Blog

The Case for Long-Duration Munis in a Range-Bound Rate Environment

Why the Rate Environment Is the Whole Thesis

Fixed income allocators spent much of 2024 and early 2025 positioning for a rate cutting cycle that was going to solve the duration question for them. The Fed would cut, the long end would rally, and duration would earn both its carry and its capital appreciation. That trade worked — partially, briefly, and not nearly as cleanly as the consensus expected. What allocators are sitting with now is a materially different setup, and the mistake would be to keep running the 2024 playbook into a 2026 macro environment that looks nothing like it.

The current picture seems straightforward from the current vantage point.

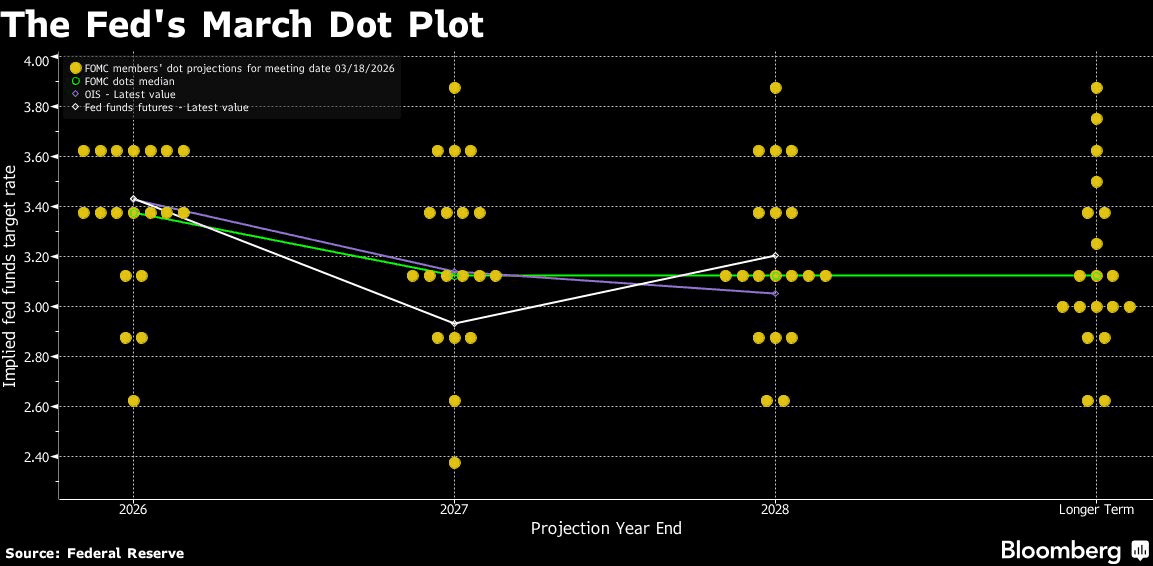

The Fed is on hold. The March SEP dot plot shows one cut in 2026 and one in 2027, with GDP revised upward, PCE and core PCE both revised higher, and unemployment projections that do not suggest the labor market is sending any distress signal.

Nonfarm payrolls continue to print well above consensus. Core CPI disinflation is quietly progressing, but headline noise from energy passthroughs is giving the Fed no political cover to move. The Fed Funds rate is sitting at 3.50% to 3.75%, and the probability of a hold at the next meeting is running in the high eighties to high nineties on CME FedWatch. A wait-and-see Fed, obviously comes with its own set of investing implications.

There is additionally some institutional uncertainty around Fed leadership, which adds another reason for the committee to stay cautious and deliberate rather than move preemptively.

The long end of the Treasury curve has reflected this. The 30-year Treasury is anchored in the 4.75% to 5.0% range. That is a flatter curve than the market was pricing six months ago, and a long end that has proven resistant to both the rate cut optimism of late 2024 and the inflation headline noise of early 2026.

For fixed income allocators, this stability at the long end is not a neutral backdrop. It is, in fact, the structural sweet spot for a specific category of carry trade — one where duration stops being a source of mark-to-market volatility and becomes instead a source of income. When rates stop moving, the question shifts. It is no longer "where are rates going." It is "who is getting paid the most to wait."

