Blog

Why Energy Sovereignty is the Only Real Defensibility in AI

In the initial phase of the AI super-cycle, the investment thesis was simple: scarcity equals alpha. For much of 2023 and 2024, the primary bottleneck was the silicon itself. Portfolio managers focused heavily on "GPU counts" and "allocation queues" as the lead indicators of a firm’s competitive standing. If you had the chips, you had the market.

However, as we move through 2026, we are witnessing a classic industrial transition. The frantic "land grab" for H100s and Blackwell B200s has given way to a saturated hardware market. Silicon, once the most precious asset in the tech stack, is rapidly transitioning into a high-performance commodity.

The Erosion of the Hardware Moat

The professional investor must now grapple with the "Paradox of Abundance." While the raw computational power available to the market has grown exponentially, the return on invested capital (ROIC) for firms whose only value proposition is "having chips" is under immense pressure. Several factors are driving this commoditization:

The Secondary Market Explosion: As the first generation of AI-dedicated clusters undergoes refresh cycles, the market is being flooded with "legacy" compute. This creates a pricing ceiling for neoclouds that lack specialized software or architectural advantages.

Architectural Parity: The gap between proprietary silicon and merchant silicon is narrowing. With the rise of custom ASICs from hyperscalers and the stabilization of model architectures, "compute" is increasingly viewed as a fungible utility—much like RAM or storage in the previous decade.

Yield Compression: In a market where everyone has access to the same fundamental hardware, the only way to compete on a commoditized product is on price. We are seeing a "race to the bottom" in cost-per-token, which benefits the end-user (the AI application developer) but devastates the margins of the pure-play infrastructure provider.

Owning the "picks and shovels" is no longer a guaranteed win if everyone else has the same tools. When hardware is abundant, the bottleneck moves elsewhere.

We are seeing a shift in the "Total Cost of Ownership" (TCO) model for AI. Historically, the silicon accounted for the lion’s share of the CAPEX. Today, the operational expenses (OPEX)—specifically the cost of keeping those chips cool and powered—have become the dominant variable in the profitability equation.

As silicon becomes a commodity, the market is beginning to realize that a thousand GPUs are worthless without the sovereign power to run them. The true defensibility in the AI trade has migrated from the chip designers to the entities that control the grid.

The Infrastructure Bottleneck: Energy Sovereignty as the New "Moat"

As the "AI trade" matures, the primary constraint is shifting from silicon availability to grid connectivity. For the professional investor, this transition necessitates a move away from evaluating chip architecture toward auditing Megawatts (MW) under management. It is becoming clear that, increasingly, the "alpha" no longer resides in who can buy the chips, but in who can power them.

Gridlock and the 10-Year Lead Time

The fundamental "bottleneck" in AI infrastructure is a temporal one. While a high-performance compute cluster can be procured and staged in months, securing 100MW+ of grid interconnection now carries a lead time of 5 to 10 years in primary markets like Northern Virginia or West London.

For a portfolio manager, this creates a significant "Execution Moat." A company with "shovel-ready" power capacity is essentially holding an irreplaceable call option on the AI cycle. Conversely, an "AI growth" company without secured power is effectively a software firm pretending to be an infrastructure firm—a distinction that the market is beginning to punish with severe valuation de-ratings.

Vertical Integration: The "Energy Alpha"

We are witnessing a structural shift toward Energy Sovereignty, where compute providers are becoming de facto utility operators to protect their margins. This manifests in three key ways:

Small Modular Reactors (SMRs) and On-site Nuclear: Major hyperscalers and top-tier neoclouds have moved from simply buying "green credits" to signing direct offtake agreements for nuclear power. Microsoft’s reactivation of Three Mile Island and Meta’s recent 1.2 GW nuclear campus deal with Oklo are not "ESG" plays—they are hard-nosed risk-mitigation strategies to ensure 24/7 uptime without grid volatility.

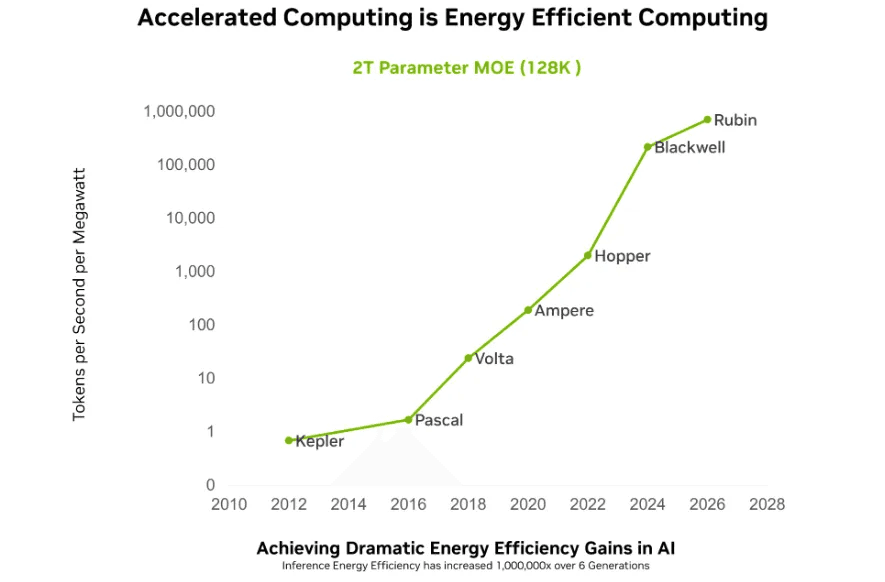

The Power Density Gap: Standard data center racks traditionally pulled 5–15 kW. Current AI-optimized racks now require 40–100 kW per rack. This 10x density leap makes legacy data centers obsolete, as they lack the electrical switchgear and liquid-cooling infrastructure to handle such thermal loads.

