Blog

Technical Implications of Decelerating Wage Growth Trends

For the better part of the post-pandemic cycle, the "wage-price spiral" has been a primary concern for the FOMC and a central variable in portfolio duration strategies.

In particular, the concerns revolve around the following specific dimensions:

The Fear of Persistence: The FOMC has been concerned that if workers demand higher wages to keep up with rising prices, firms would raise prices further to cover labor costs, creating a continuous feedback loop.

Labor Market Tightness: A very tight labor market, where job openings outnumber workers, is a key component of this concern, as it gives workers more bargaining power.

Monetary Policy Response: To avoid a de-anchoring of long-run inflation expectations, the Fed has utilized a contractionary monetary policy (rate hikes) to cool labor demand and ensure that wage growth does not lead to 3 percent or higher inflation.

Current Standing: As of late 2025/early 2026, many argue that a "traditional" wage-price spiral is unlikely due to a softening labor market, but it remains a risk factor monitored by Fed officials.

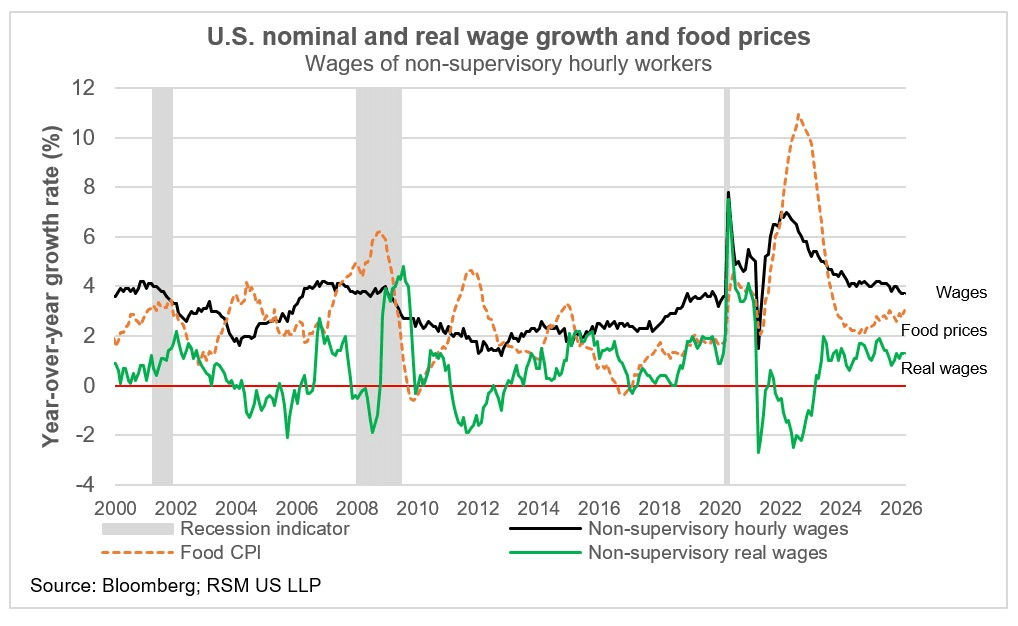

However, current data suggests we may have reached a critical inflection point. As of March 2026, the deceleration in nominal wage growth—dropping to 3.9% year-over-year from the 4.5%–5.0% corridor maintained throughout 2024—signals a cooling labor market, and more critically, a weakening feedback loop that previously sustained consumer resilience.

While a slowdown in wage growth is typically cheered by equity markets as a harbinger of a more dovish Federal Reserve, the current macro-regime offers no such simplicity. The technical concern for investment advisors is the widening "Real Income Gap." While nominal wages are trending down, core inflation remains buoyed by structural headwinds, including aggressive new tariff regimes and supply-side shocks in the energy sector. When nominal wage growth falls below the "sticky" floor of core goods inflation, real disposable income enters a contractionary phase.

For the professional specialist, this deceleration is the "canary in the coal mine." It indicates that the US economy is transitioning from a period of demand-pull inflation—where higher wages funded higher prices—to a late-cycle period of margin compression and declining solvency.

