Blog

The Low Payout Ratio Anomaly in REITs: Mispricing Growth as Risk

In the traditional REIT hierarchy, it’s almost as if the dividend yield is the sun around which all other metrics orbit. For decades, the sector has been marketed as a high-payout bond proxy, leading many generalist investors and income-focused desks to view a sub-40% payout ratio with skepticism—if not outright hostility. The prevailing heuristic suggests that a low yield implies either an inefficient use of capital or a lack of underlying cash flow support.

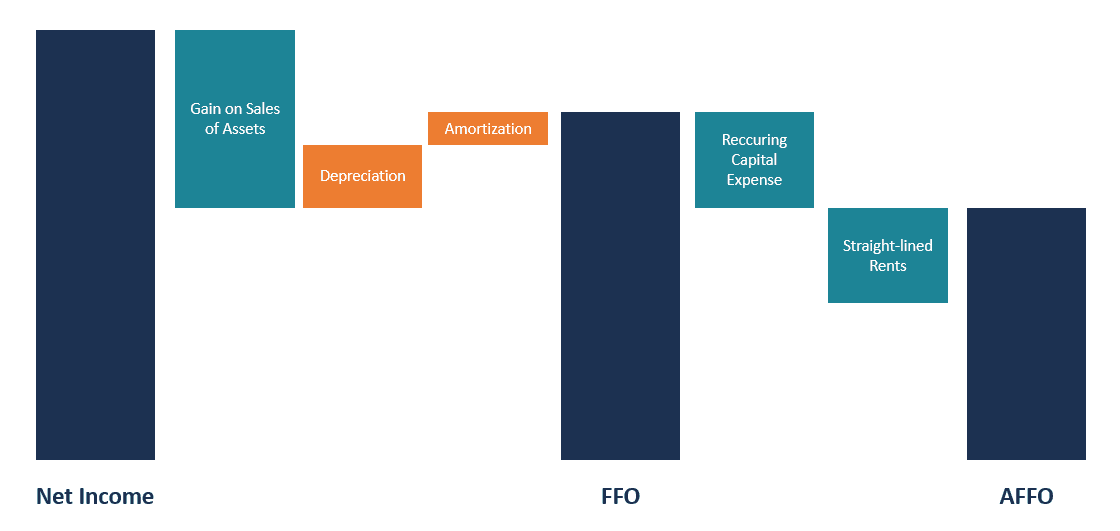

Now while REITs are typically required legally to distribute at least 90% of their taxable income, growth-oriented REITs use non-cash expenses like depreciation to keep their Adjusted Funds From Operations (AFFO) payout ratios low.

Interestingly enough, a closer technical analysis of the modern REIT landscape reveals a persistent "High-Retention Anomaly." By systematically discounting firms that retain a majority of their (AFFO), the market frequently misprices high-velocity growth as idiosyncratic risk. While the broader market chases the immediate gratification of a 7% distribution, it often ignores the superior compounding power of a REIT that can reinvest 60% of its cash flow into internal development or strategic acquisitions at a significant spread to its Weighted Average Cost of Capital (WACC).

For the institutional allocator, this creates a unique alpha opportunity. When a REIT trades at a discount to Net Asset Value (NAV) simply because its payout doesn't meet an arbitrary yield threshold, the market is effectively penalizing the most efficient capital allocators in the space.

