Blog

How Advisors Are Reducing Dollar Exposure Amid Reserve Currency Debate

The debate over the dollar's reserve currency status has moved from academic circles into daily conversations among portfolio managers and RIAs. Clients are asking pointed questions, and “wait and see” is no longer a satisfying answer. For advisors, reducing dollar exposure has shifted from a theoretical hedge to a practical portfolio consideration that deserves a structured response.

This isn't a call to abandon dollar-denominated assets or predict imminent currency collapse. It's a framework for thinking clearly about concentration risk in a single currency — and for building portfolios resilient enough to withstand a range of outcomes, through currency management, not just the consensus one.

Why Reserve Currency Status Is Being Questioned

Dollar dominance has underpinned global finance since Bretton Woods — roughly 82 years and counting. Historically, reserve currencies don't last forever: the Dutch florin held its position for around 150 years, and British sterling for over a century before gradually ceding ground through the mid-20th century.

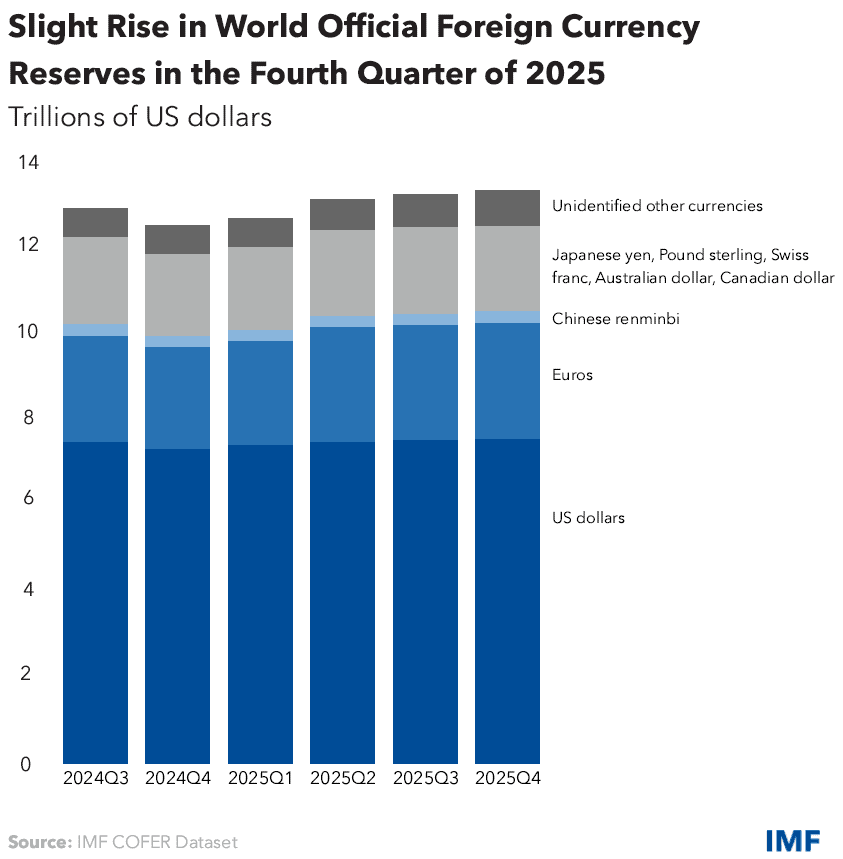

Several dynamics are fueling renewed scrutiny of reserve currency status today, often clustered under the broader banner of de-dollarization:

