Blog

Tax Diversification: The Most Underutilized Portfolio Allocation Strategy

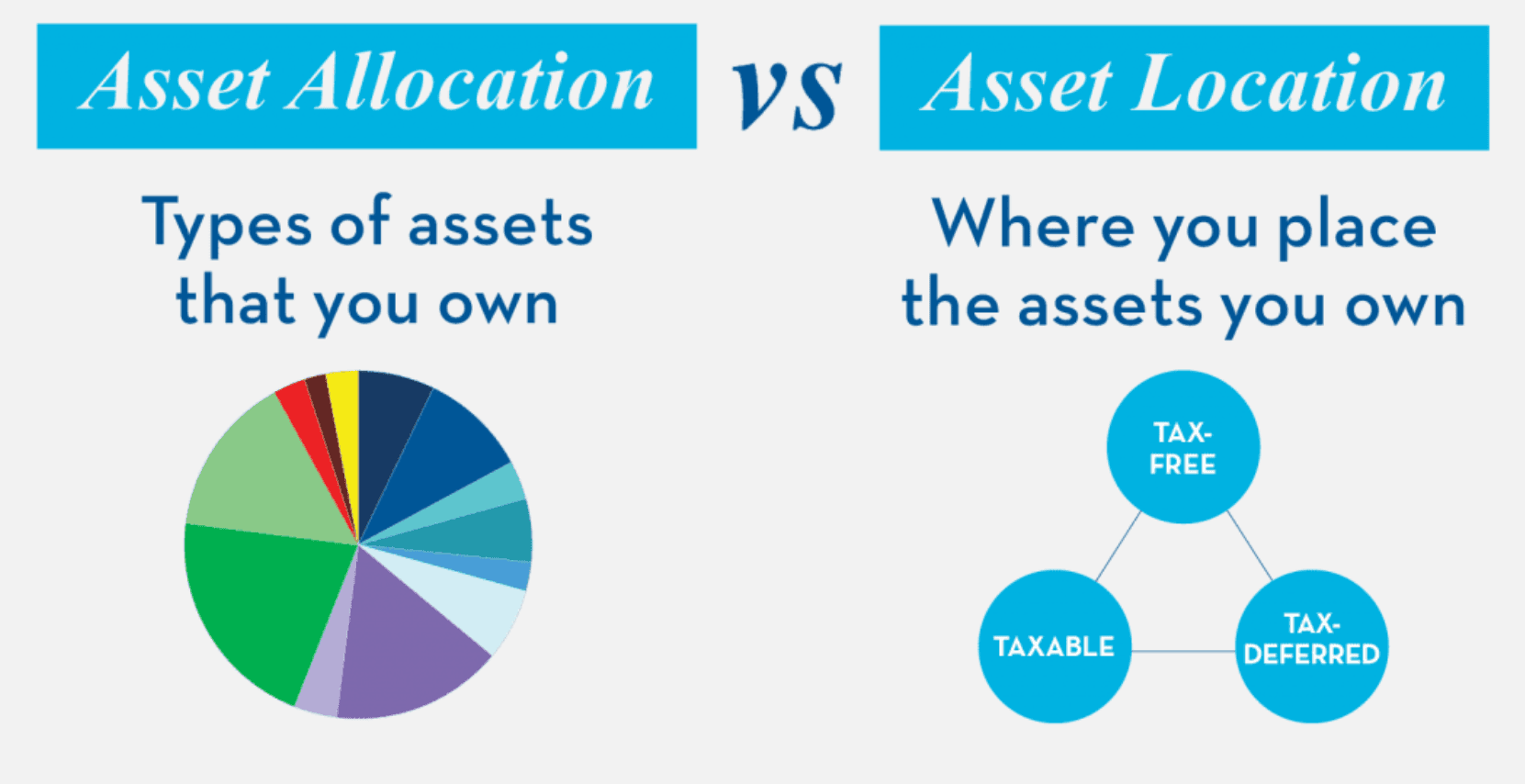

Asset allocation is widely considered the most important factor in determining a portfolio's long-term performance and risk level. This is, of course, rightfully so. According to a seminal academic paper published in 1986, approximately 94% of the variation in a portfolio's quarterly returns is explained by its asset allocation. That means that individual stock picking and market timing together accounted for less than 7% of the variability.

Yet, despite this focus on what we own, a critical piece of the wealth-building puzzle is consistently left on the table: where we own it.

