Blog

Full Replication vs. Sampling: Why ETF Construction Can Make or Break Portfolios

To most of us, index ETFs are the ultimate "set it and forget it" vehicle—a transparent, low-cost shortcut to market beta. An entire class of investors prefer index ETFs over typical ETFs, given some of the key structural advantages they offer in terms of liquidity and cost-efficiency. Afterall, they boast superior tax efficiency given the in-kind creation and redemption mechanism, which largely shields the end-investor from the capital gains realizations that plague traditional mutual funds. Furthermore, they democratize access to institutional-grade portfolios, allowing a retail advisor to deploy a sophisticated global allocation with a few clicks of a mouse.

While portfolio managers and investment advisors pay a great deal of attention to expense ratios, few actually look under the hood at the actual plumbing of the fund to assess the replication methodology.

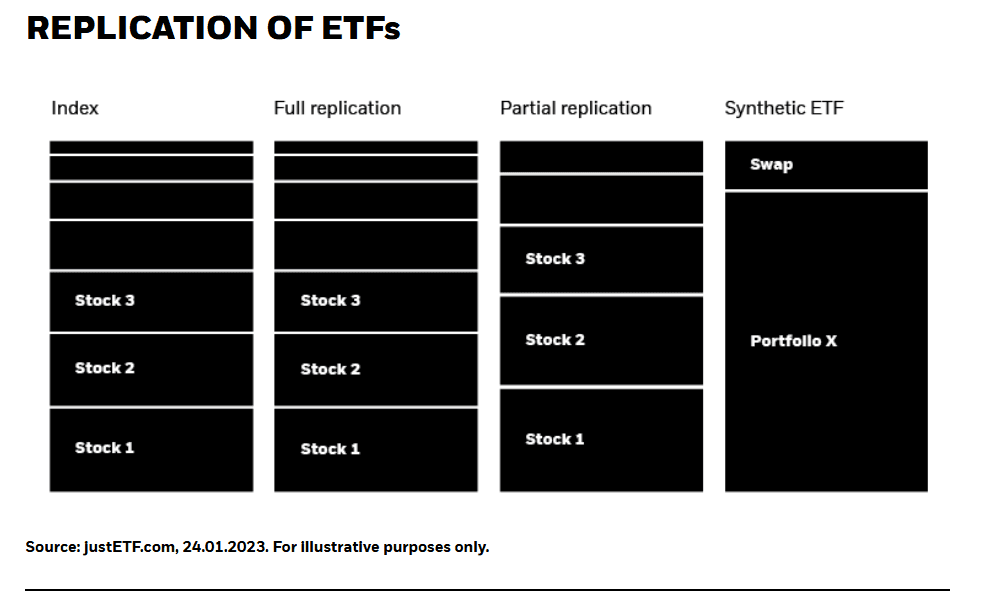

Replication, in the context of index ETFs, refers to the specific operational process the fund manager employs to mirror the performance of a target benchmark. It is the bridge between a theoretical mathematical index and a live, tradable portfolio of securities. While an index is a frictionless list of numbers, a fund is a physical entity subject to the laws of market liquidity, transaction costs, and regulatory constraints.

Generally, this bridge is built using one of two distinct architectural philosophies: Full Replication or Representative Sampling.

For sophisticated practitioners, understanding the fundamental differences between both philosophies can be crucial.

The Architecture of Alpha: Replication vs Sampling

For a portfolio manager, the choice between full replication and sampling is rarely about preference; it is a pragmatic response to the liquidity, depth, and friction of the underlying asset class. Understanding these nuances is critical for accurately forecasting tracking error and managing client expectations.

Let’s individually take a look at each of the two.

Full Replication: The Pursuit of Zero Tracking Error

Full replication is the "physical" approach to indexing. The fund manager purchases every single security in the benchmark at its exact index weight.

So for example, if an index contains 500 stocks, the ETF holds 500 stocks. The primary goal is to minimize Active Share to zero, ensuring the only divergence from the benchmark is the expense ratio and minor cash drag.

