Blog

Real Estate vs Stocks: A Risk-Adjusted Return Guide

The real estate vs stocks debate has followed advisors into nearly every client conversation about diversification. Clients read a headline, see a friend's rental property “return,” and ask why their portfolio isn't doing the same. But raw return comparisons miss the point. The real question in real estate vs stocks decisions isn't which asset appreciated more — it's which asset delivered more return per unit of risk taken.

For a broader look at where real estate fits alongside other non-traditional holdings, see our alternative assets primer.

Why the Real Estate vs. Stocks Debate Needs a Risk-Adjusted Lens

Comparing real estate vs stocks on price appreciation alone ignores three variables that matter far more to portfolio outcomes:

Volatility — how much the asset's value swings year to year

Liquidity — how quickly and cheaply the asset converts to cash

Leverage exposure — how much borrowed capital is embedded in the “return”

A rental property that appreciated 6% annually while carrying a mortgage, tenant vacancy risk, and $30,000 in unplanned repairs is not comparable to a 6% equity return with none of those frictions. Risk-adjusted analysis strips out the noise and isolates what advisors actually need: comparable, decision-useful data.

Sharpe Ratio Real Estate vs. Stocks: Measuring Risk-Adjusted Return

The Sharpe ratio remains the most widely used starting point for this comparison. It measures excess return per unit of volatility, and it's where the real estate vs stocks conversation gets more interesting than headline appreciation numbers suggest.

Rooted in Modern Portfolio Theory's efficient frontier concept — which we break down here — it measures excess return per unit of volatility.

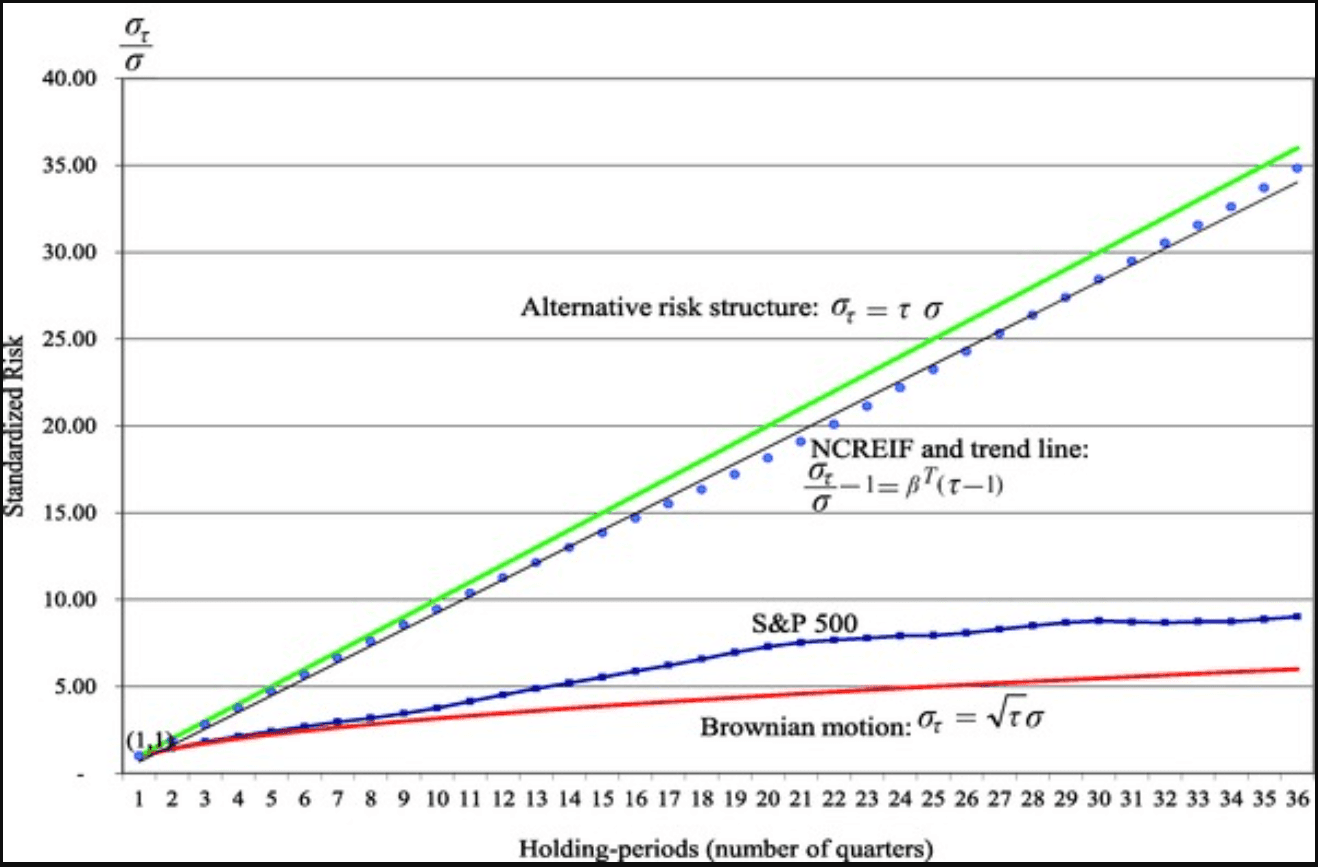

Public equities, despite higher year-to-year volatility, have historically posted Sharpe ratios that hold up well against direct real estate once financing costs, maintenance, and vacancy risk are factored in. Direct property ownership often shows artificially smoothed volatility simply because it isn't marked-to-market daily — not because the underlying risk is lower.

How Volatility Drag Erodes Long-Term Equity Returns

Critics of equities point to volatility as a weakness. But volatility drag — the gap between average returns and compounded returns caused by sequential losses — cuts both ways. Real estate isn't immune to it; it's simply harder to observe because valuations update infrequently. A diversified equity portfolio experiences volatility drag transparently, which makes it easier to model, stress-test, and manage systematically.

