Blog

Integrating MSI Signals Into Portfolio Risk Management

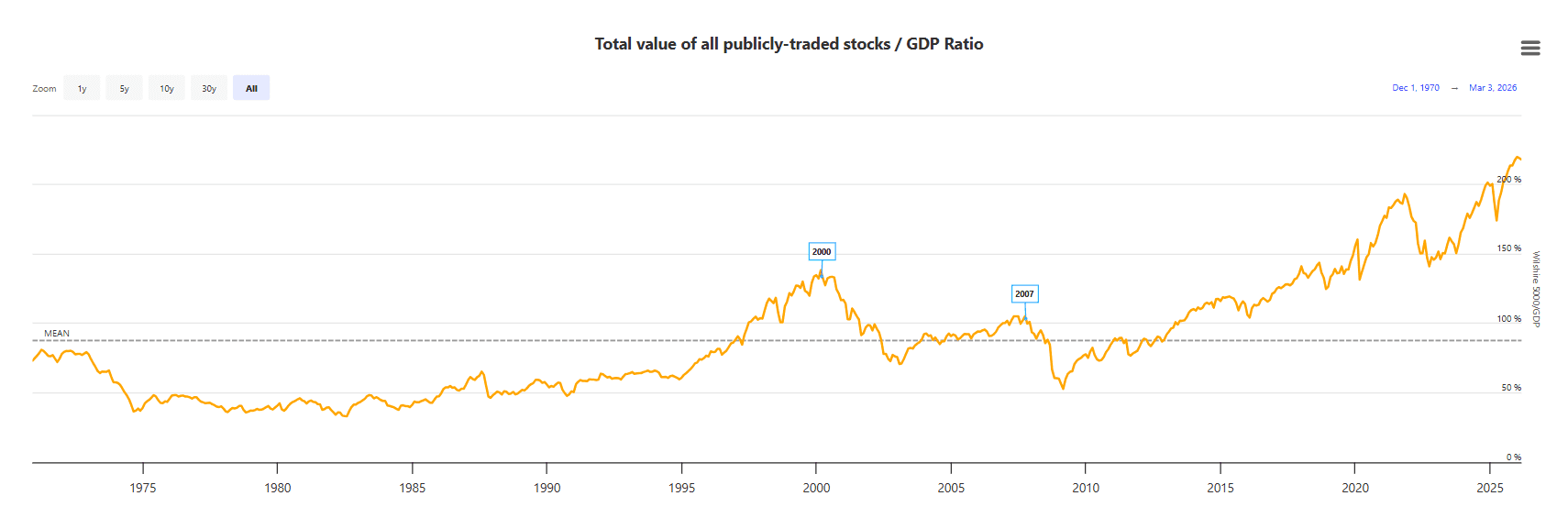

In the current investment landscape, the gap between fundamental valuation and price hinges on extreme levels, with the Buffett Indicator at a record high of 220%:

This is approximately 2.4 standard deviations above its historical trend line, a level categorized as "Strongly Overvalued".