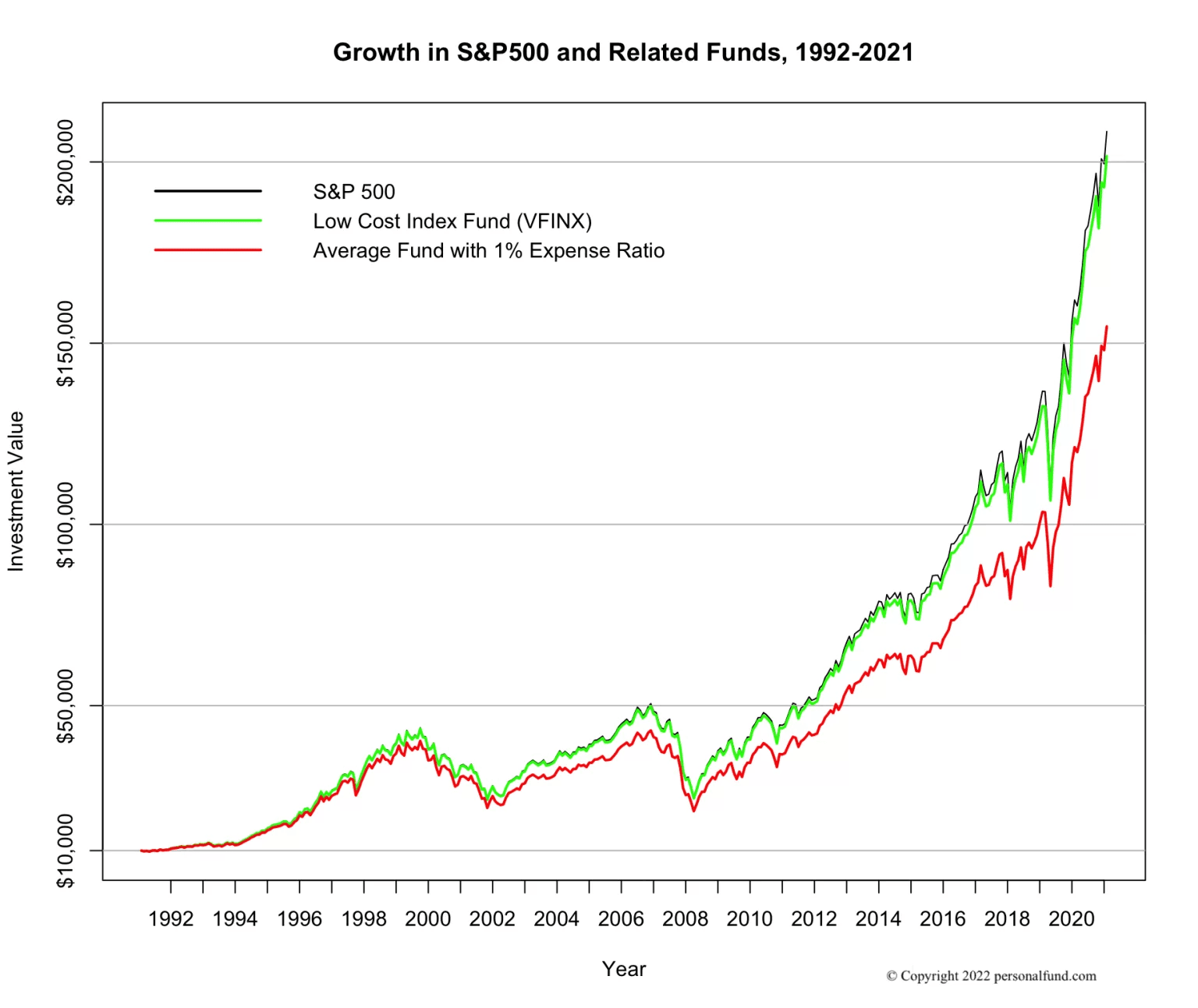

While this provides the highest fidelity, it is sensitive to transaction costs. In high-turnover indices, the cost of buying and selling every minor constituent can erode the very returns the fund seeks to capture.

The graph below highlights the difference in returns between a 0.1% fee vs a 1% fee.

This is precisely why replicating the S&P 500 is a commoditized exercise in this space because the underlying constituents trade millions of shares daily with razor-thin spreads.

For large-scale allocations to core domestic equities, the priority is "tax-loss harvesting" efficiency and absolute transparency. When managing pension or endowment money, explaining a 40-basis-point drift caused by a "sample" mismatch is a difficult conversation that is easily avoided by choosing full replication.