In the industry, we call this Asset Location. While asset allocation dictates your exposure to market forces, asset location determines how much of your hard-earned growth actually lands in your pocket versus the government’s coffers. If you aren’t strategically positioning your investments across different tax environments, you are essentially letting a silent, compounding "tax drag" erode your returns year after year.

To maximize your net-after-tax wealth, you must evolve your strategy. You need to treat your tax structure as a primary asset class in its own right.

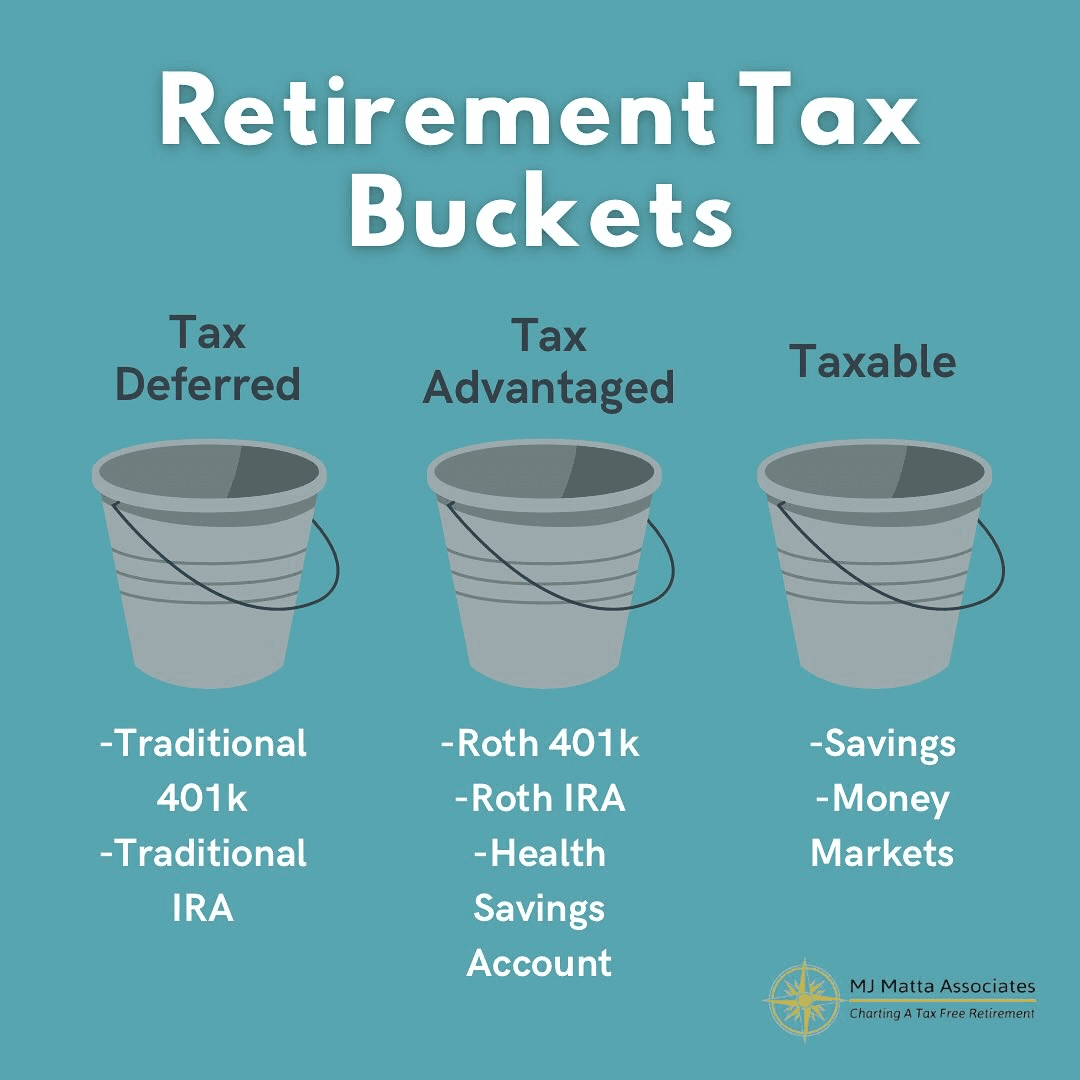

By organizing your capital into the right "buckets"—Tax-Deferred, Tax-Free, and Taxable—you stop viewing taxes as a post-script and start managing them as a core component of your portfolio's performance. It is time to move beyond simple diversification and embrace Tax Diversification: the most underutilized, yet potent, lever you have to accelerate your path to financial independence.

