Blog

REITs as an Inflation Hedge: What Lease Structures Reveal

Inflation does not affect all real estate equally. While the narrative around using a REIT inflation hedge has become mainstream in institutional circles, most of the conversation stops at the sector level — apartments good, offices bad — without ever explaining the mechanism underneath. That mechanism is lease structure, and understanding it is what separates a well-constructed real estate allocation from one that merely looks inflation-resistant on paper.

In the past we discussed the idea of REITs as a deflationary hedge in the context of the AI boom. In this piece, we flip the lens, and examine how lease reset structures determine which REIT sectors actually deliver on the inflation hedge promise when prices are rising.

Why Inflation Pass-Through Varies Across Real Estate

When inflation rises, investors expect real assets to keep pace in the form of REIT returns. But inflation pass-through in real estate — the degree to which rising prices translate into rising landlord income — is not automatic. It depends almost entirely on how frequently a lease allows the landlord to reprice.

How Lease Reset Frequency Drives NOI Growth

A landlord can only capture inflation through rent when a lease expires or contains an escalation clause tied to a price index. The shorter the lease, the more frequently the landlord can reset to market rates. This is the direct link between lease reset frequency and NOI growth during inflationary periods. A portfolio with rapid lease turnover is structurally positioned to convert CPI increases into revenue — one locked into long fixed-term contracts is not, regardless of how strong the underlying asset quality may be.

Short Duration Leases vs Long Duration Leases: The Core Tradeoff

Short duration leases offer inflation responsiveness at the cost of income predictability. Long duration leases offer income stability at the cost of real return erosion when prices rise. Neither is inherently superior — but in an inflationary environment, the repricing optionality embedded in short-duration structures becomes a genuine competitive advantage. This tradeoff sits at the heart of any serious REIT inflation hedge analysis.

REIT Property Type Comparison: Who Wins When Inflation Rises

Understanding this tradeoff across sectors is where the real estate sector inflation comparison gets interesting — and where portfolio positioning decisions should actually be made. This is particularly the case when capital intensity and WACC advantages vary significantly across property types.

Multifamily REIT Lease Reset: The Repricing Advantage

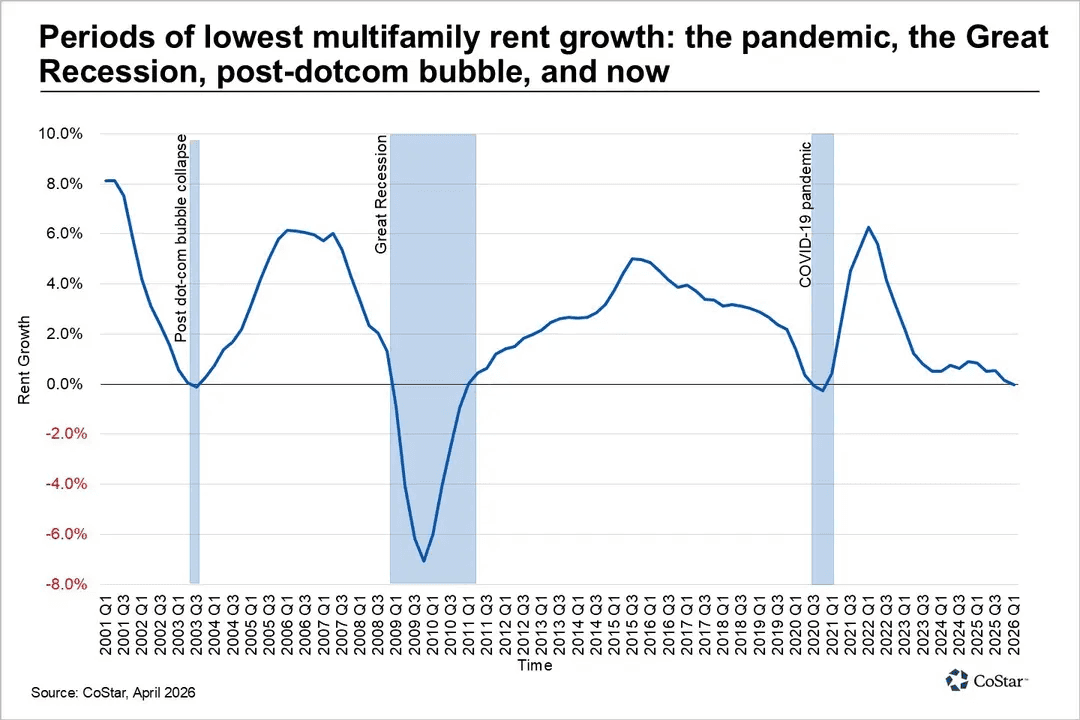

Apartment leases typically run twelve months. That annual reset cycle means multifamily landlords are effectively renegotiating their entire revenue base every year, capturing prevailing market rents as they move. During sustained inflationary periods, this multifamily REIT lease reset cadence becomes a compounding advantage.

Each renewal cycle layers current rates onto the prior year's already-elevated base — a compounding dynamic that, as we've previously argued, the market frequently misprices when reading REIT earnings signals.

This dynamic is the most direct, structurally embedded form of inflation pass-through available in listed real estate, which is a key reason apartment REITs consistently feature in REIT inflation hedge discussions among portfolio managers.

It is also important to keep view of the broader macro trends and shocks that impacts the multifamily rent growth trajectory:

Industrial REITs and the Hidden Inflation Risk in Long-Term Leases

Industrial REITs have attracted significant capital in recent years on the back of e-commerce demand and supply chain reconfiguration. The operational thesis is sound. The inflation thesis is more nuanced. Industrial leases frequently run five to ten years, with fixed or CPI-capped escalations that may not keep pace with actual inflation. When comparing apartment REIT vs industrial REIT dynamics through an inflation lens, industrial's longer lease durations can create a lag effect — strong nominal income, but quietly eroding real returns during high-inflation regimes. Investors should examine lease expiration schedules carefully rather than assuming sector tailwinds are sufficient protection.