Representative Sampling: Engineering the Proxy

Sampling (or optimization) is a sophisticated quantitative exercise. Instead of buying everything, the manager uses multi-factor models to select a subset of securities that match the primary risk characteristics of the index.

Here, the manager ensures the sample matches the index's duration, credit quality, sector weighting, and fundamental factors (like P/E or yield), even if the individual holdings differ.

Sampling is often a necessity rather than a choice. In the fixed-income world, for example, many bonds in an index may not have traded for weeks. Attempting to buy them would result in massive "pay-up" costs. Sampling allows the manager to bypass illiquid "junk" while maintaining the desired exposure.

The Bloomberg US Aggregate Bond Index contains over 13,000 securities. Buying every single one is not only inefficient—it’s impossible. A manager needs a sampled ETF that provides the "flavor" of the Agg without the deadweight of illiquid, non-tradable issues that would widen the ETF’s bid-ask spread.

The High-Stakes Choice: How Construction Methodology Dictates Alpha and Risk

The choice between full replication and sampling can often act as the primary driver of risk-adjusted returns and fiduciary accountability. While the expense ratio is the most visible cost, the construction methodology creates "hidden" performance drivers that can either shield a portfolio during volatility or erode its value through structural inefficiencies.

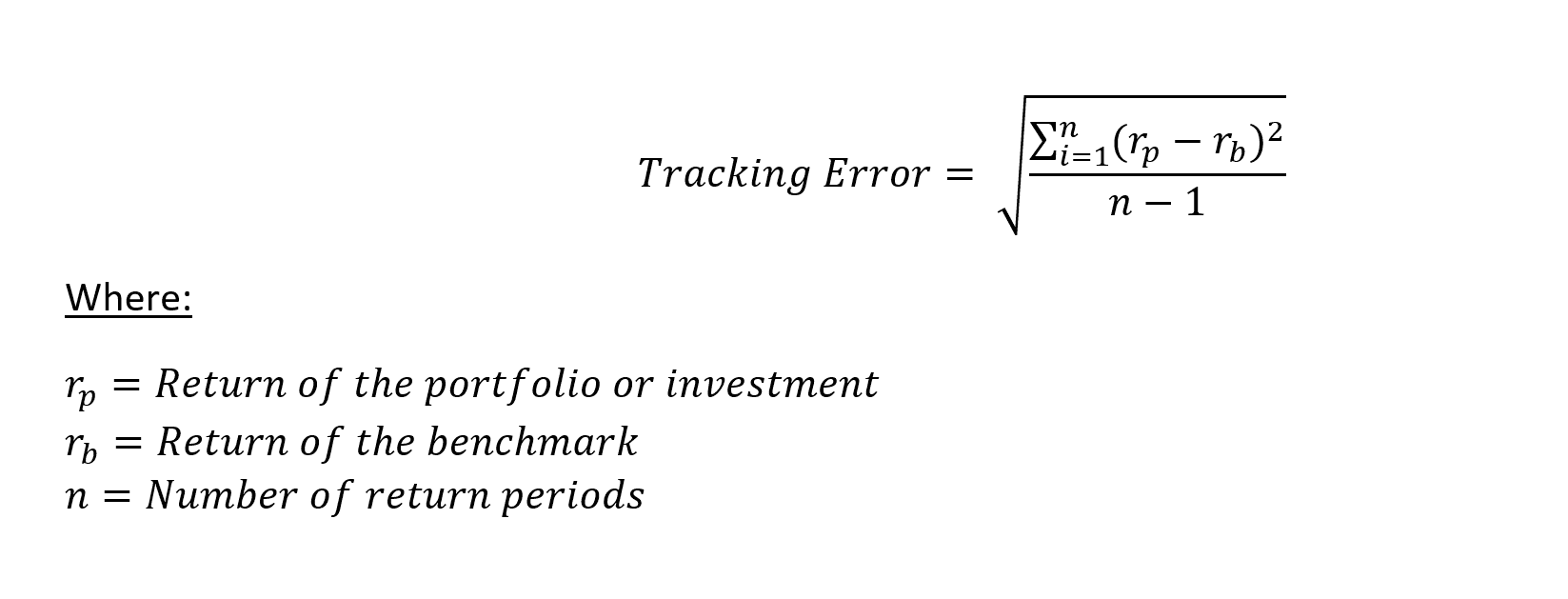

The Tracking Error Trade-off

The most immediate impact of ETF construction is seen in Tracking Error, defined as the standard deviation of the difference between the ETF’s returns and the index’s returns:

