Blog

Personalization at Scale: How to Deliver Custom Portfolios to 500+ Clients

Every RIA faces the same fundamental tension: clients increasingly demand personalized investment strategies tailored to their unique tax situations, values, and financial goals—yet delivering true customization across hundreds of accounts threatens to overwhelm even the most efficient operations.

This is the personalization paradox. And it's becoming the defining challenge for growth-oriented advisory firms.

According to Capgemini's wealth management research, 72% of high-net-worth individuals now expect personalized products and services from their advisors. Meanwhile, McKinsey reports that 76% of clients would consider switching financial advisors to gain access to more personalized wealth management services. The message is clear: personalization isn't a nice-to-have—it's a competitive imperative.

Yet the operational reality remains daunting. Kitces Research found that financial advisors spend only about 20% of their time actually meeting with clients. How do you scale personalization when advisors are already stretched thin?

The answer lies at the intersection of technology architecture, systematic processes, and strategic prioritization. Here's how leading RIAs are solving the personalization paradox.

The Economics of the Personalization Challenge

The fundamental problem is one of operational leverage. Traditional portfolio management approaches fall into two extremes: standardized model portfolios that sacrifice personalization for efficiency, or fully custom portfolios that deliver personalization but collapse under their own complexity.

A 2024 KKR RIA Forum survey captured this tension precisely. Among RIA respondents, 53% reported using a hybrid approach—combining standardized models with targeted customization. Only 28% create fully customized portfolios for each client, while 19% make only minor tweaks to standardized models.

The hybrid approach is scalable yet flexible, making it suitable for a broad client base. But "hybrid" is a spectrum, not a solution. The firms winning on personalization are those deploying specific technologies that automate the customization process itself. According to Cerulli Associates, direct indexing assets reached $864.3 billion in 2024—nearly doubling from 2021 levels with a 22.4% CAGR.

Technology Solutions: Model Portfolios Plus Customization Engines

The first breakthrough comes from reconceptualizing what a "model portfolio" actually is. Rather than a static allocation, modern portfolio infrastructure treats models as starting points—base configurations that can be systematically modified based on client-specific parameters.

The Rise of Model Portfolio Infrastructure

Model portfolio adoption has accelerated dramatically. Cerulli Associates reports that total model portfolio assets climbed to $2.5 trillion by year-end 2024, up from $2.1 trillion in 2023. More telling: 34% of advisors who outsource portfolio construction expect to increase their use of model portfolios over the next 12 months.

Cerulli's 2024 research found that 65% of model provider firms now list custom models among their top three product development priorities—and 30% of model assets are already in custom arrangements. The key shift is that 65% of model provider firms now list custom models among their top three product development priorities. These aren't cookie-cutter solutions—they're frameworks designed for systematic personalization.