Contractual "Backstops": Just as we look at "Take-or-Pay" contracts in the energy sector, we must now scrutinize Power Purchase Agreements (PPAs). A firm with long-term, fixed-rate power access is shielded from the "energy inflation" that occurs as data centers consume a projected 10% of total U.S. electricity by 2028.

The Scarcity Premium: Valuing MW-under-Management

For advisors, the due diligence process must now include a "Power-to-Equity" sanity check. If a company is trading at a $50B valuation but only has 200MW of secured, operational power, the implied valuation per megawatt becomes indefensible compared to legacy infrastructure benchmarks.

Remember that the real "Energy Alpha" belongs to the firms that own the behind-the-meter assets. By bypassing the public grid, these players avoid the regulatory and physical congestion of the aging macro-grid, allowing them to scale at the speed of the GPU cycle, not the speed of the utility commission.

Beyond the Terrestrial Grid: The Frontier of "Off-Grid" Compute

As terrestrial power grids in Tier 1 data center markets (like Northern Virginia or Dublin) reach their breaking points, the investment frontier is shifting toward decoupled infrastructure. For the sophisticated allocator, this represents a transition from "Real Estate" risk to "Logistical and Engineering" risk. To maintain the margins necessary to justify current valuations, the industry is increasingly looking at ways to bypass the traditional utility provider entirely.

Stranded Energy and the "Data-to-Fuel" Migration

Historically, industry followed the workforce; in the AI era, industry follows the electron. We are witnessing a migration of compute to "stranded" energy sources—locations where power is abundant but lacks the transmission infrastructure to reach residential or industrial hubs.

The first dimension here is the methane mitigation play. Specialized firms are now deploying modular data centers directly at oil and gas wellheads, utilizing flared natural gas to power onsite compute. This transforms a carbon liability into a high-margin digital export.

Then is hydro-sovereignty: We are seeing a resurgence in "Nordic-style" site selection, where data centers are co-located with isolated hydroelectric dams. For portfolio managers, the "Alpha" here lies in the Energy Arbitrage: buying power at sub-wholesale rates that no other industry can physically access.

