Blog

The "Six-Figure Limit": Assessing the Beta of Social Security Reform

In the traditional hierarchy of financial planning, Social Security has long been modeled as the "risk-free" foundation of the retirement capital stack. In fact, for decades, advisors have treated it as a defined-benefit proxy: a predictable, government-guaranteed, inflation-indexed annuity with a beta of zero. However, as we approach the 2033 insolvency window, the fundamental nature of this asset is shifting.

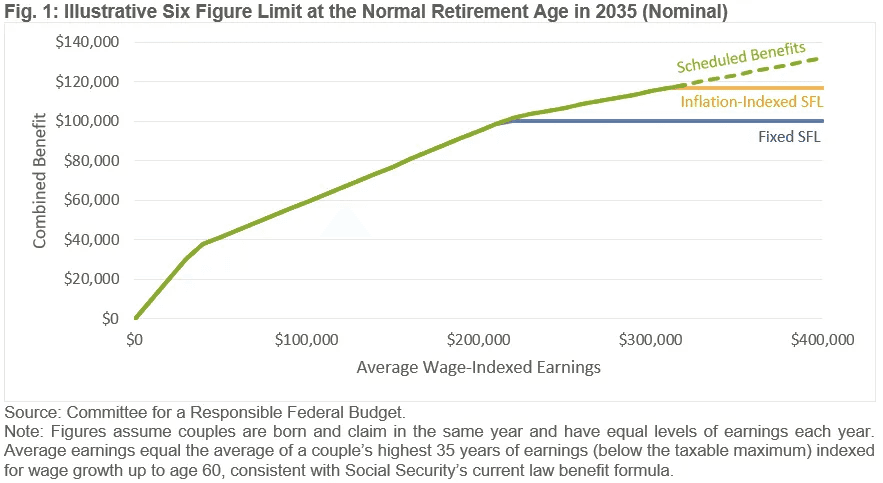

The recent proposal by the Committee for a Responsible Federal Budget (CRFB) to implement a "Six-Figure Limit"—capping annual benefits at $100,000 for couples—represents a pivot point for the industry. For your High-Net-Worth (HNW) clients, this is an important legislative tail-risk to keep track of.

If enacted, this "Six-Figure Limit" effectively transforms Social Security from a defined benefit into a politically contingent asset for the top 0.05% of earners. By decoupling future benefits from the historical Social Security "wage base" (set at $184,500 in 2026), the government is essentially proposing a retroactive cap on the ROI of a lifetime of maximum contributions.

For the modern portfolio manager, the "Six-Figure Limit" means that Social Security can no longer be viewed through a static lens. We must begin to assess the "Beta of Reform." If the floor of the retirement plan (which is basically the one source of non-correlated, inflation-adjusted cash flow) is subject to a hard ceiling or an across-the-board 24% reduction, our probability-of-success models must evolve.

This is no longer just about Social Security's solvency; it is about the systematic re-characterization of the asset itself and how we must adjust the duration and risk profile of the private portfolios tasked with filling the resulting void.

Modeling the "Wealth Tax" via Benefit Attrition

The most important thing to consider, with regards to the six-figure limit, is the structural change to the Internal Rate of Return (IRR) of a client’s lifetime Social Security contributions. For the HNW segment, this proposal effectively functions as a retrospective wealth tax by capping the payout of a system they have already over-funded.

The Indexing Trap: Bracket Creep by Design

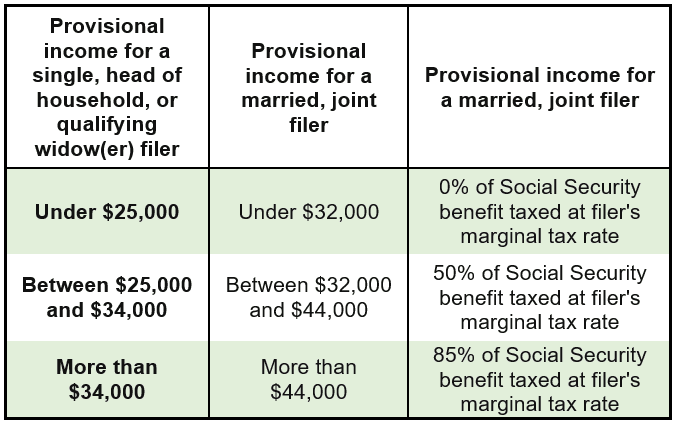

The most significant systematic risk in this proposal is the mechanism of indexing. To understand the danger, we need only look at the taxation of Social Security benefits. Since 1984, the thresholds for taxing benefits (e.g., $32,000 for joint filers) have remained nominal, never once adjusted for inflation.

If a $100,000 benefit cap is implemented without robust indexing to the Consumer Price Index (CPI), it creates a "vanishing floor."

The Math: At a modest 3% annual inflation rate, a $100,000 cap today has the purchasing power of only $55,367 in 20 years.

The Result: Advisors modeling 30-year retirements must account for the high probability that this "cap" becomes a tightening noose, capturing a larger percentage of the "middle-upper" class over time, much like the Alternative Minimum Tax (AMT) once did.

The "Waiters" Penalty: Evaporating Deferral Credits

For decades, the "gold standard" advice for healthy HNW clients has been to delay benefits until age 70 to capture the 8% annual delayed retirement credits. The Six-Figure Limit fundamentally breaks this calculus.

