Blog

The "Retirement Gear" Framework: Matching Income Assets to the Economic Cycle

Most retirement planning conversations anchor on a single question: have you saved enough?

It is an important question, but it is increasingly insufficient as a standalone framework.

The number in the account does matter. What matters equally — and receives far less attention — is the economic environment you are stepping into when you begin drawing on that account, and the one you will navigate for the 30 to 40 years that follow.

Consider two clients with identical savings, identical risk profiles, and identical withdrawal rates:

One retires into a low-rate, low-inflation environment with credit spreads at historic tights.

The other retires into a period of elevated rates, dislocated credit markets, and income assets trading at meaningful discounts to intrinsic value.

These are not equivalent starting positions. The second client, if properly positioned, can build an income stream that is both larger and more durable — not because they saved more, but because they packed the right gear for the conditions.

This is the core premise of the Retirement Gear Framework.

Retirement is not a destination you arrive at and then manage identically regardless of circumstances. It is a multi-decade journey, and the assets you deploy should reflect the terrain ahead. A seasoned traveler does not pack the same bag for every trip. Neither should a retirement income portfolio look the same in every macro environment.

The Framework — Four Economic Regimes and the Income Assets That Perform in Each

Regime awareness is not market timing. It is not a call on where rates will be in 18 months. It is a disciplined recognition that different macro environments create structurally different conditions for income assets — and that ignoring those conditions leads to portfolios that are mismatched with the journey they are supposed to fund.

1. Rising Rate and High Inflation Environments

When rates are rising and inflation is elevated, duration is the enemy. Fixed-rate instruments with long maturities experience significant price erosion, and the income they generate is simultaneously being devalued in real terms. In this environment, floating-rate instruments earn their place. Senior secured loans, floating-rate preferred securities, and BDCs with variable-rate loan books tend to hold up better because their income streams adjust upward as benchmark rates rise. Credit quality becomes paramount — this is not the environment for yield-chasing at the bottom of the capital structure.

2. Peak Rate and Plateau Environments

At the top of a rate cycle, before cuts begin, the market tends to misprice duration. Investors remain conditioned by the pain of the rising rate period and avoid fixed-rate instruments even as the risk-reward is quietly shifting in their favor. This is precisely when institutional preferred securities and fixed-rate CEFs begin to offer compelling entry points. NAV discounts widen not because fundamentals have deteriorated but because sentiment remains anchored to the recent past. The portfolio manager who recognizes a plateau environment is looking at a shrinking window of attractive pricing before the normalization cycle begins.

3. Rate Normalization and Cutting Cycles

As central banks begin easing, the tailwinds shift decisively toward fixed-income duration. NAV recovery in leveraged fixed-income funds accelerates. Borrowing costs for funds using floating-rate leverage decline, expanding the spread available for distribution. This is the environment where well-selected CEFs and preferred security funds can deliver both income and meaningful capital appreciation. The asymmetry is attractive — income investors are paid to wait, and the wait comes with a built-in recovery mechanism as rates normalize.

4. Low Rate and Financial Repression Environments

The most challenging environment for income investors is one of sustained financial repression — rates held artificially low for extended periods. Traditional fixed income yields are inadequate, and investors are forced up the risk curve. In this regime, private credit exposure through publicly traded BDCs, dividend-growth equities, and real asset income streams become load-bearing components of the portfolio. Yield sustainability and distribution coverage ratios matter more than headline yield, because the temptation to reach for yield in this environment is where most income portfolios make their most consequential mistakes.

Application — Translating Regime Awareness into Portfolio Construction Decisions

Understanding the framework conceptually is straightforward. Applying it with discipline under real market conditions, and communicating it clearly to clients, is where the work actually lives.