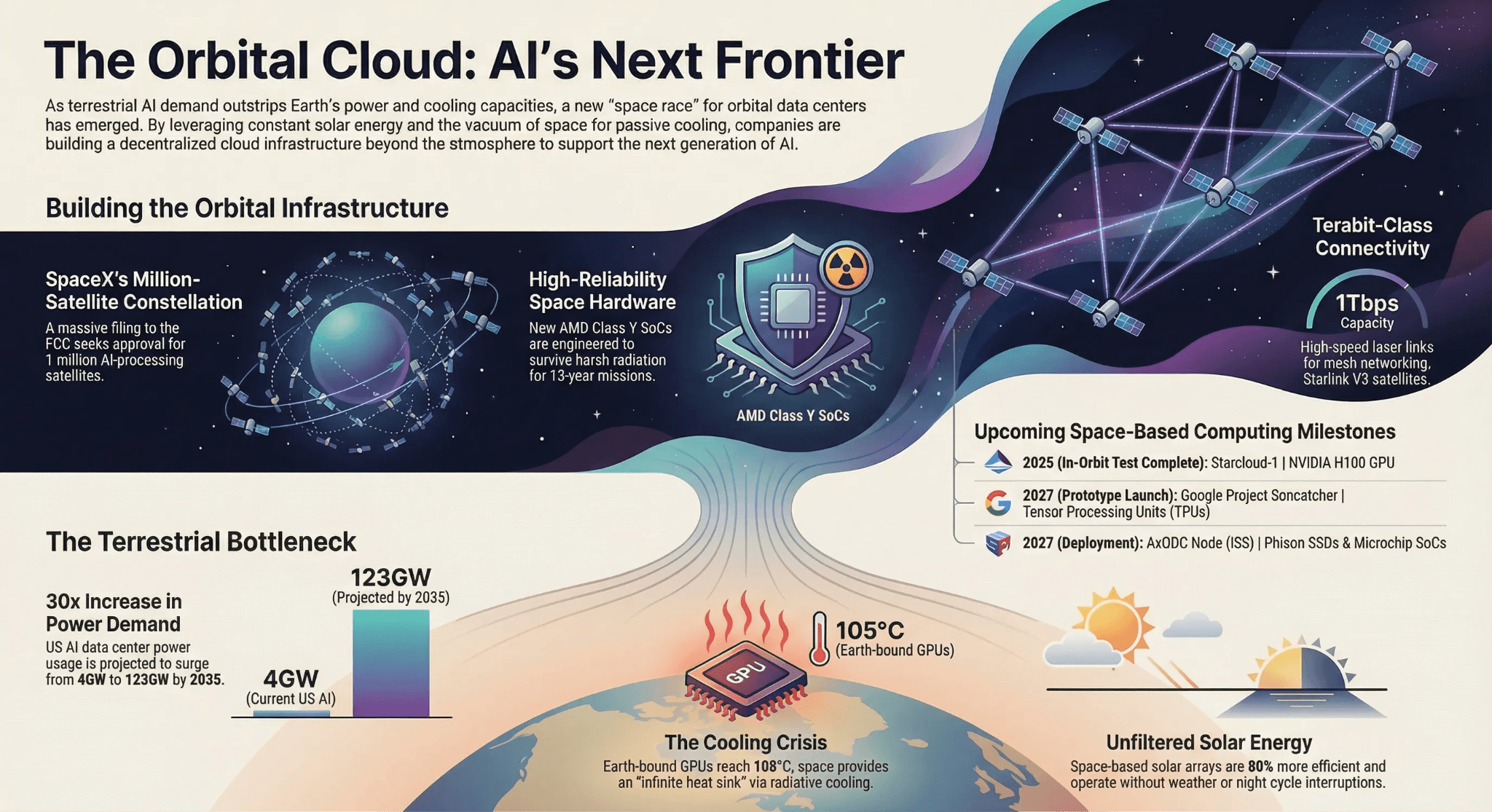

The Orbital Infrastructure: "Space-to-Grid"

The most extreme expression of energy sovereignty is the movement of compute off-planet. While it sounds like science fiction, the capital being deployed into orbital data centers and space-based solar power is grounded in cold, hard physics.

In the vacuum of space, solar panels can operate with nearly 100% uptime, free from atmospheric interference or the diurnal cycle. Furthermore, the massive cooling requirements that plague terrestrial data centers—often consuming 30-40% of total power—are reimagined in the cold sink of orbit.

While not suitable for high-frequency trading or consumer-facing apps, orbital compute is becoming the "deep cold storage" and "heavy lifting" hub for model training. Investing in companies that facilitate space-based data centers (like the xAI/SpaceX synergy) is essentially a bet on Vertical Integration that scales beyond the physical constraints of Earth’s atmosphere.

The New Due Diligence: "Who Owns the Switch?"

For the investment advisor, the takeaway is clear: the technical specifications of the LLM are secondary to the physical resilience of the power source. In a world of increasing grid instability and regulatory "energy quotas," true defensibility is found in the "Off-Grid" players.

When conducting due diligence on "Infrastructure Plays," the primary questions must shift:

Grid Independence: What percentage of the company’s compute is powered by proprietary microgrids vs. public utilities?

Regulatory Immunity: Does the energy source sit outside the jurisdiction of "curtailment" laws during peak summer/winter demand?

The Marginal Cost of Cooling: As density increases, is the company solving cooling through traditional water/air (a growing ESG liability) or through radical site selection (Space, Sub-sea, or Arctic)?

Ultimately, the "Space-to-Grid" Alpha isn't just about high-tech novelty; it is about securing the supply chain of the electron. In the AI arms race, the winner won't be the one with the best code—it will be the one who never has to ask permission to turn the lights on.

Turning Insight into Action: Automate Your High-Conviction Theses

Identifying the structural shift from "Silicon" to "Sovereign Power" is only half the battle. For the professional advisor, the real challenge lies in execution—maintaining a disciplined exposure to these thematic tailwinds without being consumed by the manual overhead of rebalancing, risk management, and the high-frequency noise of the AI hype cycle.

This is where Surmount Wealth changes the game.

Our platform is designed specifically for investment professionals who demand institutional-grade control paired with seamless automation. Whether you are looking to capture the "Energy Alpha" we discussed today or deploy a proprietary systematic strategy, Surmount provides the tools to turn your research into a live, rule-based portfolio in a fraction of the time.

Why Leading Advisors are Switching to Surmount:

Automate Any Thesis: Use our no-code builder to turn specific data points—like energy capacity, Capex-to-Revenue ratios, or hardware refresh cycles—into automated entry and exit signals.

Prebuilt Institutional Strategies: Access a library of data-driven models designed to navigate the volatility of the AI and infrastructure sectors, ready for immediate deployment.

Full Customization & Control: Unlike "black box" robo-advisors, Surmount gives you the keys. You define the logic; our AI-driven engine handles the relentless execution 24/7.

Broker-Agnostic Integration: Seamlessly connect your automated strategies to your existing accounts (including Interactive Brokers and Alpaca) without the need for complex ACAT transfers.

Don’t Just Watch the Trend—Capture It.

The window to capitalize on the "Space-to-Grid" transition is open, but in a market this fast, manual execution is a liability. It’s time to move beyond spreadsheets and legacy workflows.

See how Surmount Wealth can scale your investment management and deliver a more software-driven client experience.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.