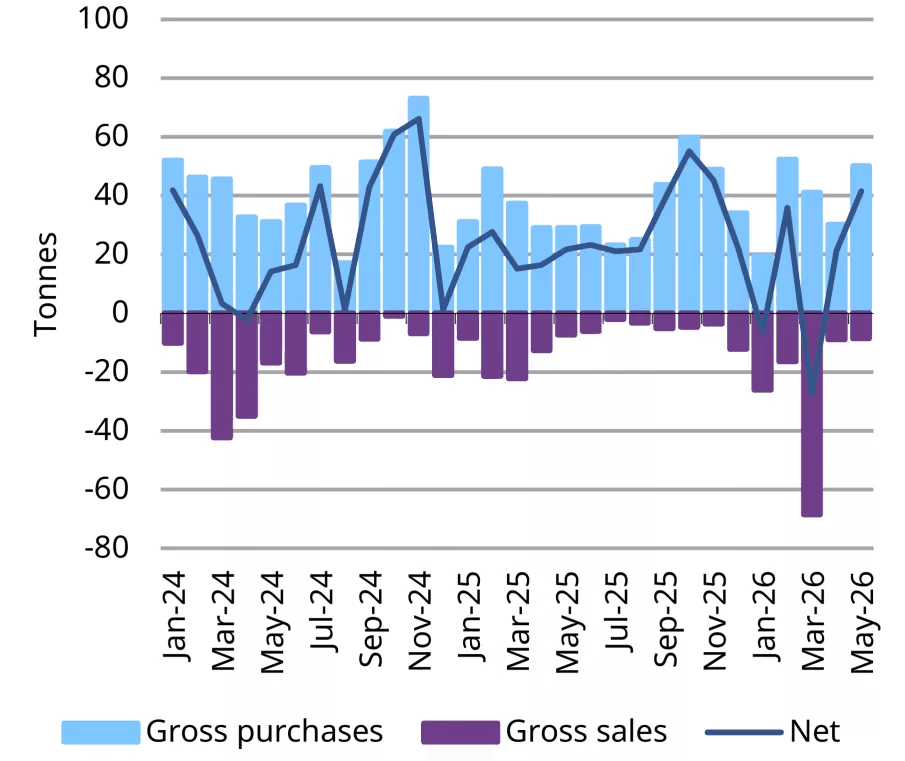

1. Sanctions-driven diversification — Countries are actively building alternative payment infrastructure and increasing gold reserves to reduce reliance on dollar-denominated settlement systems.

2. Fiscal sustainability concerns — Recurring debt ceiling standoffs raise questions about the predictability of US Treasury issuance.

3. Geopolitical fragmentation — A more multipolar world reduces the structural incentives that historically reinforced dollar centrality in trade and reserves.

None of this means transition is imminent. In fact, as we've explored in our analysis of why de-dollarization narratives often precede dollar rallies, periods of peak pessimism toward the dollar have historically coincided with sharp reversals rather than continued declines — a dynamic worth weighing against the consensus narrative. Historically, currency transitions unfold over decades, with long overlap periods where the incumbent remains dominant even as its position visibly erodes. But for advisors, the relevant question isn't when dominance ends — it's whether client portfolios are appropriately diversified against a slow-moving structural risk.

What Reducing Dollar Exposure Actually Means for a Portfolio

Reducing dollar exposure doesn't mean eliminating US assets. It means ensuring that currency risk is a deliberate, sized position — not an unexamined byproduct of home-market bias.

Currency Diversification Across Asset Classes

For most portfolios, international diversification remains one of the most straightforward avenues for reducing correlated dollar risk. Currency diversification can be implemented incrementally across multiple sleeves of a portfolio:

Unhedged international equities, which carry embedded currency exposure alongside their equity risk

Foreign currency-denominated bonds, which isolate currency exposure more directly

Multinational allocations, where revenue diversification provides indirect dollar-exposure dampening

The goal is a measured tilt, not a wholesale reallocation — most advisors implement this gradually, often through incremental rebalancing rather than a single large trade. This shift connects to a broader theme we explored in our analysis of why 2026 could reward global diversification more broadly — currency exposure is just one dimension of a wider case for looking beyond US-concentrated portfolios.

Gold as a Hedge Against Dollar Weakness

Gold has re-emerged as a hedge against dollar weakness for central banks precisely because it carries no counterparty or currency-issuer risk. As we detailed in our piece on gold as the sole anchor in a negative real-rate environment, gold allocations have historically shown low correlation to dollar-denominated financial assets, making it a candidate for a modest strategic allocation rather than a tactical trade.

Managing Treasury Bond Exposure and Debt Ceiling Risk

Recurring debt ceiling standoffs inject episodic volatility into Treasury markets, even when resolved without default. Managing Treasury bond exposure in this environment involves:

Laddering maturities to reduce reinvestment risk around politically sensitive periods

Diversifying sovereign debt exposure beyond US Treasuries where mandates allow

Monitoring short-term bill markets closely, since debt ceiling risk concentrates most visibly at the front end of the curve

Monitoring these dynamics fits within the broader leading-indicator framework we outlined in our guide to recession indicators every portfolio manager should track.