We are no longer observing a "return to normal"; we are witnessing a fundamental shift in the consumer’s ability to service the record levels of leverage seen in auto and credit markets.

The "Operating Leverage" Reset

The primary concern for equity analysts during inflationary cycles is the "wage-price spiral" eating into bottom-line results. However, a closer look indicates that output prices seem to remain "sticky" while labor input costs begin to mean-revert.

Margin Expansion Dynamics: As nominal wage growth decelerates—specifically as measured by the Employment Cost Index (ECI) rather than the more volatile Average Hourly Earnings—companies with high operating leverage stand to benefit.

If a firm’s revenue grows at 4% while its labor costs (often 20–30% of OpEx) slow from 6% to 3%, the resulting margin expansion is non-linear.

Sector-Specific Sensitivity: We must differentiate between "Price Takers" and "Price Makers." In labor-intensive sectors like Healthcare and Professional Services, the delta between the Rate of Change (RoC) in wages and the RoC in service pricing is the most critical variable for earnings surprises in the coming quarters.

The Phillips Curve and the "Non-Linear" Labor Supply

Technically, the market is currently testing the slope of the Phillips Curve. The traditional view suggests that lower wage growth requires higher unemployment. However, the current "Quantitative Transmission" suggests a rebalancing via the Beveridge Curve.

The deceleration in wages is currently being driven by a collapse in "Job Openings" (JOLTS data) rather than a spike in initial jobless claims. For advisors, this is a signal that the "labor shortage" premium is evaporating without triggering the negative feedback loop of a consumer spending collapse.

The most vital metric for the technical analyst is the convergence of ULC with the Fed’s 2% inflation target. If productivity growth holds steady while wages cool, the inflationary impulse of the labor market is neutralized, allowing for a higher "Return on Invested Capital" (ROIC) across the board.

The Real Rate Path and Term Premia

Decelerating wages act as a "term premia suppressor" in the Treasury market. As wage growth cools, the market’s expectation for "embedded" long-term inflation falls. This reduces the volatility of inflation expectations, which in turn compresses the term premium on the 10-year and 30-year yields.

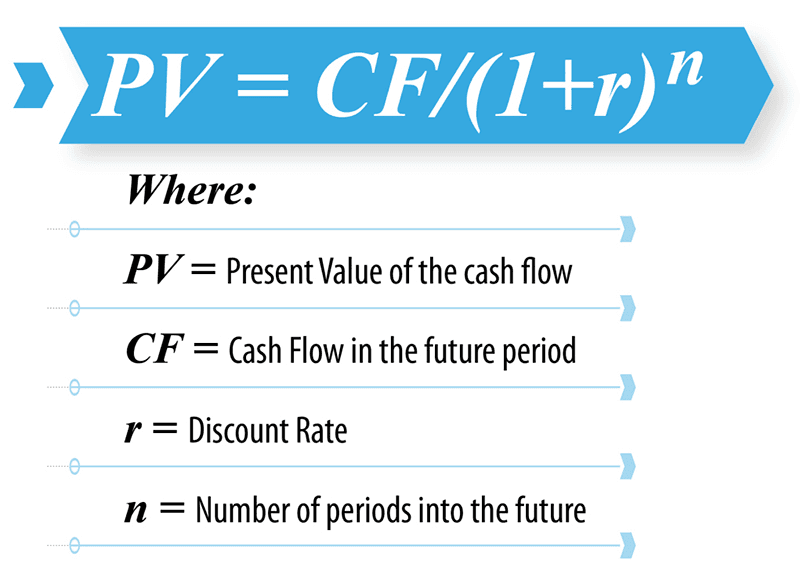

In the standard Discounted Cash Flow (DCF) model:

If decelerating wages allow the Fed to lower the terminal rate (decreasing r), the present value of long-duration assets—particularly Growth and Technology equities—increases, provided the cooling wages do not signal a deep recessionary collapse in CF (Cash Flow).

The Equilibrium Signal

Portfolio managers should monitor the Real Wage Gap (the difference between nominal wage growth and realized CPI). A positive but narrowing gap suggests a sustainable path for consumption that doesn't force the Fed’s hand.