Retail and Office REITs — Inflation Sensitivity at the Edges

Office REIT inflation sensitivity is structurally challenged for reasons that compound beyond lease duration. Typical office leases run seven to ten years, limiting repricing frequency. More importantly, the structural demand headwinds facing the sector mean occupancy risk increasingly dominates any inflation conversation. Vacancy is the enemy of inflation pass-through regardless of lease terms.

Retail REIT vs multifamily inflation dynamics follow a similarly complex path. Anchor tenant leases in retail can run ten to twenty-five years, though smaller inline tenants turn over more frequently. The sector's inflation resilience depends heavily on tenant mix, location quality, and whether percentage rent clauses — which tie landlord income to tenant sales — are present and structured effectively.

NNN Lease vs Gross Lease — Inflation Risk in Commercial Real Estate

The NNN lease vs gross lease inflation debate often gets overlooked but is material. In a triple net lease inflation arrangement, the tenant absorbs operating cost increases — taxes, insurance, maintenance — directly. This protects the landlord from rising operating expenses but does not solve the repricing problem if the base rent is fixed for a long term. Gross leases expose landlords to operating cost inflation directly. Neither structure is a complete inflation hedge on its own — the base rent reset mechanism remains the dominant variable in both cases.

Building an Inflation-Resilient Real Estate Portfolio

A thoughtful real estate inflation protection portfolio does not simply overweight one sector. It maps lease reset frequency, escalation clause quality, occupancy stability, and balance sheet strength across holdings to model actual inflation pass-through capacity — treating real assets inflation hedge potential as a quantifiable characteristic rather than a marketing label.

Positioning Across REIT Sectors in a Rising Rate Environment

In a rising rate environment REIT strategy must account for a tension that is easy to overlook: the same inflation that benefits short-duration landlords through repricing also raises financing costs and compresses cap rate-driven valuations. The sectors most capable of passing through inflation — primarily multifamily — tend to also carry the valuation sensitivity that rate increases punish. Inflation hedging strategies for institutional investors therefore require balancing repricing capacity against duration risk at the portfolio level, not optimizing for one variable in isolation.

This is the same dynamic that sits within the broader challenge of allocating adaptively under a data-dependent Fed.

Conclusion — Lease Structure Is the Signal Most Investors Miss

Most REIT inflation hedge analysis starts and ends with sector selection. The more precise analysis begins with lease structure — reset frequency, escalation clause design, and lease expiration schedules. These are the variables that determine whether inflation actually flows through to investor returns, or quietly erodes them instead. Multifamily's annual reset cycle remains the most structurally direct inflation pass-through mechanism in listed real estate. That does not make it universally superior, but it does make it the clearest signal in the comparison — and the one most worth building around when constructing real estate allocations for inflationary regimes. This is why portfolio managers typically show preference for this category of income-generating alternative assets.

Automate This Thesis With Surmount Wealth

Understanding the mechanics of a REIT inflation hedge is one thing. Executing on it systematically — rebalancing sector weights as macro conditions shift, rotating between multifamily and industrial exposure as the inflation cycle evolves, trimming rate-sensitive positions when the Fed signals — is where most advisors lose the edge their analysis should have delivered.

That is exactly the problem Surmount Wealth is built to solve.

Surmount's platform allows investment professionals to build, test, and fully automate rule-based strategies across real estate and broader asset classes — without writing a single line of code and without moving client funds away from existing brokerage accounts.

Hypothetical Strategy Illustration — "Lease Reset Rotator" (Concept Only)

Imagine a strategy that systematically overweights multifamily REITs when trailing CPI readings exceed 3% and the 10-year yield spread over the Fed Funds Rate compresses — signaling that inflation is running ahead of rate containment. As CPI cools below a defined threshold, the strategy rotates exposure toward longer-duration industrial and net lease REITs to capture yield stability. Rebalancing triggers are rule-based and execute automatically. No discretionary intervention required.

This is a hypothetical concept for illustrative purposes only and does not represent an actual deployed strategy or investment advice.

This is the kind of thesis-driven, macro-responsive automation Surmount makes possible. Whether you are working from a published framework, your own proprietary research, or a strategy built from scratch, the platform gives you the infrastructure to run it with precision and consistency.

Stop leaving execution to chance. Book a demo with Surmount Wealth today and see how your next macro thesis can be automated from idea to live portfolio.

FAQ: REIT Inflation Hedge

Why aren't all REITs equal inflation hedges?

Lease reset frequency determines how quickly landlords can reprice rents to match inflation. Without frequent resets, rising prices erode real returns regardless of asset quality.

Which REIT sectors benefit most from inflation?

Multifamily REITs offer the strongest inflation pass-through due to annual lease resets that reprice the entire revenue base every twelve months. Industrial and net lease REITs lag because longer lease durations limit repricing opportunities.

How does a triple net lease affect inflation risk?

A triple net lease shifts operating cost increases to the tenant, protecting landlord margins from rising expenses. However, fixed base rents on long-term NNN leases still erode real NOI growth during sustained inflation.

When should investors rotate between REIT property types?

Rotate toward multifamily REITs when CPI is rising and rate containment is lagging, maximizing inflation pass-through through frequent lease resets. Shift toward longer-duration industrial or net lease REITs as inflation cools and yield stability becomes the priority.

Why does lease reset frequency drive REIT returns?

Lease reset frequency is the direct mechanism connecting inflation to NOI growth — the more frequently rents reprice, the more inflation translates into real revenue gains. It is the variable most investors overlook when building a real estate inflation protection portfolio.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.