Consider a high-earning couple with a Primary Insurance Amount (PIA) of $4,200 each. By waiting until age 70, their combined benefit could easily exceed $100,000. If the cap is a hard ceiling:

The IRR collapses: The "yield" on the 8-year deferral period (from 62 to 70) drops to zero once the cap is hit.

Increased Drawdown Risk: Clients would be depleting private, tax-advantaged portfolios to "wait" for a stepped-up benefit that the government then confiscates via the cap.

Advisors may need to pivot to an "Early Claim, Early Invest" strategy, where the client takes the benefit at the Normal Retirement Age (NRA) to ensure they capture the cash flow before it hits the legislative ceiling.

Sensitivity Analysis: The 24% "Haircut" vs. The Cap

We must model this as a binary risk outcome. Current projections suggest an across-the-board 24% cut by 2033 if no action is taken.

Feature | The 24% Across-the-Board Cut | The $100,000 Cap |

Primary Target | All retirees (Progressive impact) | Top 0.05% - 5% (Targeted impact) |

Planning Implication | Systematic reduction in "Safe Withdrawal Rate" | Capping of the "Fixed Income" floor |

Portfolio Hedge | Defensive/Quality Income focus | Aggressive Growth/Accumulation focus |

The proposed limit creates a unique convexity risk. While it protects the solvency of the system for the masses, it creates a "tail risk" for the very clients who represent the bulk of an advisor's Assets Under Management (AUM). Modeling a flat 10% to 15% reduction in anticipated Social Security cash flows is no longer a "pessimistic" view—it is a necessary stress test for fiduciary excellence.

Strategic Reallocation: Hedging the Legislative Haircut

If the "risk-free" floor of a client’s retirement plan is effectively capped or cut, the liability (maintaining their lifestyle) remains unchanged. This creates a "funding gap" that must be closed through more aggressive or more efficient private capital management. For the HNW segment, we must view the proposed $100,000 cap as a duration extension event.

Extending the Growth Runway

To offset a legislative haircut, the traditional "glide path" that shifts clients toward fixed income as they approach their 60s may no longer be optimal. Advisors should consider two things:

Duration Extension in Equities: Maintaining a higher weighting in "Accumulation Phase" assets (Large-Cap Growth) further into the early years of retirement. If we assume a 10% reduction in expected Social Security cash flows, the portfolio must generate an additional $5,000 to $10,000 in annual distributions.

Active Alpha vs. Passive Beta: In a world where the government floor is lowering, the 8.73% CAGR of the S&P 500 may not be sufficient. This is where institutional-grade active strategies, such as Fidelity Contrafund (FCNTX) or JPMorgan Large Cap Growth (SEEGX), earn their fees by attempting to provide the necessary buffer without significantly increasing the standard deviation relative to the benchmark.

Yield Enhancement: Swapping Sovereigns for Corporates

With Social Security benefits potentially capped, the fixed-income portion of the portfolio must work harder.

Rather than sticking strictly to intermediate government bonds, PMs might look toward intermediate corporate credit, such as the Schwab 5-10 Year Corporate Bond ETF (SCHI).

Similarly, by capturing the credit spread (currently yielding roughly 100-125 basis points over Treasuries) advisors can partially synthesize the "lost" Social Security COLA adjustments through higher organic portfolio yield.

The Sequence of Returns Contingency

Extended equity exposure naturally invites higher volatility. To hedge this, the "Strategic Reallocation" must include a robust liquidity sleeve.

The 24-Month Cash Bridge: To remain in growth equities longer without falling prey to a poorly-timed market drawdown, clients should maintain at least two years of living expenses in cash equivalents or ultra-short duration vehicles.

Strategic Withdrawals: This allows the growth portfolio to remain untouched during market corrections, effectively "self-insuring" against the legislative volatility of the Social Security system.

Ultimately, the goal is not to chase returns for the sake of greed, but to treat the CRFB’s proposal as a signal to overshoot retirement targets by at least 10%. In the HNW space, the best hedge against a change in the rules of the game is to be less dependent on the referee.

Automate the Alpha: Bridge the Retirement Gap with Surmount Wealth

The era of "set it and forget it" retirement planning is over. When legislative risk introduces a variable beta to your Social Security floor, your portfolio must work harder, smarter, and with greater precision. If your current thesis requires a 10% accumulation "overshoot" or a tactical rotation into institutional growth and corporate credit, you shouldn't be executing those moves manually in a volatile market.

Surmount Wealth empowers professional advisors and sophisticated investors to turn macroeconomic insights into automated reality. Whether you are hedging against the "Six-Figure Limit" or capitalizing on the "SaaSpocalypse," our platform provides the infrastructure to build, backtest, and deploy high-conviction strategies with institutional rigor.

Why Portfolio Managers are Moving to Surmount:

Custom Strategy Engine: Don't just read the analysis—automate it. Build a custom "Social Security Hedge" strategy that dynamically scales equity duration based on your client’s unique risk-adjusted needs.

Prebuilt Alpha Strategies: Access our library of vetted, automated strategies designed to outperform standard benchmarks during shifting interest rate cycles.

Total Transparency & Liquidity: Unlike the opaque world of private equity, Surmount keeps you in control of liquid assets with real-time execution and zero "black box" mystery.

Precision Accumulation: Mitigate sequence of returns risk by automating your cash-buffer rotations, ensuring your clients stay in growth mode without the fear of a mistimed market drawdown.

The math of retirement is changing. Your execution tools should too.

Don't let legislative uncertainty erode your clients' hard-earned capital. Join the next generation of advisors who are automating their edge.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.