Blog

30-Year Treasury Yield 2026: What the Long End Is Signaling

Most rate conversations fixate on the Fed funds rate or the 2-year Treasury. But for serious allocators, the 30-year treasury yield 2026 environment may be the most important signal in the room. Long-duration yields don't move on Fed rhetoric alone — they reflect the market's collective judgment on growth, inflation, fiscal sustainability, and risk appetite over decades. When the long end moves decisively, portfolios need to respond accordingly.

The 30-year recently flirted with 5.2% — a level last seen in June 2007, just before the subprime crisis unraveled into the worst economic contraction since the Great Depression. That precedent alone warrants serious professional attention.

30-Year Treasury Historical Levels — How Today Compares

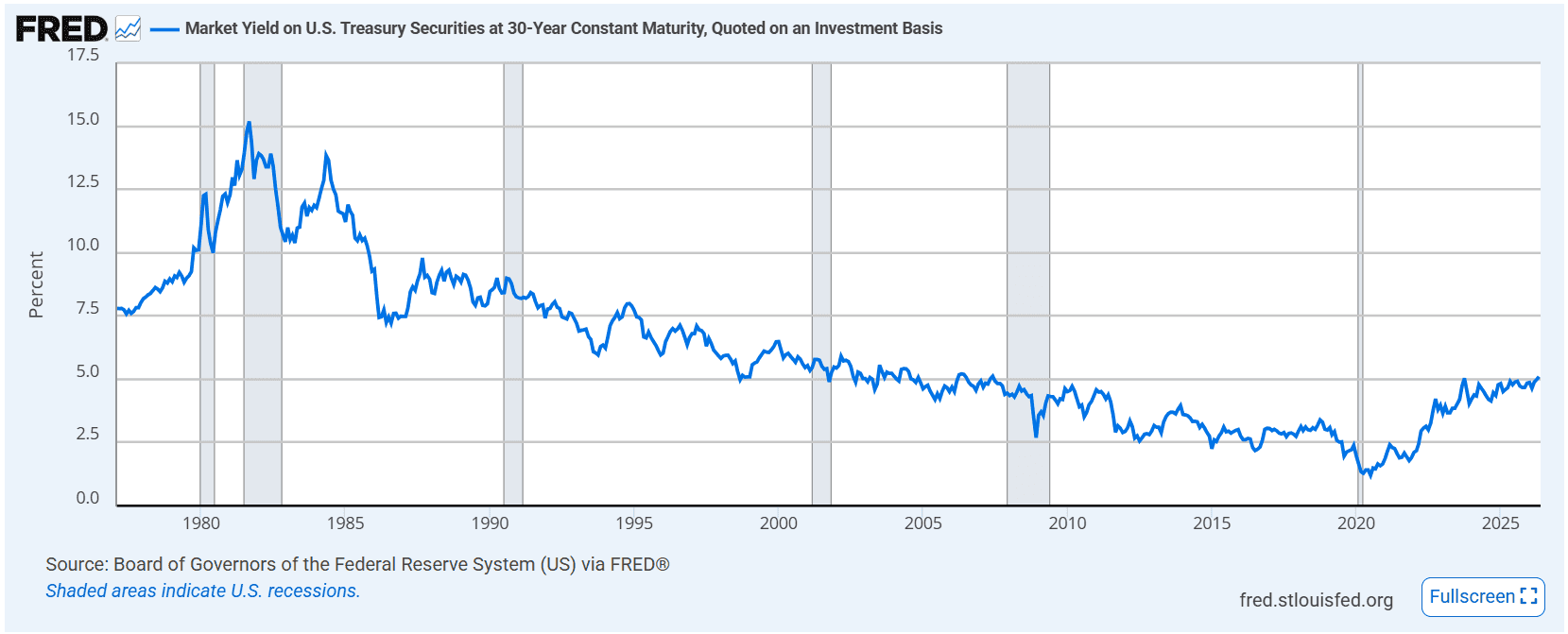

To appreciate the current treasury yield curve 2026 dynamic, context matters. The 30-year yield averaged above 8% through much of the 1980s and 1990s before a four-decade secular decline brought it to historic lows near 1.2% in 2020. The reversal since then has been sharp and structurally significant.

At 5%+, we are not in anomalous territory by the standards of financial history. But we are in a fundamentally different regime than the one that shaped most modern portfolio construction frameworks — frameworks built during an era of structurally declining long-term treasury yield outlook assumptions. Those frameworks are now being stress-tested in real time.

The Long Bond as a Macro Barometer

The long bond encodes what markets believe about the future. A rising long bond yield recession signal is nuanced — it can reflect either growth optimism driving up real rates, or inflation and fiscal fear driving up the nominal vs real yield analysis spread. Right now, evidence points to both simultaneously, which is precisely what makes this environment difficult to navigate with conventional heuristics.