Direct Indexing: Personalization at the Security Level

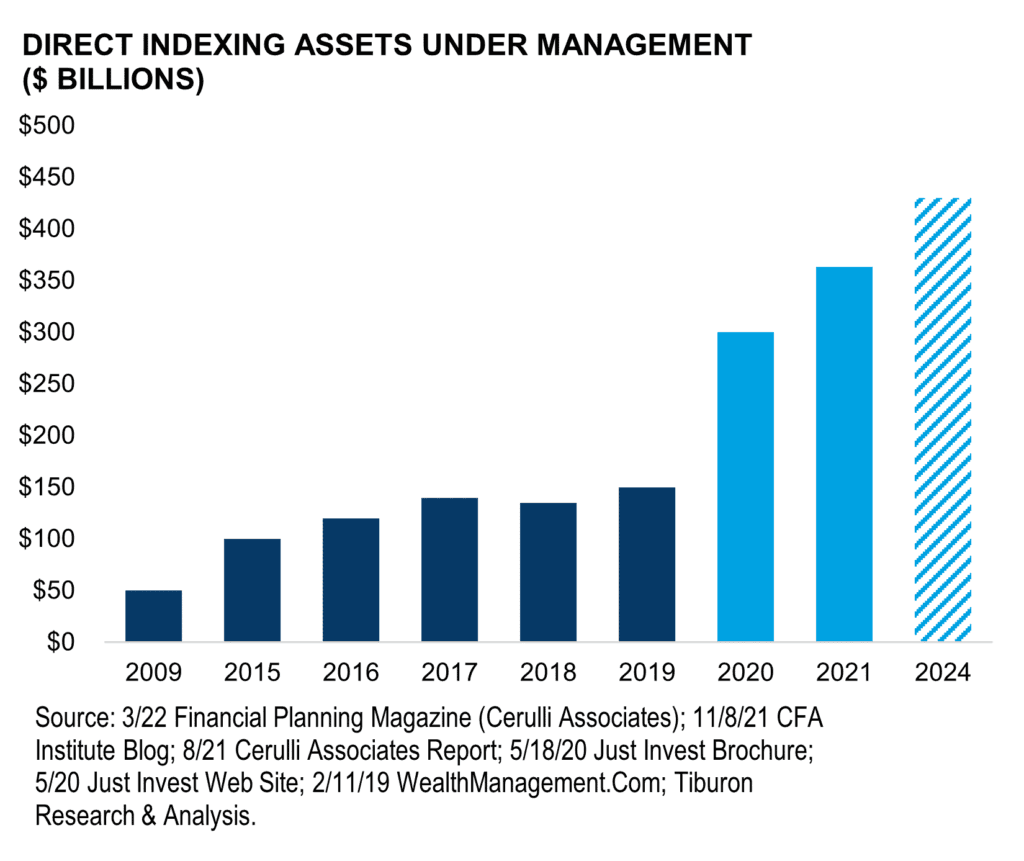

The most powerful tool for scaled personalization is direct indexing—owning individual securities rather than fund shares to enable security-level customization and tax management.

Cerulli Associates reports that direct indexing assets reached $864.3 billion by year-end 2024, nearly doubling from 2021 levels at a compound annual growth rate of 22.4%. Direct indexing strategies now account for 37.6% of manager-traded assets reported by SMA asset managers, more than doubling since 2020.

What makes direct indexing transformative for personalization? Consider the capabilities:

Tax-loss harvesting at the individual security level

ESG and values-based exclusions without tracking error penalties

Concentrated position management for executives with company stock

Factor tilts based on client-specific risk preferences

Charitable giving optimization through appreciated share donation

The barriers to entry have fallen substantially. Fractional share trading now enables direct indexing solutions with minimums as low as $5,000, down from the historical $1 million thresholds. This democratization means RIAs can extend genuine customization to mass affluent clients, not just ultra-high-net-worth households.

Yet adoption remains limited. Only 18% of advisors reported using direct indexing in 2024, up modestly from 16% in 2023. Perhaps more striking: 26% of advisors choose not to use it despite having access, and 12% don't know what it is. The education gap represents both a challenge and an opportunity for differentiation.

Tax Overlay Management Across Hundreds of Accounts

Tax management may be the most quantifiable value an RIA can deliver—and the most difficult to scale manually. The solution is systematic tax overlay management that applies consistent tax optimization rules across the entire client base while respecting individual circumstances.

The Magnitude of Tax Drag

BlackRock's research found that the average annual tax cost of 1.14% is three times higher than the average portfolio fee of 0.38%. Across U.S. equity funds, 76% of active mutual funds have reported capital gains over the last five years, compared to just 3% of index ETFs and 17% of active ETFs.

This creates a substantial opportunity for advisors who can systematically minimize tax drag. But here's the challenge: effective tax management requires daily monitoring, not year-end reviews.

Continuous Tax-Loss Harvesting

Parametric demonstrates the difference between continuous and calendar-based tax-loss harvesting. In years when markets rise rapidly—like 2023 or 2024—calendar-based harvesting that only reviews portfolios quarterly or annually may miss almost all opportunities to capture losses. Continuous monitoring catches brief volatility windows when losses present themselves.

