centralize client data, automate routine communications, and surface actionable insights enable advisors to deliver family-office-level service without the corresponding headcount.

Tax Optimization Moves from Differentiator to Table Stakes

For HNW clients, tax minimization is now as important as wealth preservation. According to BlackRock's research on HNW advisory practices, tax minimization ranks alongside wealth preservation as the most important objective for high-net-worth-focused teams.

The strategies are well-established but often underutilized. Annual gifting using the $19,000 per-recipient exclusion in 2025 allows meaningful wealth transfer without reducing lifetime exemption. Qualified charitable distributions from IRAs—up to $108,000 in 2025—enable retirees to satisfy required minimum distributions while avoiding taxable income. Roth conversions during lower-income years create tax-free growth that compounds over decades.

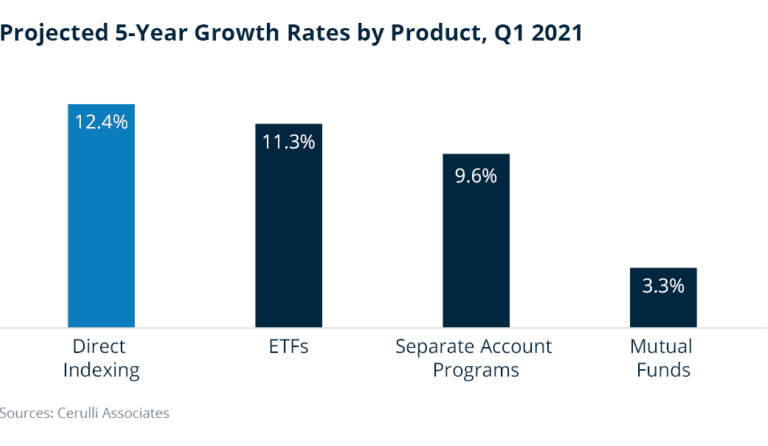

Tax-loss harvesting has become particularly powerful when paired with direct indexing. According to Russell Investments, Cerulli projects direct indexing assets will grow at 12.4% annually, outpacing mutual funds and ETFs, reaching $800 billion by year-end 2026. Direct indexing ended 2024 with $865 billion in assets, per InvestmentNews.

The appeal is straightforward: by owning individual securities rather than funds, investors can harvest losses at the position level throughout the year—even when the broader market rises. For a $2 million portfolio, industry analysis suggests this approach could capture $100,000 to $400,000 in harvested losses during volatile periods like 2025, compared to roughly $115,000 maximum from a traditional index fund approach.

Yet only 14% of financial advisors actively use direct indexing, per Cerulli. The gap between adoption and opportunity is substantial—and represents a competitive advantage for firms that can deliver these capabilities at scale.

Technology Enables Scalable Sophistication

The operational challenge facing RIAs is clear: HNW clients demand increasingly personalized service, but delivering that service through manual processes doesn't scale. The solution lies in technology infrastructure that automates routine tasks while surfacing the insights that drive client value.

According to the 2025 Charles Schwab RIA Benchmarking Study, firms of all sizes saw significant growth in 2024, with AUM increasing by 16.6% and client growth up 4.8%. A major driver: strategic technology adoption. The Advisor360° RIA Connected Wealth Report found that generative AI and automation are being rapidly adopted across the RIA space—not as novelties, but as the new standard for streamlining meeting prep, automating compliance tasks, and reducing administrative burdens.

Client relationship management and workflow automation tools are improving advisor productivity and client engagement. API integrations are centralizing client data, improving reporting accuracy, and providing holistic portfolio views. Digital onboarding platforms are streamlining client acquisition. The Goldman Sachs RIA Professional Investor Forum highlighted these capabilities as essential for RIAs seeking to remain competitive.

The firms winning in the HNW space aren't simply adopting technology—they're building integrated platforms where data flows seamlessly between planning, portfolio management, and client communication. This infrastructure enables advisors to deliver sophisticated strategies like tax-loss harvesting, asset location optimization, and coordinated estate planning without drowning in operational complexity.

Building the Modern HNW Practice

The path forward for RIAs serving high-net-worth clients requires excellence on multiple fronts simultaneously. Investment management remains foundational, but it's no longer sufficient. Tax optimization, estate planning coordination, and multi-generational relationship building have become essential capabilities.

The firms that thrive will be those that pair deep planning expertise with scalable technology infrastructure. They'll deliver personalized, tax-aware strategies to every client—not just the top tier—because their systems make that level of service efficient. They'll engage family members proactively, recognizing that the $124 trillion wealth transfer will reward firms that build relationships before assets move. And they'll position themselves as the central coordinator across clients' advisory teams, becoming the one firm that wealthy clients turn to first.

The HNW opportunity is substantial and growing. The question for RIAs is whether they have the infrastructure to capture it.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.