Energy price shocks feeding into CPI expectations, a federal deficit showing no credible path to consolidation, and a global de-risking of U.S. Treasuries by foreign holders are all contributing. The long end is not screaming one message — it is whispering several uncomfortable ones at once.

Unpacking the Signal — What's Actually Driving Yields Higher

The move in long-end rates is not monolithic. Decomposing it matters.

Term Premium Is Back — And What That Means for Allocators

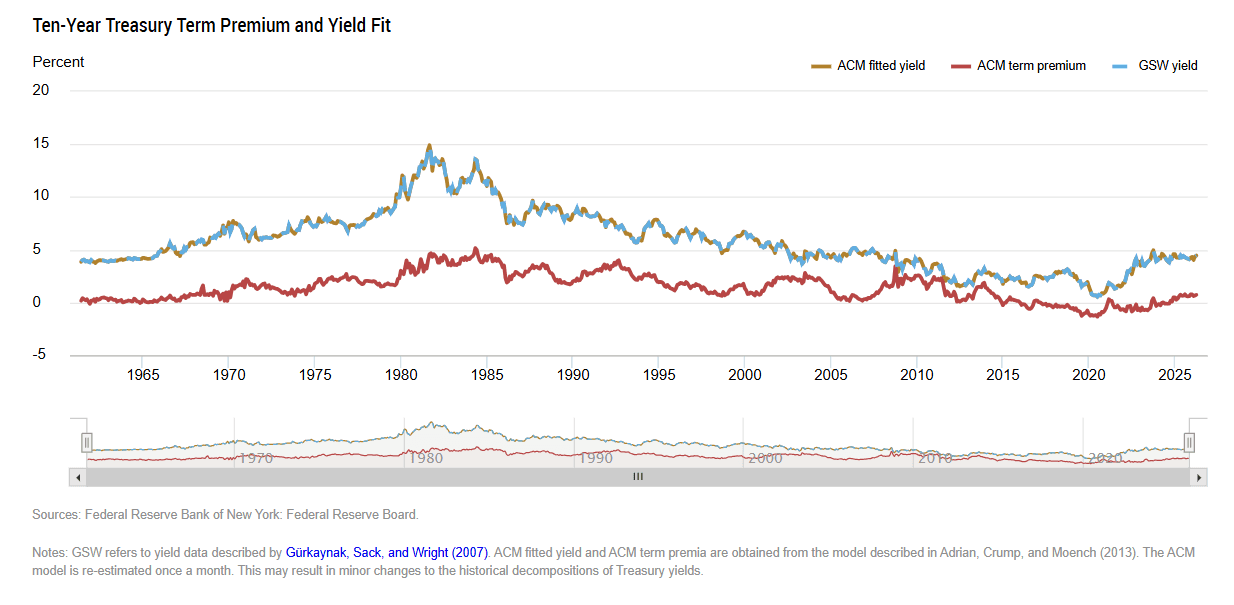

For over a decade following the Global Financial Crisis, the term premium treasury bonds component was effectively zero or negative — compressed by quantitative easing and global safe-haven demand. Investors were paid nothing extra to accept the duration risk of holding a 30-year bond over rolling short-term paper.

That has changed. Term premium has re-emerged as a meaningful contributor to long-end yields, reflecting genuine uncertainty about fiscal trajectories, inflation persistence, and the reliability of Treasuries as a volatility hedge.

A proper nominal vs real yield analysis of the current 30-year yield suggests that real yields — yields above expected inflation — are elevated, not just nominal ones. This makes duration exposure genuinely costly in a way it was not for most of the past decade.

Portfolio Implications of a Sustained High-Rate Long End

Elevated long-end yields reprice nearly every asset class through the discount rate mechanism. In equity valuation models, the discount rate equity prices relationship is direct: higher long-duration risk-free rates compress the present value of future cash flows, particularly for long-duration growth equities whose earnings are weighted heavily toward the future.

We explored this dynamic in depth in our analysis of equity risk premium in 2026.

Duration risk portfolio management becomes central. Portfolios that loaded up on long-dated bonds or high-multiple equities during the zero-rate era now carry embedded losses that can crystallize quickly if yields push higher still. Meanwhile, fixed income strategy rising yields thinking has shifted — shorter duration, inflation-linked instruments, and floating rate exposure have displaced the traditional long-bond allocation in many institutional frameworks.

Equity valuation rising interest rates pressure is most acute in sectors where growth is priced far into the future. The concentration of U.S. equity market cap in AI and technology names — many of which command elevated multiples — makes the aggregate index more rate-sensitive than headline earnings growth figures suggest.