Year-to-date through Q3 2025, Parametric sold more than $13 billion in market value to realize $330 million in net losses—delivering a potential tax benefit of more than $119 million for their fixed income SMA investors.

Even in strong market years, opportunities exist at the security level. Natixis Investment Managers notes that in 2024, even as the S&P 500 returned 25%, 35% of individual stocks lost money—creating 175 potential tax-loss harvesting opportunities while the overall portfolio gained value.

Household-Level Tax Coordination

Effective tax overlay extends beyond individual accounts to coordinate across a client's entire household—including asset location optimization, wash sale monitoring across accounts, and gain/loss harvesting that considers each spouse's tax situation. Envestnet's tax overlay services exemplify this approach, continuously addressing holistic tax management needs while maintaining portfolio strategy. Cerulli's 2025 Managed Accounts Report shows managed account assets reached $13.7 trillion in 2024, with UMA programs experiencing $257.7 billion in net flows—the highest of any program type.

Unified Managed Accounts: The Architecture for Scale

The vehicle that brings all these capabilities together is the Unified Managed Account (UMA)—a single account structure that consolidates multiple investment sleeves into one cohesive portfolio.

Cerulli Associates reports that managed account assets grew 19.8% to reach $13.7 trillion in 2024. UMA programs experienced the highest net flows at $257.7 billion, followed by SMA programs at $218.4 billion. UMA and SMA programs exhibited five-year compound annual growth rates of 18.7% and 18.3%, respectively.

Why UMAs for personalization at scale? The structure enables:

Sleeve-level management: Allocate to multiple strategies (direct indexing, active equity, fixed income) within a single account

Coordinated tax optimization: Harvest losses across sleeves while avoiding wash sales

Simplified reporting: One consolidated statement instead of multiple account statements

Efficient rebalancing: Coordinate trades across all sleeves to minimize transactions and tax consequences

According to Vestmark, UMA assets are expected to grow approximately 15% annually to nearly $4.6 trillion by the end of 2027. The growth reflects both market appreciation and increasing allocation of managed account flows to unified structures.

The operational efficiency is substantial. Rather than managing five separate accounts for a client—taxable brokerage, IRA, Roth IRA, trust, and joint account—the UMA structure allows coordinated management with household-level visibility.

Risk Management at Scale

Personalization must operate within risk parameters. The challenge is maintaining portfolio discipline across hundreds of customized accounts while respecting each client's individual risk tolerance.

Systematic Risk Monitoring

Modern portfolio management platforms enable rule-based monitoring that alerts advisors when accounts drift outside acceptable parameters:

Drift from target allocation: Automatic alerts when asset class weights exceed tolerance bands

Concentration risk: Flags when individual positions or sectors exceed predetermined limits

Risk score changes: Notifications when portfolio risk metrics shift relative to client risk tolerance

Compliance checks: Automated monitoring for regulatory violations

Schwab's 2024 RIA Benchmarking Study found that 99% of firms use a portfolio management system, 97% have a CRM system, and 93% have a financial planning system. Top-performing RIAs—those in the top 20% of the Firm Performance Index—spend 25% less time annually per client on operations and about 10% more time per client on service.

Risk Budgeting Across Customizations

When implementing client-specific customizations—ESG exclusions, concentrated stock positions, factor tilts—each modification creates tracking error. Sophisticated platforms allow advisors to set tracking error budgets that the optimization engine respects when implementing customizations. A client requesting fossil fuel exclusions, for example, can receive alternative sector exposures to minimize deviation from their target risk profile while respecting the values-based constraint.

Client Communication Strategies

Personalization creates complexity that must be communicated clearly. Clients want customized portfolios, but they also want to understand what they own and why.

