Blog

Fiscal Policy and Demographic Arbitrage: Investment Implications

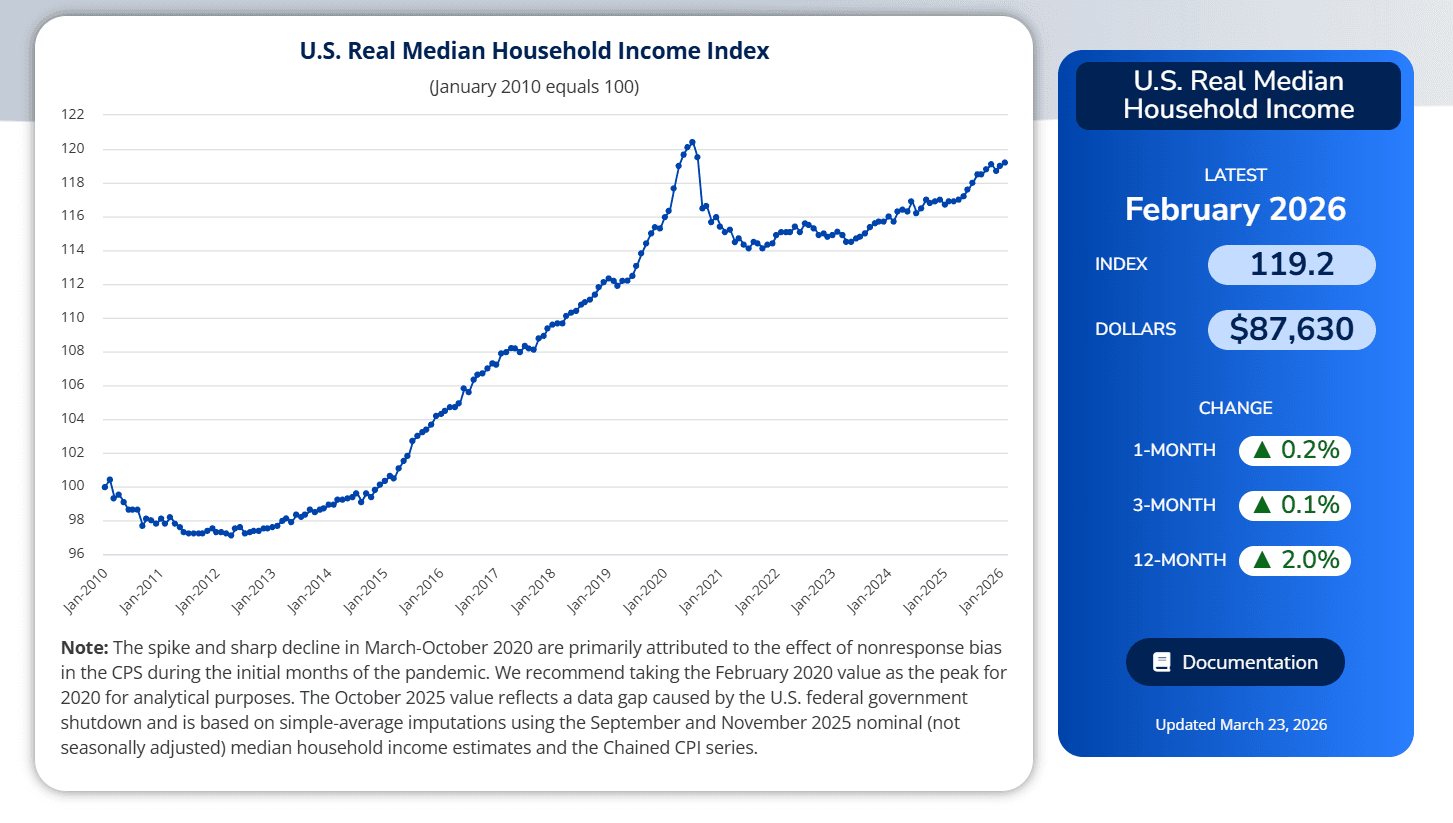

Recently, Motio Research released their initial estimate of U.S. median household income for February 2026, pegging the figure at $87,630, which implies a $360 month-over-month increase. This, understandably, seems to suggest that the U.S. consumer is entering the second quarter of the year on a footing of renewed strength.