Illiquidity Premium in Real Estate: Real Return or Illusion?

Advisors often hear that real estate's illiquidity premium justifies its inclusion — investors are theoretically compensated for tying up capital. In practice, this premium is inconsistent:

It varies significantly by market cycle and geography

It's frequently offset by transaction costs, financing spreads, and holding costs

It rarely accounts for the opportunity cost of capital sitting in an illiquid asset during a market drawdown

For clients who may need portfolio flexibility, the illiquidity premium is a real but unreliable source of excess return.

We break down how to size and manage this exposure in our guide to managing real estate risk in client portfolios without sacrificing long-term returns.

Correlation Between Real Estate and Equities in a Diversified Portfolio

Diversification value depends on correlation, not just standalone returns. Direct real estate has historically shown low-to-moderate correlation with public equities, which is the strongest argument in its favor. However:

REITs, which are publicly traded, correlate far more closely with equities than direct property ownership does

Correlation benefits from direct real estate come with a liquidity cost that many diversification models don't price in

During systemic shocks (2008, for example), correlations across asset classes — including real estate and equities — tend to converge upward, reducing the diversification benefit precisely when it's needed most

This is a critical nuance for client conversations — a dynamic we explore further in REITs as an inflation hedge, where lease structures play a bigger role than most advisors assume. Diversification benefits aren't static, and they weaken during the periods that matter most.

Portfolio Diversification in Real Estate: Building a Risk-Adjusted Framework

A defensible real estate vs stocks framework for client portfolios should weigh four factors side by side:

For a deeper framework on structuring diversification more broadly, see our 2025 portfolio diversification guide.

Factor | Direct Real Estate | Public Equities |

|---|---|---|

Liquidity | Low | High |

Volatility (observed) | Low (smoothed) | Higher (transparent) |

Correlation to equities | Low-moderate | N/A |

Leverage embedded | Often high | Client-controlled |

Rather than treating this as an either/or decision, the more useful advisor framing is: what role does each asset play, and how much risk is the client actually taking to get there?

Applying Systematic Asset Allocation to the Real Estate vs. Stocks Decision

This is where systematic asset allocation earns its place. Instead of relying on anecdotal client comparisons (“my friend made X on their rental”), a rules-based approach applies consistent risk-adjusted criteria — volatility targets, correlation thresholds, liquidity minimums — across every allocation decision. This removes recency bias and anecdote-driven portfolio drift, replacing it with a repeatable process.

This is the same principle we detail in why rebalancing matters more than market forecasts.

Conclusion

The real estate vs stocks question isn't really about which asset wins. It's about whether a client's portfolio is allocated based on a defensible, risk-adjusted process — or based on headline returns and dinner-table anecdotes. For advisors, the ability to reframe this conversation using Sharpe ratios, correlation data, and a clear-eyed view of the illiquidity premium is what separates a credible allocation recommendation from a guess.

From Framework to Execution: Automating the Real Estate vs. Stocks Decision

Understanding the risk-adjusted case for real estate vs stocks is only half the battle. The harder part — for advisors managing multiple client portfolios — is operationalizing that framework consistently, without relying on manual rebalancing triggered by gut feel or quarterly reviews.

This is precisely the gap Surmount Wealth's automated strategy engine is built to close.

Surmount Wealth lets advisors and self-directed investors apply professional-grade, rules-based algorithms directly to existing brokerage accounts — no fund transfers, no custom code required. Any thesis, including the risk-adjusted allocation logic discussed in this piece, can be systematized and run automatically.

As a hypothetical illustration, consider a strategy concept like a “Correlation Drift Monitor”:

Continuously tracks the rolling correlation between REIT exposure and broad equity indices

Flags when correlation regimes shift upward — the exact scenario where diversification benefits erode, as discussed above

Automatically rebalances allocation weights when correlation crosses a pre-set threshold, rather than waiting for a scheduled review

Applies consistent, backtested rules instead of anecdote-driven adjustments

This is a hypothetical strategy concept for illustrative purposes only and does not represent an actual Surmount Wealth product offering, investment advice, or a guarantee of performance. All investing involves risk, including the potential loss of principal.

Why Advisors Are Automating Strategies Like This

Consistency: Rules apply the same way every time — no recency bias, no dinner-table anecdotes influencing allocation

Speed: Reacts to correlation and volatility shifts in real time, not at the next quarterly rebalance

Transparency: Every rule and trigger is visible and auditable — critical for client conversations and compliance documentation

No migration required: Strategies run on top of existing brokerage accounts, with no need to transfer assets or build from scratch

Scalability: Apply the same systematic logic across dozens or hundreds of client portfolios simultaneously

If you're already having the real estate vs stocks conversation with clients, the next step is making sure your portfolio construction process reflects it systematically — not just in a one-off spreadsheet.

See how Surmount Wealth can help you build and automate a strategy like this for your practice. Book a demo now →

FAQ: Real Estate vs Stocks

What is real estate vs stocks?

Real estate vs stocks refers to comparing risk-adjusted returns between direct property ownership and public equities for portfolio allocation.

Which has better risk-adjusted returns?

Public equities often show stronger Sharpe ratio real estate vs stocks comparisons once financing costs and illiquidity are factored in.

Why does correlation matter here?

Low correlation between real estate and equities supports diversification, but it weakens during systemic market shocks.

Is the illiquidity premium reliable?

The illiquidity premium in real estate varies by cycle and is often offset by transaction and holding costs.

How can advisors automate this decision?

Systematic asset allocation applies consistent, rules-based criteria instead of relying on anecdotal client comparisons.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.