Transparency Through Technology

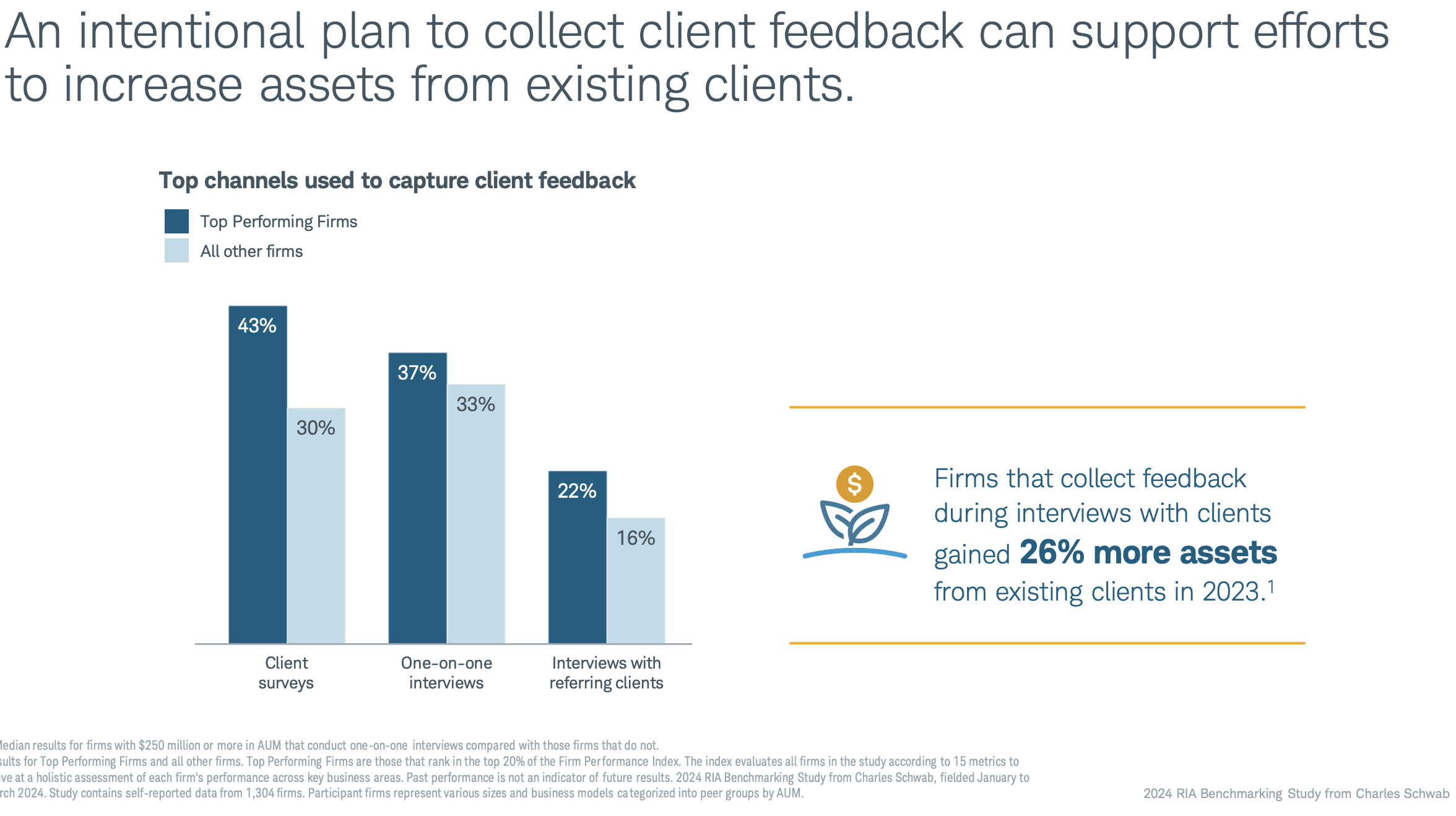

CircleBlack's industry statistics reveal the communication imperative: 85% of high-value clients say more frequent or personalized communication would greatly improve their confidence in their advisor. 88% say it would influence their decision to stay with their advisor. 89% say it would affect how likely they are to recommend that advisor.