While this may appear to signal that the economy is finally breaking through the potential of a 2026 recession that economists had pointed to, a more rigorous technical interrogation of the data suggests we may be witnessing a statistical mirage rather than a genuine expansion of middle-class purchasing power. Looking closely, a rising median is only as valuable as the underlying drivers of that growth; in the current environment, those drivers appear to be demographic rather than purely economic.

The Compositional Shift: Why the Denominator Matters

The fundamental challenge with median-based metrics is their sensitivity to population composition. When we observe a 0.4% increase in the median, the natural assumption is that the "typical" household is earning more. However, the Trump administration’s recent fiscal initiatives—specifically the $3000 cash and free travel incentives offered to illegal immigrants—have introduced a significant exogenous variable. By facilitating the exit of a large volume of the nation’s lowest-income earners, the administration has effectively "truncated" the bottom of the income distribution.

Understanding the "Exit Boost"

In a distribution of values, removing the lowest-weighted entries automatically shifts the midpoint (the median) upward, even if no single remaining household receives a raise. This Demographic Arbitrage allows for a cosmetic improvement in national income statistics that masks a potential slowing in organic growth. Indeed, Motio’s own survey-based estimates indicate that the actual pace of income growth may have decelerated since the end of 2025.

Distinguishing Nominal Gains from Structural Health

As the initial value of the U.S. Real Median Household Income Index hits 119.2 for February 2026, advisors must distinguish between:

Organic Momentum: Real wage growth fueled by productivity and labor demand.

Arithmetic Momentum: A "rising floor" effect caused by the departure of low-income demographics.

For the investment professional, mistaking the latter for the former can lead to significant misallocations in consumer-facing equities and credit risk models. As we move further into 2026, the divergence between survey-based sentiment and aggregate wage data—which currently shows a 0.9% gap—will be the primary "noise" that must be filtered to find the true signal of economic health.

Decomposition of the Real Income Index

According to the Motio Survey, February’s US real median household income index climbed to 119.2. This index value serves as a vital technical benchmark, representing a 19.2% increase in real, inflation-adjusted median income over the last 16 years. However, a granular decomposition reveals three critical tensions that portfolio managers must reconcile.

1. The Momentum Stall: Deceleration in Real Terms

While the nominal monthly increase for February 2026 was 0.4%, the pace of growth in the Real Index has notably slowed since the final quarter of 2025. This suggests that while wages are still climbing in dollar terms, the "Real" gains are hitting a plateau.

For specialists, this indicates that the marginal utility of current fiscal and labor policies may be diminishing. If the index fails to break toward 120 in the coming months, it could signal that the domestic consumer’s purchasing power peak is behind us.

2. Methodological Divergence: Survey Sentiment vs. Hard Wage Data

A significant point of friction exists between the Motio Index (119.2) and the BEA-derived wage data by other analysts. These can be summarised as follows:

The "Sentiment Gap": Motio’s data is survey-based (Current Population Survey), which often captures shifts in household composition and sentiment in near real-time.

The "Reality Check": Political Calculations' January estimate sits 0.9% ($764) below Motio’s initial estimate.

For advisors, this delta is significant. It suggests that while households report higher income levels (potentially due to the exit of lower-earning neighbors), the aggregate "hard" wage data, which relies on actual payrolls and salary disbursements, is actually taking longer to validate these gains.

3. The Revision Trap and "Data Fog"

There also seems to be massive upward revisions by the BEA from July through December 2025, with some months seeing adjustments as high as +0.73%. These are structural shifts that were initially missed.

This reinforces the idea that relying on the 119.2 figure as a static data point is risky. If the pattern of significant upward revisions continues, the "real" economic floor might actually be stronger than the current index suggests. Conversely, if the revisions begin to skew downward as the labor market cools, the 119.2 index could be an overestimation of the remaining consumer base's strength.

4. Adjusting the "Real" Benchmark

When modeling future cash flows for consumer-facing equities, the 119.2 level should be viewed as a "resistance point." Given that the median is being mechanically buoyed by demographic exits at the bottom of the curve, the Index may actually be overstating the health of the middle-income bracket.