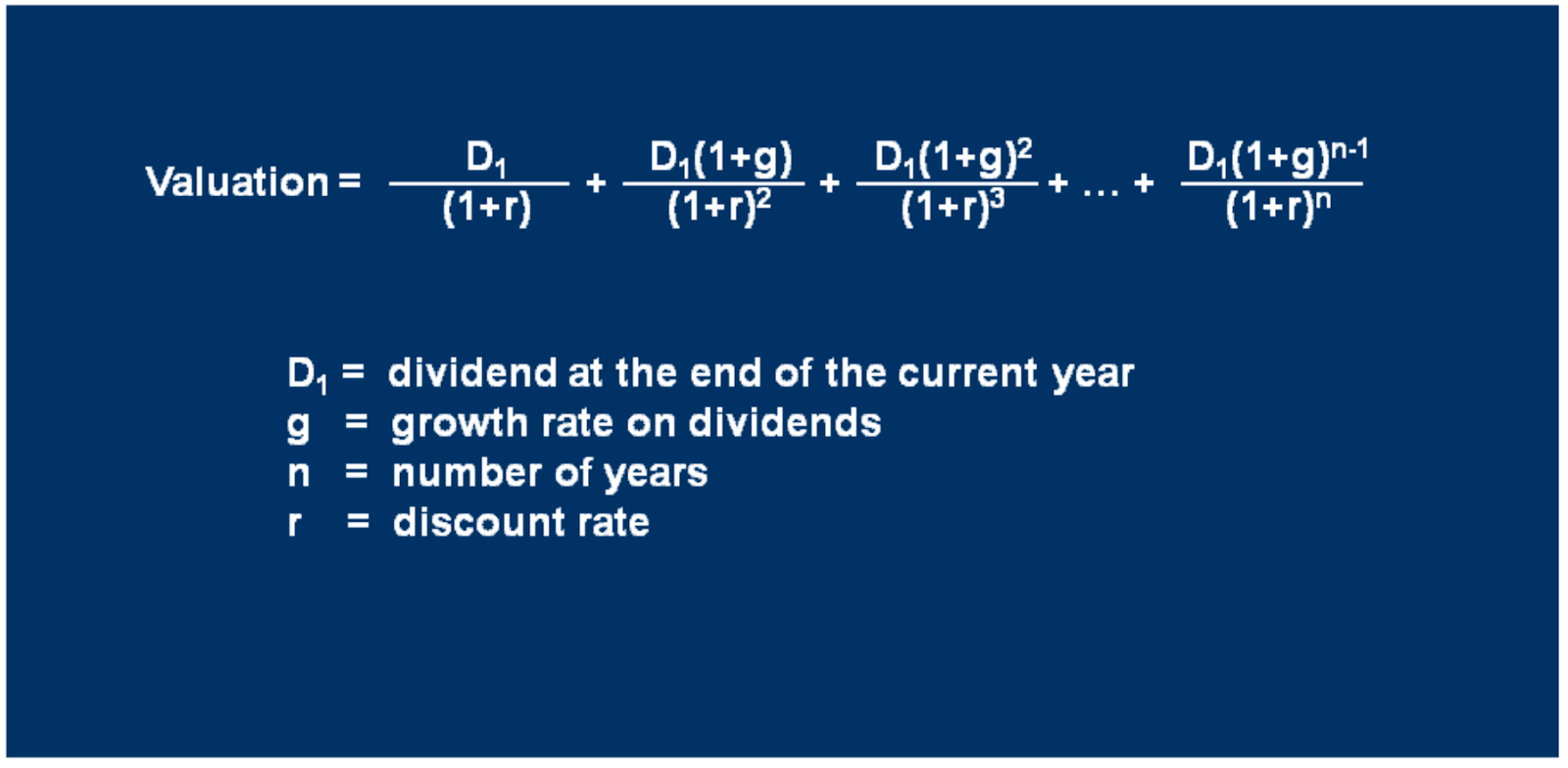

Factor Decomposition: Decoupling Yield from Total Return

In the REIT sector, the market often defaults to a "bond-proxy" valuation model, where the primary driver of the share price is the dividend yield. However, for the sophisticated allocator, total return is a function of the Gordan growth model:

When a REIT maintains a sub-40% payout ratio, it is intentionally suppressing the first variable (Yield) to aggressively optimize the second (Growth). This creates a decoupling effect that generalist screens often miss.

There are three angles through which this anomaly can be best understood:

The Internal Compounding Engine

The core of the anomaly lies in Retained Cash Flow (RCF). While a high-payout REIT must return to the capital markets (equity or debt) to fund every new acquisition or Tier-1 CAPEX project, a low-payout REIT uses "free" internal capital.

Consider the efficiency of a REIT reinvesting at an 8% unlevered NOI cap rate. By retaining 60% of its AFFO, the firm avoids the 3-5% friction of equity issuance costs and the dilutive "treadmill" of constant share count expansion. Over a market cycle, this creates a significant divergence in AFFO per share growth—the metric that truly drives long-term terminal value.