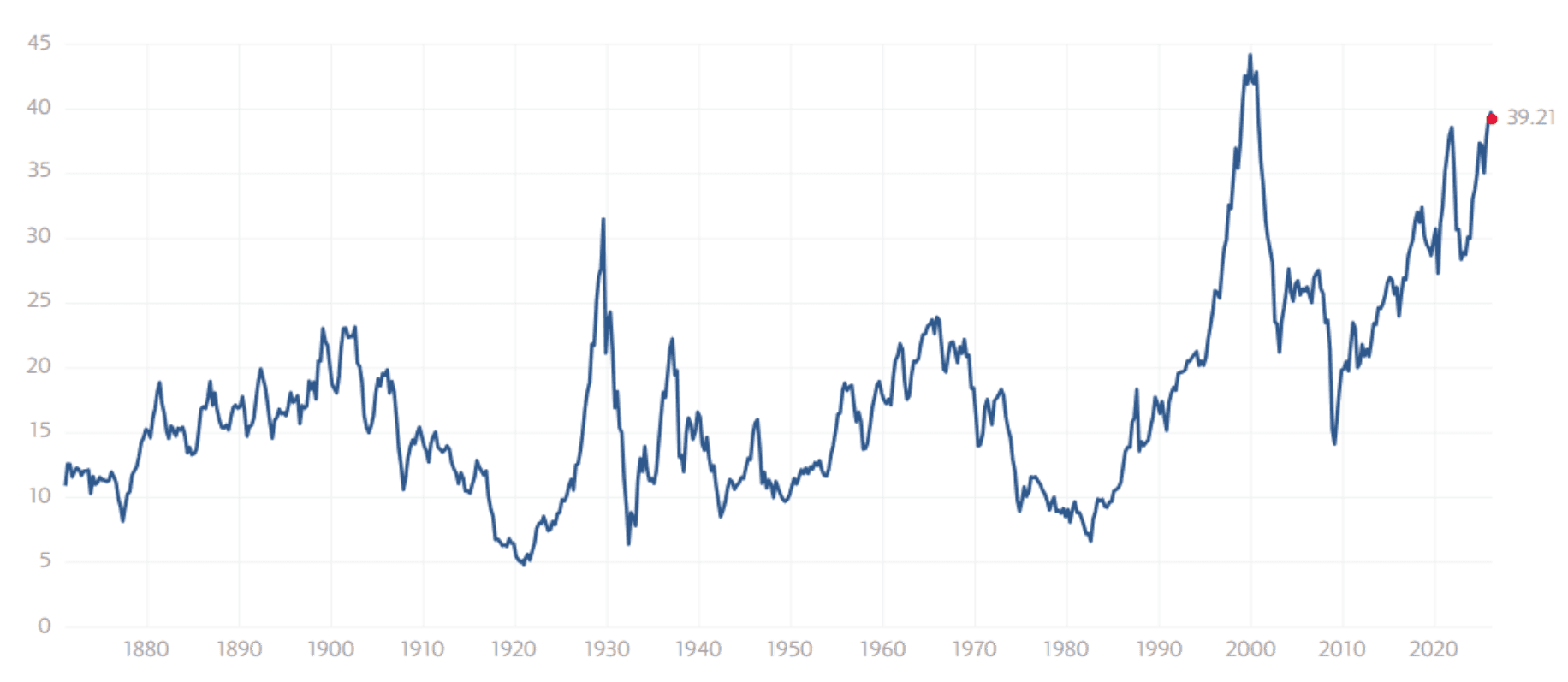

Similarly, the Shiller PE ratio is also at an extreme level, second only to the 2000 peaks of the dot com era:

Overall, we clearly see that traditional valuation metrics are flashing red, yet markets continue to exhibit a resilient, momentum-driven buoyancy.

For the professional portfolio manager, this creates a dangerous paradox. Relying on fundamentals alone invites "opportunity cost" risk during melt-ups, while ignoring them invites catastrophic drawdown risk.

This missing link to this dilemma is, of course, the quantification of sentiment.

With algorithmic dominance and rapid-fire information cycles, fundamental valuation tells you where the market should be, but Market Sentiment Indicators (MSI) tell you how market participants are behaving toward that valuation. When valuations become this extended, the primary driver of price action shifts from earnings growth to the psychology of the marginal buyer.

Integrating MSI signals into your risk management framework should not be seen as just a technical exercise; but rather should be treated as an essential layer of institutional defense. It moves your process from a static, valuation-anchored model to a dynamic, regime-aware strategy—allowing you to distinguish between a rational expansion and a speculative blow-off top before the mean reversion begins.

Integrating MSI into the Quantitative Risk Framework

Despite how important sentiment as a variable is to investing, it can be pretty misunderstood to many. Sentiment is not actually a binary buy/sell signal. It’s far more than that. Technically, sentiment operates as a volatility and conviction multiplier within your risk framework.