In a Full Replication model, tracking error should theoretically approach zero, minus the expense ratio. However, in "thick" markets like the S&P 500, the cost of holding 500 liquid names is negligible. The risk here is operational drag—the minute losses incurred during rebalancing or corporate actions.

In contrast, Sampling intentionally introduces tracking error. By selecting a representative subset—often used in fragmented markets like Emerging Market (EM) debt or High-Yield bonds—the manager bets that the sample’s factor exposures (duration, credit rating, sector) will proxy the whole.

During a liquidity crunch, a sampled portfolio may lack the specific security that drives index recovery, leading to a permanent "performance gap" that no low expense ratio can offset. This is because, in illiquid spaces, sampling prevents the fund from being a "forced buyer" of expensive, low-volume securities, potentially allowing the ETF to outperform the net-of-fee index by avoiding high transaction costs.

Tax Efficiency and the "In-Kind" Advantage

For taxable accounts, the construction method dictates the efficacy of the Heartbeat Trade and the general tax-loss harvesting capabilities of the fund.

A fully replicated fund must sell a security the moment it drops out of an index. If that security has appreciated significantly since the fund's inception, the sale triggers a capital gain. While the "in-kind" redemption process usually mitigates this, high-turnover replicated indices can still face "cash drag" or tax leakage if the manager cannot find an Authorized Participant (AP) to take the specific low-basis shares.

Sampling, on the other hand, gives the portfolio manager discretionary latitude. They can choose which specific tax lots to deliver to an AP during a redemption. By strategically shedding the lowest-basis shares through the sampling subset, a manager can keep the fund’s internal cost basis high, effectively "making" the portfolio by deferring capital gains indefinitely for the end client.

Structural Risk: Liquidity and Bid-Ask Variance

The "Break" scenario often occurs at the intersection of sampling and market stress. Professional managers must look at the implied liquidity of the ETF’s underlying basket.

When an advisor chooses a sampled ETF in a distressed asset class (e.g., CCC-rated corporate bonds), they are relying on the manager’s optimization algorithm. If that algorithm fails to capture the "tail risk" of the omitted securities, the ETF's NAV may plummet faster than the index it claims to track.

Conversely, a well-sampled fund "makes" the portfolio by providing liquidity in an asset class where the underlying components are essentially un-tradable in small lots.

From Oversight to Ownership: Bridging the Gap with Custom Models

Navigating the trade-offs between full replication and sampling is a core competency for any institutional manager, but identifying these structural nuances is only half the battle. The real challenge lies in execution: How do you translate these insights into a cohesive strategy that fits a client’s unique risk profile without getting bogged down in the operational weeds?

Whether you prefer the surgical precision of replication or the optimized efficiency of sampling, your ability to scale these decisions across a book of business is what defines your value proposition.

Design, Deploy, and Dominate with Surmount Wealth

We built our platform to give investment professionals the power of an institutional trading desk with the simplicity of a modern interface, enabling you to build high conviction, custom portfolios for your clients in minutes.

Precision Control: Define your own rules for replication or sampling.

Rapid Deployment: Push model updates across your entire client base with a single click.

Factor-Level Insights: Instantly see the overlap and drift within your custom sleeves.

Expertly Engineered Prebuilt Portfolios

Short on time but unwilling to sacrifice quality? Choose from our library of Prebuilt Portfolios.

Multi-Asset Coverage: Diverse strategies spanning global equities, fixed income, and alternatives.

Risk-Calibrated: Models categorized by risk levels and time horizons to match every client persona.

Institutional Rigor: Every prebuilt model undergoes the same rigorous construction analysis we’ve discussed today—ensuring your "beta" is as smart as your "alpha."

Experience the Future of Portfolio Construction

The difference between a "break" and a "make" for your portfolio often comes down to the tools at your disposal.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.