The Carry Math: What Duration Actually Earns When the Tape Is Flat

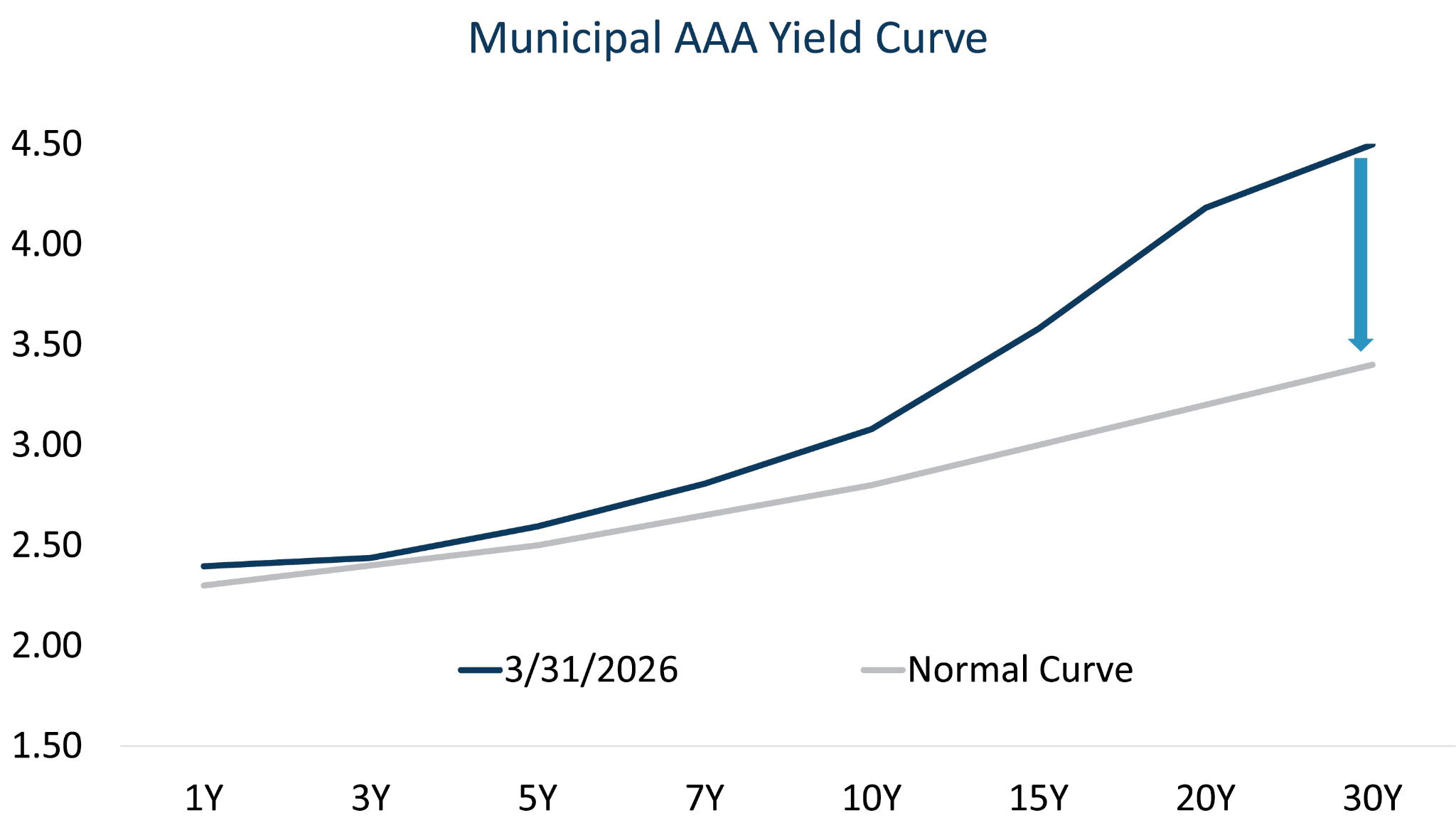

The muni curve is not uniformly attractive in this environment. Muni-to-Treasury ratios on the front and intermediate parts of the curve — the five and ten year segments — are running in the high fifties to low sixties on a percentage basis. That is historically rich. The front end of the muni curve is expensive relative to comparable Treasury duration, and the carry advantage over taxable alternatives is compressed as a result. Allocators chasing munis in the two to ten year range are paying a premium for a credit quality advantage that is not being adequately compensated in yield terms.

The long end tells a different story. The 30-year AAA muni yield is running in the 4.0% to 4.1% range, which puts the muni-to-Treasury ratio in the high eighties — close to historical fair value.

The spread advantage of long-dated munis over comparable corporate fixed income instruments is running over 170 basis points on a tax-equivalent basis at the top federal bracket, before any state tax exemption is factored in. The long end of the muni curve is, at this moment, the only segment of the broader muni market where the relative value case is structurally supported by the data rather than by narrative.

Now bring leverage into the picture. A leveraged muni vehicle running 40% effective leverage against a portfolio with an average duration in the 20 to 21 year range is doing something specific in this rate environment. It is borrowing at short-term rates that are stable — because the Fed is on hold — and deploying that capital into long-duration muni paper that is earning at or near fair value relative to taxable alternatives. The carry spread between the short-term funding cost and the long-end muni yield is the engine of the distribution. When short rates are stable and the long end is range-bound, that engine runs cleanly. There is no meaningful compression from a rate backup, and there is no erosion of the funding cost from a Fed pivot in the wrong direction.