The Tax-Bucket Allocation Framework

To optimize your portfolio, you must view your net worth through three distinct lenses. By matching your investments to the right "bucket," you minimize the taxes you pay today and maximize the wealth you keep for tomorrow:

Strategic Placement: Where Does What Go?

The Taxable Bucket (The "Liquidity" Bucket)

This bucket provides the most freedom but the least tax protection.

Assets that make the most sense for this bucket include tax-efficient investments like broad-market index ETFs or municipal bonds. Avoid high-turnover funds or assets that pay high interest (like REITs or corporate bonds), as the annual tax bill will erode your returns.

Use this bucket for Tax-Loss Harvesting. Since you can realize losses here to offset gains elsewhere, this bucket is your best tool for managing your annual tax liability.

The Tax-Deferred Bucket (The "Growth" Bucket)

This is the home for assets that produce "tax-inefficient" income—money that would be taxed at your highest marginal rate if held in a standard brokerage account.

Ideally, in this bucket, you would want to hold assets that generate regular, taxable cash flow, such as high-yield corporate bonds, REITs (Real Estate Investment Trusts), or actively managed funds with high turnover.

By holding these in a 401(k) or Traditional IRA, you defer the tax hit, allowing your dividends and interest to reinvest at the full amount rather than being reduced by annual IRS leakage.

The Tax-Free Bucket (The "Power" Bucket)

This is your most valuable real estate. Because there is no future tax on withdrawals, this is where your "home runs" belong that will bring you tax alpha.

This bucket is for highly aggressive, high-growth assets. Think small-cap stocks, emerging markets, or individual stocks you believe will have the greatest long-term appreciation.

If you have an asset expected to grow significantly over the next 20 years, you want all that capital appreciation to occur in a place where the government cannot take a cut when you sell. If your portfolio doubles, you want that entire gain to be yours.

The Golden Rule of Location

The rule of thumb is simple: Hold your most tax-inefficient assets in your most tax-protected accounts. By shuffling your holdings into the appropriate buckets, you can often "engineer" an extra 0.5% to 1.0% of annual return without taking on any additional market risk. Over a 30-year career, that small delta can result in hundreds of thousands of dollars in additional terminal wealth.

Orchestrating Your "Tax Alpha"

Now tax diversification isn't a "set it and forget it" strategy; it is a dynamic process. If you don't actively manage the locations of your assets, your portfolio will naturally "drift" toward tax inefficiency. Creating Tax Alpha—the extra return generated by minimizing tax friction—requires deliberate orchestration.

To maintain your edge, you must synchronize three moving parts:

Strategic Asset Location (The Anchor): As your portfolio grows, continue to place your most tax-inefficient assets (like high-yield bond funds or REITs) in your Tax-Deferred buckets and your high-growth, high-turnover assets in your Tax-Free buckets.

Tactical Tax-Loss Harvesting: Within your Taxable bucket, treat your losses as assets. By systematically selling securities at a loss to offset capital gains, you lower your current-year tax liability while keeping your market exposure constant.

Dynamic Rebalancing: Rebalancing is usually about returning to your target asset allocation. To master tax diversification, you must also prioritize "Tax-Efficient Rebalancing." Instead of selling assets in a taxable account—which triggers a capital gains tax—rebalance by shifting new contributions or by selling within your tax-sheltered buckets.

The Withdrawal Sequence: Your Final Move

The ultimate expression of Tax Alpha occurs during the distribution phase. You are no longer just managing growth; you are managing a "pension" of your own design.

Draw from your accounts in an order that optimizes your marginal tax rate for that specific year. By strategically blending withdrawals from Taxable, Tax-Deferred, and Tax-Free buckets, you can often keep your taxable income significantly lower than your actual cash flow needs, effectively creating a "tax-free" retirement lifestyle.

Stop Manually Managing, Start Automating

Even with the best intentions, manual portfolio management is fraught with human error and emotional bias. Tax-efficient rebalancing and consistent tax-loss harvesting require real-time monitoring and data-driven execution—exactly what modern technology is designed for.

If you’re ready to move beyond manual spreadsheets and stop letting tax drag eat your returns, it’s time to consider a professional, automated approach.

Ready to optimize your portfolio?

At Surmount Wealth, we help investors move from reactive management to proactive wealth-building. Whether you are looking for pre-built, professionally-engineered strategies designed to capture market opportunities, or you have a specific thesis you want to turn into a custom automated model, our platform gives you the tools to put your strategy on autopilot.

Book a demo today to see how you can unify your accounts, implement systematic tax-efficiency, and let data-driven AI work for your portfolio 24/7.