Cost of Capital Advantage

In a volatile interest rate environment, the low-payout ratio acts as a synthetic hedge.

High-payout REITs are essentially "capital takers." They are beholden to the current WACC. If their equity is trading at a discount to NAV, any growth-oriented issuance becomes NAV-dilutive.

On the other hand, Low-Payout REITs are the "capital makers." Their ability to self-fund maintenance CAPEX and a portion of their pipeline allows them to maintain a fortress balance sheet. This lower leverage typically earns them a tighter credit spread, further lowering their cost of debt and widening the Investment Spread (ROIC minus WACC).

The Quality Factor: CAPEX Translucency

There is a common misconception that low payout ratios hide "leaky" businesses with high recurring CAPEX. On the contrary, in sectors like Industrial or Data Centers, low payout ratios often signal a management team that sees an abundance of high-hurdle-rate opportunities.

By decomposing the return, we find that the "Yield" component is often a return of capital, whereas the "Retention" component is a return on capital. For the taxable institutional investor, the latter is significantly more efficient, as it transforms immediate ordinary income into long-term capital appreciation.

Internal Funding as a Competitive Moat

While the market often prices REITs based on their current distribution, the "Low Payout Anomaly" is fundamentally a mispricing of the Cost of Capital. In a normalized or high-interest-rate environment, the ability to self-fund growth becomes a massive structural advantage that is rarely captured in a simple dividend-yield model.

High-payout REITs (those distributing 90%+ of AFFO) retain almost no cash, so any expansion or asset acquisition must be funded through the capital markets. This creates a binary dependency: if the REIT’s share price dips or credit spreads widen, their growth engine stalls.

Conversely, a REIT with a sub-40% payout ratio creates a perpetual internal circularity of capital. By retaining 60% of its cash flow, the firm can fund maintenance CapEx and incremental acquisitions without diluting existing shareholders or increasing leverage.

Internal vs. External Spreads

The technical superiority of the low-payout model is best viewed through the lens of leakage-free compounding. Consider the following comparison:

External Funding (High Payout): To raise $100M for a new development at a 7% Cap Rate, a high-payout REIT must issue equity. Between underwriting fees, legal costs, and the "market discount" often required for a follow-on offering, the "leakage" can be 3% to 5%. The effective yield on that capital is immediately handicapped.

Internal Funding (Low Payout): Reinvesting retained AFFO has 0% issuance cost. A dollar retained and reinvested at that same 7% Cap Rate is 100% accretive from day one. Over a five-year cycle, this lack of friction leads to a significant divergence in NAV per share.

Automating the Quality-Growth Factor

Identifying a persistent market anomaly like the Low Payout Ratio is only half the battle. For the professional investment advisor or portfolio manager, the true challenge lies in execution: systematically filtering the REIT universe, managing rebalancing cycles, and maintaining exposure without increasing operational drag.

This is where Surmount Wealth transforms institutional-grade research into live, tradeable portfolios.

Institutional Execution, Automated

Whether you are looking to exploit the mispricing of high-retention REITs or deploy a multi-factor risk-managed framework, Surmount provides the infrastructure to automate your specific investment DNA.

Custom Strategy Engineering: Move beyond rigid, off-the-shelf products. Our team can help you build and backtest a proprietary strategy that specifically targets the payout-ratio anomaly—integrating your own fundamental overlays and risk parameters.

Plug-and-Play Precision: Access our library of pre-built automated strategies, designed for modern market regimes. From EMA-based trend following to sophisticated capital recycling models, these are ready for immediate deployment across your client accounts.

Seamless Integration: We don't just provide the logic; we provide the rails. Seamlessly deploy and manage automated strategies across your existing custodial architecture, ensuring your thesis is executed with 100% fidelity, 24/7.

Stop Managing Spreadsheets. Start Managing Alpha.

The "Low Payout Anomaly" is a structural edge waiting to be captured. Don't let manual execution or operational friction dilute your returns.

[Book a Demo with the Surmount Wealth Team]

Join the elite cohort of managers using automated infrastructure to scale their highest-conviction ideas.