For an investor in the top federal bracket, incorporating the Net Investment Income Tax, the tax-equivalent yield on long-duration muni exposure is already compelling on an unlevered basis. Add state tax exemption for a resident of a high-tax state, and the after-tax yield advantage over investment-grade corporates, preferreds, and BDCs becomes difficult to replicate through any other publicly available instrument. The carry, on an after-tax basis, is not close. A flat tape does not reduce that carry. It simply means the investor is paid that after-tax income without the capital appreciation, which for an income-oriented fixed income allocation is an entirely acceptable outcome.

The Risk Case: What Actually Breaks This Trade

A technically sophisticated reader deserves an honest accounting of the downside, so here it is.

The primary risk is a sustained backup in long-end rates. If the 30-year Treasury moves another 50 to 75 basis points higher on persistent inflation data or a significant increase in Treasury supply, long-duration muni paper reprices lower. The NAV impact on a leveraged vehicle with a 20-plus year average duration is not trivial. A 75 basis point backup on a portfolio with an effective duration of 18 to 20 years translates to a 13 to 15 point NAV decline before any premium or discount adjustment. Any premium carried by a closed-end vehicle in that scenario does not hold — it compresses, and likely flips to a discount, compounding the mark-to-market pain. Zero-coupon long-dated muni positions within such a portfolio are particularly exposed, as their effective duration approximates their full term to maturity and they carry no coupon cushion to offset price movement.

The second risk is on the short end. If the Fed is forced to reverse course and raise rates — an outcome that is not the base case but is not zero probability given the inflation trajectory — the funding cost of leverage increases. That compresses the carry spread, and distribution coverage deteriorates. A leveraged muni fund's distribution is a function of the spread between what it earns on its portfolio and what it pays to fund its leverage. Narrow that spread materially, and the distribution comes under pressure.

The honest framing of this trade is that it is not a capital appreciation thesis. It is a carry thesis. The job of the long-duration muni allocation is to generate after-tax income at a level that is unavailable elsewhere in investment-grade fixed income, while the rate environment remains cooperative. Range-bound long rates are the condition under which this works. The position sizing and the entry point should reflect that — because when the condition changes, the trade changes with it, and the exit needs to be managed with the same discipline as the entry.

Put the Thesis on Autopilot with Surmount Wealth

Reading the muni curve is one thing. Acting on it systematically, at the right entry points, with the right position sizing, and without letting execution lag erode the carry advantage — that is another problem entirely. This is exactly what Surmount Wealth was built to solve.

Surmount offers a library of prebuilt automated trade strategies across asset classes, and the ability to build fully custom strategies around any thesis your practice is running — including the kind of rate-environment-conditional, carry-driven positioning discussed in this piece. You define the logic. Surmount automates the execution.

What a strategy like this could look like in practice:

Consider a hypothetical strategy we might call the Long Muni Carry Monitor — and to be clear, this is an illustrative idea, not a live product or investment recommendation.

The strategy would hold a core allocation to one or more leveraged, long-duration municipal closed-end funds as its primary income engine. It would monitor a small set of rate environment signals — the 30-year Treasury yield relative to a defined range, the Fed Funds futures implied probability of a hike versus a cut at the next meeting, and the muni-to-Treasury ratio at the long end of the curve. As long as those signals remain within the parameters consistent with the carry thesis — long end anchored, Fed on hold, long muni ratios near fair value — the strategy holds its position and collects the distribution. When one or more of those signals breaches a defined threshold, the strategy reduces exposure or exits, depending on the severity of the signal.

The result is a rules-based implementation of the exact thesis this piece outlines — carry collection in a stable rate environment, with an automated exit condition built around the two risks that actually break the trade. No discretionary second-guessing. No watching the tape every morning and wondering whether today is the day to trim. The rules are set, the logic is transparent, and the execution is handled.

That is what systematic strategy construction looks like when it is applied to a real macro thesis. Surmount makes that kind of strategy buildable — whether you are starting from a prebuilt template or working from a blank page with your own logic.

Why your clients deserve systematic execution:

For the professional advisor or portfolio manager reading this, the carry math we walked through is compelling on paper. But discretionary implementation of a carry trade introduces a category of risk that the math does not capture — behavioral risk. The tendency to hold through the first rate backup because it looks temporary. The tendency to exit after the second one because the pain is real. Systematic strategies remove that variable. The exit condition is defined before the position is entered, which means it gets honored when the moment comes rather than debated.

Surmount's platform is built for exactly this kind of professional-grade strategy design — rules-based, transparent, and executable across client accounts without the operational overhead of managing it manually position by position.

Book a demo today.

If you are running a thesis like this one — or have a dozen others sitting in research documents that have never made it into a scalable, automated implementation — Surmount is worth thirty minutes of your time. Their team works directly with advisors and portfolio managers to translate investment logic into live, automated strategies, whether you are starting from their prebuilt library or building something entirely proprietary.

Book your demo now and see what it looks like when your best ideas start running in a portfolio.