When you move away from treating sentiment as a directional crystal ball and begin treating it as a dynamic risk-weighting input, you transform your portfolio’s sensitivity to changing market regimes.

To institutionalize this, you must shift your perspective from timing to scaling. Sentiment data provides a high-fidelity look at the "crowding" of a trade—essentially telling you how much of the current price action is supported by fundamentals versus how much is driven by momentum and positioning.

There are three primary ways of achieving this:

1. Regime-Dependent Position Sizing

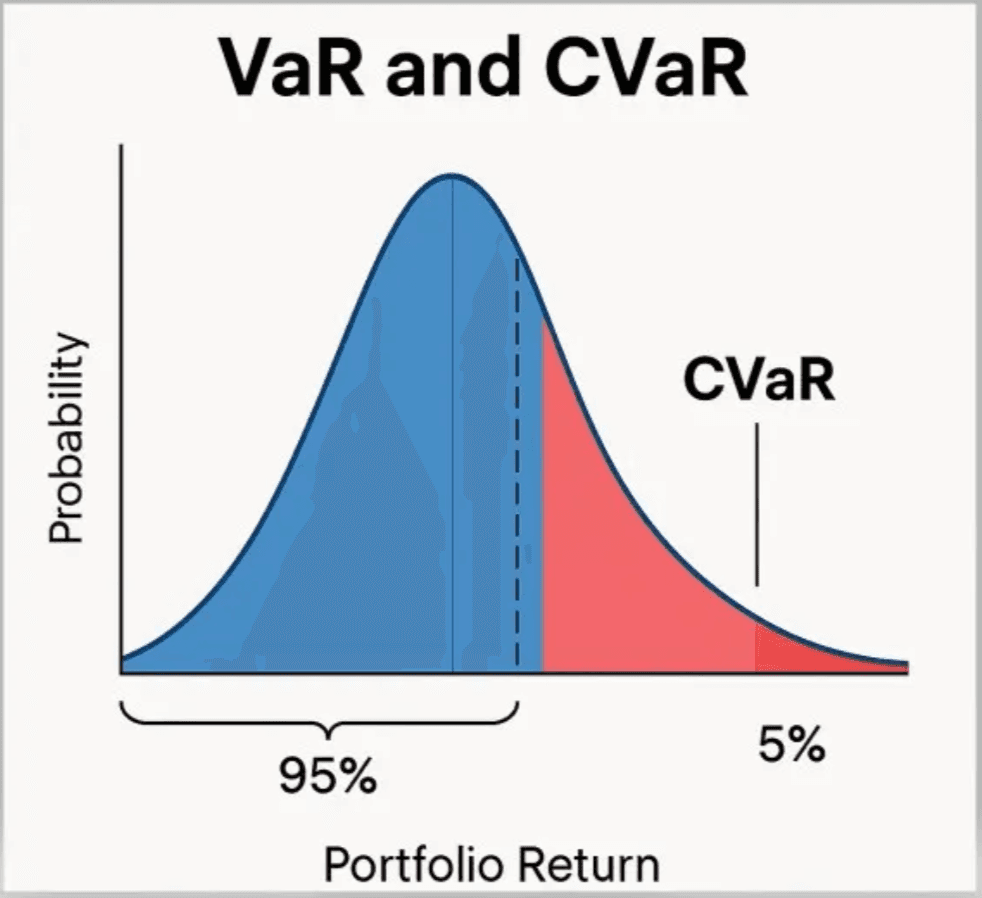

Your risk models should treat MSI as a volatility scaler. In institutional frameworks, we often use Value at Risk (VaR) or Conditional Value at Risk (CVaR) to manage exposure. By overlaying MSI onto these metrics, you can create a "Sentiment-Adjusted Volatility" model.