Rethinking Asset Allocation in a High Rate Environment

The classic 60/40 portfolio was built on a negative stock-bond correlation that held reliably for two decades. That correlation has become unreliable. And as we argued in Gold as the Sole Anchor, the search for genuine portfolio diversifiers in this environment points away from traditional fixed income entirely

In the current asset allocation high rate environment, bonds no longer consistently cushion equity drawdowns — they can move in the same direction, as 2022 demonstrated painfully.

Factor investing high rate environment research consistently shows that value, quality, and low-duration factors tend to outperform in sustained rising-rate regimes. Momentum strategies require recalibration as sector leadership rotates away from the long-duration growth names that dominated the prior cycle. A rules-based, systematic approach to factor exposure offers more disciplined navigation than discretionary reallocation during volatile rate transitions.

What Should Portfolio Managers Do Now?

The 30-year treasury yield 2026 level presents two primary scenarios. In the first, yields stabilize as inflation moderates and fiscal concerns plateau — allowing equities to re-rate modestly higher and duration to recover. In the second, yields continue climbing toward 5.5% or beyond, driven by persistent inflation, foreign Treasury selling, or a sovereign credit concern — triggering a meaningful equity de-rating and credit spread widening.

Portfolio rebalancing strategy 2026 must account for both scenarios rather than betting on one. This means stress-testing factor exposures, reducing uncompensated duration, and systematically hedging tail risk rather than relying on discretionary judgment during fast-moving markets. Algorithmic portfolio strategy interest rates frameworks — particularly those that can dynamically adjust allocation weights based on yield curve signals — offer structural advantages here. Automated investing rising rate environment tools allow for faster, emotion-free execution of pre-defined reallocation rules. Systematic investing macroeconomic risk management, anchored in quantitative signals rather than narrative, is precisely the discipline this environment rewards.

Conclusion — Navigating Uncharted Rate Territory

The 30-year treasury yield 2026 move above 5% is not noise. It reflects a genuine regime shift — the end of the four-decade bond bull market, the re-emergence of term premium, and a fundamental repricing of duration risk across asset classes. For professional allocators, the question is not whether this matters. It is whether your portfolio construction framework was built for it.

Markets can remain dislocated from economic fundamentals longer than intuition suggests. But the long end of the curve has a way of eventually reasserting gravity. The allocators best positioned will be those who act on the signal systematically, not reactively.

Automate Your Rate Thesis With Surmount Wealth

Understanding the macro signal is one thing. Acting on it — consistently, systematically, and without emotional interference — is another challenge entirely.

Surmount Wealth is an AI-driven investment platform built for exactly this kind of environment. It allows self-directed investors and professional allocators to build, backtest, and fully automate sophisticated investment strategies directly on top of their existing brokerage accounts — no fund transfers, no coding required.

Consider a hypothetical strategy we might call the "Long End Rotation Model" (illustrative concept only — not a live strategy or investment advice): a rules-based allocation framework that monitors the 30-year treasury yield as a primary signal, systematically rotating out of long-duration growth equities and into short-duration value, energy, and floating-rate credit when the 30-year breaches predefined thresholds — and reversing the rotation when yields stabilize. Rebalancing triggers are automated. Execution is instant. Emotion is eliminated entirely.

This is exactly the kind of thesis-driven, macro-aware strategy that Surmount Wealth's platform is designed to bring to life. Whether you are working from a rate outlook, a factor model, a sector rotation thesis, or a tail-risk hedge — you can build it, test it against historical data, and automate it in minutes.

Stop letting your best macro insights sit idle in a research note.

Book a Demo with Surmount Wealth Today →

FAQ: 30-Year Treasury Yield 2026

Why is the 30-year treasury yield rising in 2026?

A combination of persistent inflation, re-emerging term premium, and growing fiscal deficit concerns are pushing the 30-year treasury yield 2026 higher. Foreign Treasury selling is adding additional upward pressure.

How do rising treasury yields affect my portfolio?

Rising yields increase the discount rate applied to future earnings, directly suppressing equity valuations — particularly long-duration growth stocks. Duration risk portfolio management becomes critical in this environment.

What does the long bond yield signal for recession?

A sustained long bond yield recession signal at 5%+ historically precedes periods of significant economic stress. However, today's move reflects both inflation fear and term premium, not growth collapse alone.

When should allocators rebalance for rising rates?

Rules-based, systematic rebalancing triggered by yield threshold breaches outperforms discretionary timing in rising-rate regimes. A portfolio rebalancing strategy in 2026 should be pre-defined, not reactive.

What asset allocation works in a high-rate environment?

Research consistently favors short-duration, value, and quality factors in a high-rate environment. Revisiting traditional 60/40 frameworks and incorporating factor investing strategies is strongly advisable right now.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.