Meanwhile, 78% of clients now expect interactive digital experiences—a static quarterly PDF no longer suffices. Schwab's 2024 RIA Benchmarking Study found top-performing RIAs spend 25% less time per client on operations and 10% more on service—demonstrating that technology enables better personalization, not less.

Demonstrating Personalization Value

The most sophisticated RIAs quantify personalization value for each client:

Tax alpha: Calculate actual tax savings from loss harvesting and asset location

Customization impact: Show how ESG exclusions or factor tilts performed relative to unconstrained alternatives

Risk-adjusted returns: Demonstrate how personalized risk management protected during drawdowns

This transparency transforms personalization from an operational cost into a visible value proposition.

Tiered Communication Frameworks

Effective client segmentation aligns communication intensity with client complexity:

Simple portfolios, low-touch preference: Quarterly summary with annual review

Complex situations, detail-oriented: Monthly tax reports, proactive rebalancing notifications

High-net-worth, white-glove service: Real-time access to portfolio analytics, on-demand advisor availability

The key is systematizing these tiers so personalized communication scales with the client base.

The Technology Stack for Personalized Portfolios at Scale

Delivering personalization across 500+ clients requires integrated systems that share data and automate workflows. Franklin Templeton's 2024 survey of 150 RIAs found that 85% see a critical or moderate need for technology to improve day-to-day client service, communication, and data management.

Core Platform Components:

Portfolio management and accounting: Real-time position data, performance attribution, tax lot tracking

Rebalancing engine: Rules-based automation that respects client-specific constraints and tax situations

Trading and execution: Direct integration with custodians for efficient multi-account trading

Client reporting portal: Interactive access to performance, holdings, and planning data

CRM integration: Connect portfolio data with client relationship context

Integration Is Non-Negotiable: Cerulli's research found that data aggregation capabilities rank as the number one factor in advisor technology selection. The 2024 Kitces Research study confirms this: 67% of advisors now use integrated technology stacks rather than standalone solutions, up from 48% in 2022.

Key Data Point: Statista's U.S. Wealth Management Outlook projects assets under management to reach $92.53 trillion in 2025, growing to $101.62 trillion by 2029—underscoring the scale at which personalization must operate.

The Path Forward: Where to Start

For RIAs looking to enhance personalization capabilities, the journey typically progresses through stages:

Stage 1: Model Portfolio Foundation — Establish well-designed model portfolios that serve as baselines for customization across major client segments.

Stage 2: Tax Overlay Implementation — Layer systematic tax management across all taxable accounts, including automated tax-loss harvesting and wash sale monitoring.

Stage 3: Direct Indexing Integration — For clients above appropriate minimums, introduce direct indexing sleeves that enable security-level customization.

Stage 4: UMA Consolidation — Migrate appropriate clients to unified managed account structures that coordinate all sleeves within a single tax-optimized framework.

Stage 5: Personalization at Scale — Systematically extend personalization across the entire client base through automated systems rather than manual workarounds.

The Competitive Advantage

The RIA industry is consolidating. Cerulli reports that RIA consolidators now account for $1.5 trillion in assets under management. Technology is central to this consolidation: 55% of advisors say an integrated technology platform is among the most-valued services offered by a consolidator.

The implication for independent RIAs is clear—your technology infrastructure is now a competitive differentiator. Personalization at scale isn't just about client satisfaction. It's about building an advisory firm that can grow efficiently, demonstrate measurable value, and compete with the resources of larger institutions.

The personalization paradox is real. But it's solvable with us. The RIAs that invest in systematic infrastructure for customization today will be the ones serving 500, 1,000, or 5,000 clients tomorrow—each with a portfolio as personalized as they demand.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.