When sentiment registers at statistical extremes (such as greed), the probability of a "mean reversion" spike increases. Here, your risk engine should automatically reduce the confidence intervals in your model, essentially "taxing" the position size to account for the heightened risk of a sentiment-led pullback.

Conversely, during periods of capitulation, your models might show rising realized volatility. While a standard model would advocate for derisking, an MSI-integrated model recognizes the "exhaustion" signal, allowing you to maintain or add exposure when the sentiment floor is reached.

2. Breadth as a Risk-Control Circuit Breaker

One of the most persistent risks in modern portfolio management is hidden concentration. You may hold a diversified basket, but if the broader market is being held up by a tiny, sentiment-fueled segment of the index, your diversification is illusory.

One way to overcome this is to integrate market breadth indicators—such as the percentage of stocks above their 200-day moving average—as a circuit breaker. If the index makes a new high but your MSI-breadth metrics are contracting, the risk model should trigger a defensive shift (e.g., increasing hedge ratios or rotating into defensive sectors) regardless of what the price chart says.

Alternatively, during bouts of market panic, correlations tend to spike to 1.0. Your framework should use MSI to anticipate these regimes; when sentiment shifts from "complacency" to "nervousness," your model should preemptively adjust for the loss of diversification benefits that typically occurs during liquidity crunches.

3. The Sentiment-Based Beta Overlay

Think of your MSI inputs as an adaptive beta adjustment. Rather than maintaining a static target beta, use sentiment extremes to oscillate your beta exposure within a pre-defined range (e.g., ꞵ ± 0.15).

If sentiment signals an unsustainable level of optimism, your framework mandates a move toward the lower end of your beta target. This isn't "market timing" in the amateur sense; it is a systematic, rules-based approach to reducing downside capture when the crowd’s conviction is at its most fragile.

From Signal to Strategy: Institutional-Grade Implementation

Ultimately, a signal is only as good as the process that governs its execution. Implementing MSI into a portfolio isn’t about chasing the latest sentiment swing; it is about building a robust, repeatable framework that survives the scrutiny of an Investment Committee.

Filter for Macro-Confluence

Sentiment is a psychological indicator, not a fundamental one. To avoid the trap of "fighting the tape," sentiment signals should act as a secondary filter rather than a primary trigger.

One must never rely on a sentiment extreme in isolation. Instead, evaluate the signal against the prevailing macro-regime (e.g., liquidity, interest rates, or fiscal policy).

Similarly, a "Buy" signal during a period of market fear is only actionable if the underlying fundamental liquidity environment remains supportive. Using sentiment to time entries into an already fundamentally sound thesis is where the real alpha is captured.

Rigorous Backtesting and Sensitivity Calibration

Professionals demand to see the "math" behind the decision. Your implementation must address how the MSI signal behaves across multiple market cycles.

For instance, avoiding whipsaws is of utmost importance. Sentiment indicators can stay at extremes for long periods. You must establish clear "exit" and "re-entry" criteria based on the signal’s historical mean-reversion profile to prevent the portfolio from being whipsawed by brief volatility.

It is recommended to perform stress tests on your signal threshold. Does a move to the 90th percentile of sentiment historically demand an immediate 10% reduction in beta, or is it more efficient to scale out of positions?

Systematizing via the Investment Policy Statement (IPS)

The final step in institutionalizing MSI is integration into your operational workflow. Without formalizing the rules, human bias will almost always lead to ignoring the signal at the most critical moments.

Documented Triggers: Incorporate specific sentiment-based rules into your firm’s formal investment policy. This provides the fiaduciary cover necessary to maintain discipline during periods of high market stress.

Operational Integration: Ensure your risk management platform is configured to flag these signals in real-time, allowing for a structured review process. The goal is to move from "discretionary reaction" to "systematic response."

One of the best ways to ensure a smooth level of systemization is through Surmount’s pre-built or custom designed strategies. Get in touch now to get started.