Portfolio managers should discount this index growth by the estimated "compositional boost" to find the organic growth rate of the core American consumer.

Sector Implications: Labor Tightening and the Service Beta

For the portfolio manager, the "Demographic Arbitrage" identified in the data above suggests a bifurcated impact on corporate margins. We can break these implications down into three primary vectors:

1. The "Cost-Push" Squeeze in Low-Margin Services

The departure of a large segment of the lowest-income earners—traditionally the backbone of the flexible, entry-level labor force—is not just a demographic shift; it is a structural supply shock.

Sectors with high operating leverage and high reliance on low-wage labor (e.g., hospitality, quick-service restaurants (QSR), and basic facilities management) will likely face acute margin compression.

Ultimately, as the labor floor disappears, the "reservation wage" for remaining workers resets higher. Advisors should scrutinize the Labor-to-Revenue ratios of firms in these spaces. Companies unable to pass these costs through to a shrinking "bottom-tier" consumer base are at significant risk of earnings misses.

2. The TAM Contraction in Discount Retail and Staples

According to the income effect, rising median household income expands the Total Addressable Market (TAM). However, if this rise is purely compositional, the absolute number of consumers may be falling.

For discount retailers and consumer staple giants, volume is the primary driver of valuation. If the "exit" of the demographic is substantial enough to move the national median by 0.4% in a single month, it implies a volume loss that may not be offset by the increased "wealth" of the remaining middle class.

As such, we expect a premium to be placed on companies with high pricing power and a move away from those reliant on "high-velocity, low-ticket" transactions.

3. Multifamily Real Estate and Class C REITs

The housing market provides perhaps the most direct evidence of this arbitrage, and may even suggest an occupancy delta. The Motio Research data implies a sudden reduction in the population segment that typically occupies Class C multifamily units or "niche" workforce housing.

This poses a valuation risk. Portfolio managers should be wary of REITs with heavy exposure to the "bottom-rung" rental market. While the median income of the remaining population looks stronger—potentially supporting higher rents in Class A or B assets—the Class C assets may face a "vacancy cliff" that traditional absorption models failed to predict for 2026.

4. Capex as a Proxy for Survival

Finally, this demographic exit accelerates the Automation Mandate.

We are looking for "Service Beta" firms that are aggressively shifting toward capital expenditure in robotics and AI-driven service layers. In an environment where the human labor floor is being policy-incentivized to exit, Capex is no longer an optional growth strategy; it is a defensive necessity to preserve EBITDA margins against rising structural wages.

On a more technical note, managers should keep a close eye on Unit Labor Costs (ULC) relative to these income gains. If ULC is outstripping the 0.4%–0.6% monthly income growth, it confirms that the "Statistical Mirage" of higher wealth is masking a deeper erosion of corporate profitability.

From Macro Thesis to Systematic Execution

Identifying a structural shift like demographic arbitrage is only half the battle. For the professional investment advisor, the true challenge lies in the "Execution Gap"—translating a nuanced macroeconomic insight into a precise, risk-adjusted portfolio position before the market prices in the delta.

This is where Surmount Wealth transforms your research into reality.

The data is clear: median income is currently a "noisy" signal. Whether you want to hedge against labor-supply shocks in the service sector or capitalize on the divergence between survey-based sentiment and BEA aggregate revisions, you shouldn't be limited by manual execution or rigid, off-the-shelf models.

With Surmount Wealth, you can:

Automate Any Thesis: Deploy custom automated trading strategies that react to the exact data points we’ve discussed—from inflation-adjusted income indices to sector-specific labor betas.

Access Prebuilt Alpha: Utilize our library of sophisticated, institutional-grade strategies designed to navigate the "Data Fog" of 2026.

Eliminate Latency: Our infrastructure ensures your thesis is executed with systematic precision, removing the emotional bias and timing risks of manual trading.

Don't let your best insights sit on the sidelines while the data shifts. In a market defined by rapid policy changes and demographic volatility, precision is your greatest hedge.

See the platform in action. Book a personalized demo today and discover how Surmount Wealth can automate your competitive advantage.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.