Building a Systematic Approach to Reducing Dollar Exposure

Ad hoc currency hedging is difficult to execute consistently — it requires ongoing monitoring, rebalancing discipline, and a defensible process clients can understand. As we've covered in depth in our piece on rebalancing frequency best practices, threshold-based systematic approaches consistently outperform discretionary, calendar-driven adjustments across market regimes. This is where a systematic portfolio strategy adds real value: predefined rules for rebalancing thresholds, allocation bands, and hedge ratios remove emotion and inconsistency from execution.

A systematic approach also creates an auditable process — critical for advisors who need to explain portfolio decisions to clients and, in some cases, to compliance reviewers.

Common Pitfalls When Reducing Dollar Exposure

Advisors moving in this direction should watch for:

1. Overcorrecting — Shifting too aggressively into non-dollar assets introduces new concentration risk in less liquid or less familiar markets. This concentration concern echoes what we've documented in our analysis of the S&P 500 concentration bubble — uncompensated concentration risk is a problem whether it shows up in currency exposure or equity positioning.

2. Ignoring correlation shifts — Currency and equity correlations aren't static; a hedge that worked historically may not hold under future stress conditions.

3. Underestimating implementation cost — Currency hedges and international rebalancing carry transaction and tax implications that erode returns if not managed carefully.

4. Treating this as a one-time trade — This is an ongoing allocation discipline, not a single rebalancing event.

Conclusion

Reducing dollar exposure is no longer a fringe conversation — it's a legitimate, structural risk-management question that advisors are increasingly expected to address. The goal isn't to predict when the dollar's reserve status changes, but to build portfolios that remain resilient regardless of how that debate resolves. A disciplined, systematic approach — rather than reactive, one-off trades — is what separates a durable strategy from a market-timing bet.

Automating the Strategy with Surmount Wealth

Reading about reducing dollar exposure is one thing. Actually implementing it — consistently, across every client account, without manual rebalancing errors — is another challenge entirely.

This is exactly the kind of thesis Surmount Wealth is built to automate.

With Surmount, you can take a macro view like currency diversification and turn it into a fully systematic, rules-based strategy that runs on autopilot inside your existing brokerage accounts — no fund transfers, no custom code required.

Hypothetical Strategy Concept: “Dollar Diversification Monitor”

This is a hypothetical illustration only, not investment advice or a live Surmount strategy.

To show how this might work in practice, consider a rules-based concept like a Dollar Diversification Monitor:

Tracks a basket of dollar-hedge proxies — gold, international equities, and non-USD sovereign debt exposure

Rebalances automatically when dollar exposure drifts outside a defined target band

Applies predefined thresholds to avoid emotional, reactive trading during periods of currency volatility

Scales consistently across every client account simultaneously, with full auditability for compliance review

This is the kind of strategy that would take hours to monitor and rebalance manually across a full book of clients — but runs continuously and consistently when automated.

Why Advisors Choose Surmount Wealth

Prebuilt strategy library — access professional-grade, rules-based strategies without building from scratch

Custom strategy builder — codify your own thesis, like dollar diversification, into an automated rule set

No asset transfers required — strategies run directly within clients' existing brokerage accounts

Full transparency and control — every rule, threshold, and rebalance is visible and adjustable

If reducing dollar exposure is a conversation you're already having with clients, don't let implementation friction be the bottleneck.

Book a demo today and see how Surmount Wealth can turn your macro thesis into an automated, scalable strategy:

FAQ: Reducing Dollar Exposure

Why reduce dollar exposure now?

Recurring debt ceiling standoffs and shifting reserve currency dynamics have raised structural, not imminent, risk — making this a proactive diversification move rather than a reaction to crisis.

How much dollar exposure should I cut?

There's no universal target — most advisors implement a measured tilt via international equities, foreign bonds, or gold, not a wholesale reallocation away from dollar assets.

Is gold a good dollar hedge?

Yes. Gold carries no currency-issuer risk and has historically shown low correlation to dollar-denominated assets, making it a candidate for a modest strategic allocation.

What is a systematic portfolio strategy?

It's a rules-based approach using predefined rebalancing thresholds and allocation bands, removing emotion and inconsistency from currency diversification decisions.

Does debt ceiling risk affect Treasury bonds?

Yes. Recurring debt ceiling standoffs inject episodic volatility into Treasury markets, particularly at the front end of the curve, even when resolved without default.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.