The technical goal is to identify the "inflection point" where wage growth levels off at a rate compatible with productivity gains (roughly 3% to 3.5%), which traditionally marks the stabilization of the long-run neutral rate.

The Multiplier Effect: Consumption Elasticity and Systemic Liquidity

As wage growth decelerates, the primary concern for portfolio managers shifts from inflation control to the marginal propensity to consume (MPC). In an environment where nominal wage gains are no longer outpacing historical norms, the technical "multiplier effect" that sustained the post-pandemic recovery begins to lose its inertia.

Consumption Elasticity: The Shift from Income to Credit

With nominal wages cooling, the sensitivity of consumer spending to changes in disposable income—income elasticity of demand—becomes more pronounced. We are moving away from a "spend at any cost" regime toward one where consumers are increasingly sensitive to price and interest rates.

The Discretionary Pivot: High-value advisors should watch for a divergence in spending patterns. When wage growth slows, the "Income Effect" suggests a pullback in discretionary services, but the "Substitution Effect" may drive flows toward lower-cost staples.

The Wealth Effect Offset: A critical technical nuance is the degree to which asset price appreciation (equities/housing) can bridge the gap. If the "Wealth Effect" remains strong, the drag from lower wages may be mitigated, complicating the Fed's attempts to cool the "overheated" economy.

Systemic Liquidity and the Velocity of Money

Decelerating wages have a direct impact on M2 velocity. Higher wages generally circulate more quickly through the economy; as that growth slows, the velocity of money tends to dampen.

Savings Rate Normalization: As the wage premium vanishes, the personal savings rate—which was depleted during the inflation spike—may see a forced "re-stocking." This shift from consumption to defensive saving effectively drains liquidity from the retail economy, exerting downward pressure on corporate top-line growth.

The Credit Impulse: With less "organic" cash flow from wages, the reliance on credit (revolving debt) increases. For credit analysts, this is the point where delinquency vectors begin to shift, especially in sub-prime and lower-tier consumer paper, as the "wage cushion" disappears.

Portfolio Positioning: Duration and Quality Factors

From a construction standpoint, this cooling multiplier suggests a rotation is necessary.

As the disinflationary impulse of slower wages solidifies, the technical case for increasing portfolio duration strengthens, as the "inflation risk premium" in the term structure fades.

In a regime of slowing consumption elasticity, companies with high operating leverage are at risk. Advisors should favor "Quality" factors—firms with robust balance sheets and low labor-intensity—that can maintain margins even as the broader "multiplier effect" of the labor market wanes.

Monitor the Real Wage Gap (Nominal Wage Growth minus Core PCE). When this narrows or turns negative, the systemic liquidity transition from "expansionary" to "restrictive" is technically confirmed, regardless of where the Fed Funds Rate sits.

Capitalize on the Disinflationary Impulse: Automate Your Edge

The transition from a wage-push inflation regime to a period of labor normalization creates a distinct window of opportunity for tactical asset allocation. However, in a market where the delta between a "soft landing" and a "policy error" is measured in basis points, execution speed and emotional discipline are your most valuable assets.

Don't let your macro thesis sit idle as a PDF or a static spreadsheet. At Surmount Wealth, we bridge the gap between high-level investment strategy and systematic execution.

From Thesis to Trade, Automatically

Whether you are looking to hedge against a shift in the Phillips Curve or capitalize on sector-specific margin expansion, Surmount provides the institutional-grade infrastructure to build, backtest, and deploy:

Prebuilt Quant Strategies: Access our library of professionally vetted, automated strategies designed to navigate various interest rate and labor environments.

Bespoke Customization: Have a proprietary view on the wage-growth-to-yield-curve correlation? Use our intuitive platform to code and automate your specific logic without the need for a full-scale dev team.

Rules-Based Rigor: Remove the behavioral biases of manual trading. Our systems monitor the technical signals 24/7, ensuring your portfolio reacts to data, not headlines.

Your Strategy, Systematized

The macro environment is shifting—is your execution model keeping up? See how Surmount Wealth empowers advisors and portfolio managers to scale their best ideas with precision.

[Book a Demo Today] and discover how to automate your edge in the next market cycle.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.