Valuation Signals Worth Monitoring

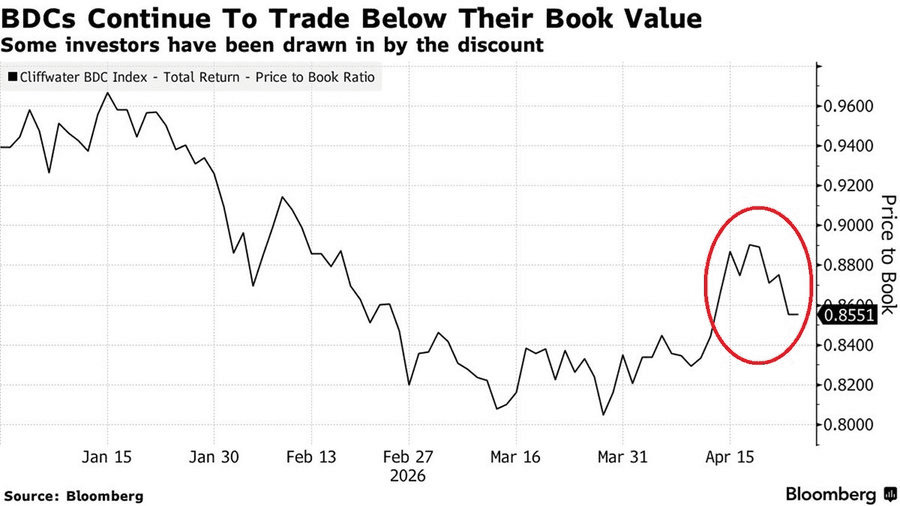

Regime-aware income investing requires a small set of recurring inputs. For credit-oriented income assets, the relevant signals include: discount-to-NAV levels across the CEF universe, BDC price-to-book ratios relative to historical ranges, investment-grade and high-yield credit spread levels, and the proportion of new preferred issuance carrying floating versus fixed coupons. None of these individually dictates positioning, but together they provide a coherent picture of where the market is mispricing income relative to the underlying fundamentals.

When BDCs broadly trade below book value and non-accrual rates remain consistent with historical norms, that divergence warrants attention — not panic, not indifference, but a deliberate assessment of whether the portfolio is positioned to take advantage.

Communicating Regime-Based Positioning to Clients

The greatest practical challenge is not identifying the regime. It is keeping clients positioned through the discomfort that typically accompanies the best entry points. Sector dislocations are, by definition, periods when sentiment is negative. The advisor's role is to separate price behavior from fundamental behavior — to help clients understand that a wide NAV discount in a structurally sound fund is not the same signal as deteriorating credit quality. A useful framing: the portfolio is not reacting to short-term price volatility; it is being equipped for a specific set of journey conditions. That language resonates because it is concrete, it is forward-looking, and it removes the implication that the portfolio is either wrong or in distress.

The Goal Is Consistency, Not Precision

No framework predicts regime transitions with precision, and advisors should not position it as one that does. What it provides is a structured basis for tilting income allocations toward assets that are well-suited to current conditions and attractively valued relative to those conditions. The objective is not to optimize for the next 12 months. It is to build a portfolio capable of funding a 30- to 40-year journey with the consistency and predictability that retirement actually demands.

The right gear, packed thoughtfully, makes the difference between a journey that is sustainable and one that is not.

Put the Framework on Autopilot — Powered by Surmount Wealth

Reading a framework like this is one thing. Implementing it consistently, across dozens of client portfolios, through the noise of daily markets and the friction of manual execution, is another challenge entirely.

That is where Surmount Wealth changes the game.

Surmount allows advisors and portfolio managers to build, automate, and deploy systematic investment strategies — either from a library of prebuilt models or from the ground up as fully custom, rules-based strategies. If you can articulate a thesis, Surmount can help you automate it. No more manual rebalancing. No more inconsistent implementation across client accounts. Just disciplined, systematic execution — every time, at scale.

What Would This Look Like in Practice?

To make this concrete, consider a hypothetical strategy we might call the Regime-Aware Income Rotator — an illustration of exactly the kind of thesis Surmount is built to automate.

The idea: The strategy monitors a rules-based set of macro signals — Federal Reserve rate decisions, credit spread levels, and CEF discount-to-NAV thresholds — and systematically rotates income allocations across four sleeves: floating-rate credit, institutional preferred CEFs, BDC exposure, and short-duration fixed income. When credit spreads are wide and BDC price-to-book ratios fall below a defined threshold, the model increases allocation toward those assets. As the rate cycle shifts and NAV discounts compress, it rotates toward duration. The strategy runs continuously, rebalances automatically, and eliminates the behavioral drag that causes most income investors to be in the wrong asset at the wrong time.

This is a hypothetical strategy concept for illustrative purposes only — not an existing product or investment recommendation.

But here is the point: this is exactly the kind of systematic, thesis-driven strategy that Surmount is built to bring to life. Whether you want to license a prebuilt income strategy and deploy it immediately, or work with the Surmount team to engineer something bespoke to your investment philosophy, the infrastructure is already there.

Why Advisors Are Making the Switch

The advisors gaining the most ground right now are not the ones with the best ideas. They are the ones who can implement their best ideas consistently, at scale, without the operational overhead that typically comes with active portfolio management. Surmount eliminates that gap.

Prebuilt strategies ready to deploy across client accounts from day one

Custom strategy development that encodes your specific investment thesis into automated rules

Seamless multi-account execution so your implementation is as consistent as your thinking

Full transparency and control — you stay in the driver's seat, the automation handles the heavy lifting

The Opportunity Is in the Market Right Now

As this blog lays out, the current environment is presenting a genuine window — dislocated income assets, compressed valuations, and a rate cycle that is shifting in favor of well-positioned portfolios. These windows do not stay open indefinitely. The advisors who act with speed and precision will capture what the hesitant ones will read about in retrospect.

Don't let a sound thesis sit unexecuted.

📅 Book a Demo with Surmount Wealth Today

See exactly how your income strategy — or one of Surmount's prebuilt models — can be automated and deployed across your book of business. The conversation takes 30 minutes. The impact on your practice could be permanent.