Blog

Understanding RMDs in 2026: A Practical Guide for Advisors

Required Minimum Distributions (RMDs) aren't what they used to be. In the past, the rules were relatively static: you hit age 70½, you started taking money out, and you paid your taxes. Simple.

But between the original SECURE Act and the sweeping changes of SECURE 2.0, the RMD landscape has been completely rewritten. For an advisor in 2026, staying "current" means navigating a maze of shifting age brackets, eliminated requirements for Roth workplace accounts, and reduced (but still stinging) penalties.

In today's dynamic environment, with a growing retiree population, RMD planning almost resembles a high-stakes chess match with the IRS. To keep your clients' retirement on track, here is the 2026 briefing every advisor needs.

What Are RMDs?

An RMD is basically the federal government’s way of ensuring they eventually collect the deferred tax revenue on retirement savings. While assets in traditional retirement accounts grow tax-free for decades, the IRS mandates that owners begin withdrawing a specific minimum amount each year once they reach a certain age.

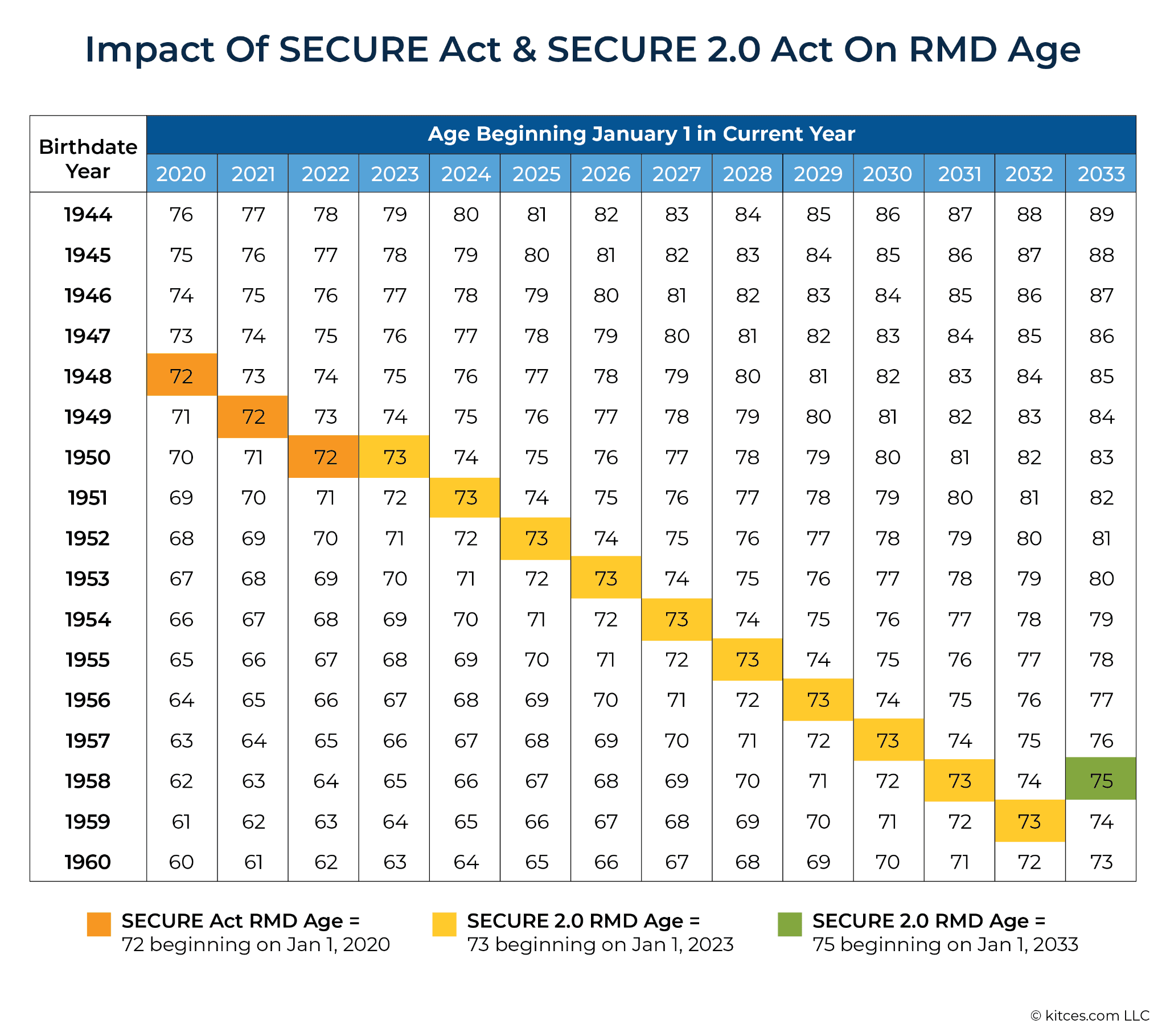

The 2026 Age Framework

As of 2026, the "RMD Age" depends entirely on the client's birth year. SECURE 2.0 pushed these dates further out to allow for more growth:

Born 1951–1959: The RMD age is 73. (Many of your clients reach this milestone this year).

Born 1960 or later: The RMD age is 75

This change provides a wider window for tax-planning strategies, such as partial Roth conversions, but it also increases the size of future RMDs as account balances have more time to compound.

The Roth Revolution: 401(k) and 403(b) Parity

Perhaps the most significant change for 2026 is the full implementation of the Roth RMD exemption. Historically, one of the biggest headaches for advisors was explaining why Roth IRAs had no RMDs, but Roth 401(k)s did.

As of 2024 and continuing into 2026, pre-death RMDs are eliminated for all Roth designated accounts in employer plans. Your clients no longer need to execute "defensive" rollovers from a 401(k) to an IRA just to avoid a mandatory distribution on their tax-free assets.

The implications of this change are profound: clients can now leave assets in high-quality institutional plans longer, simplifying their estate planning and preserving the tax-free wrapper without the friction of a rollover.

For advisors, this means strategic precision.

With the penalty for a missed RMD now reduced from 50% to 25% (and potentially as low as 10% if corrected within two years), the "cost of error" has decreased, but the complexity of planning has increased. Beyond just the "when" and "how much," advisors must now consider:

The 10-Year Rule for Heirs: For non-spouse beneficiaries, the ambiguity around annual RMDs within the 10-year window has been clarified. If the decedent had already reached their Required Beginning Date (RBD), the beneficiary must generally take annual distributions in years 1–9.

QCDs as the Ultimate Hedge: The Qualified Charitable Distribution (QCD) limit is now indexed for inflation, allowing clients 70½ or older to offload up to $111,000 (for 2026) directly to charity—counting toward their RMD without touching their AGI.

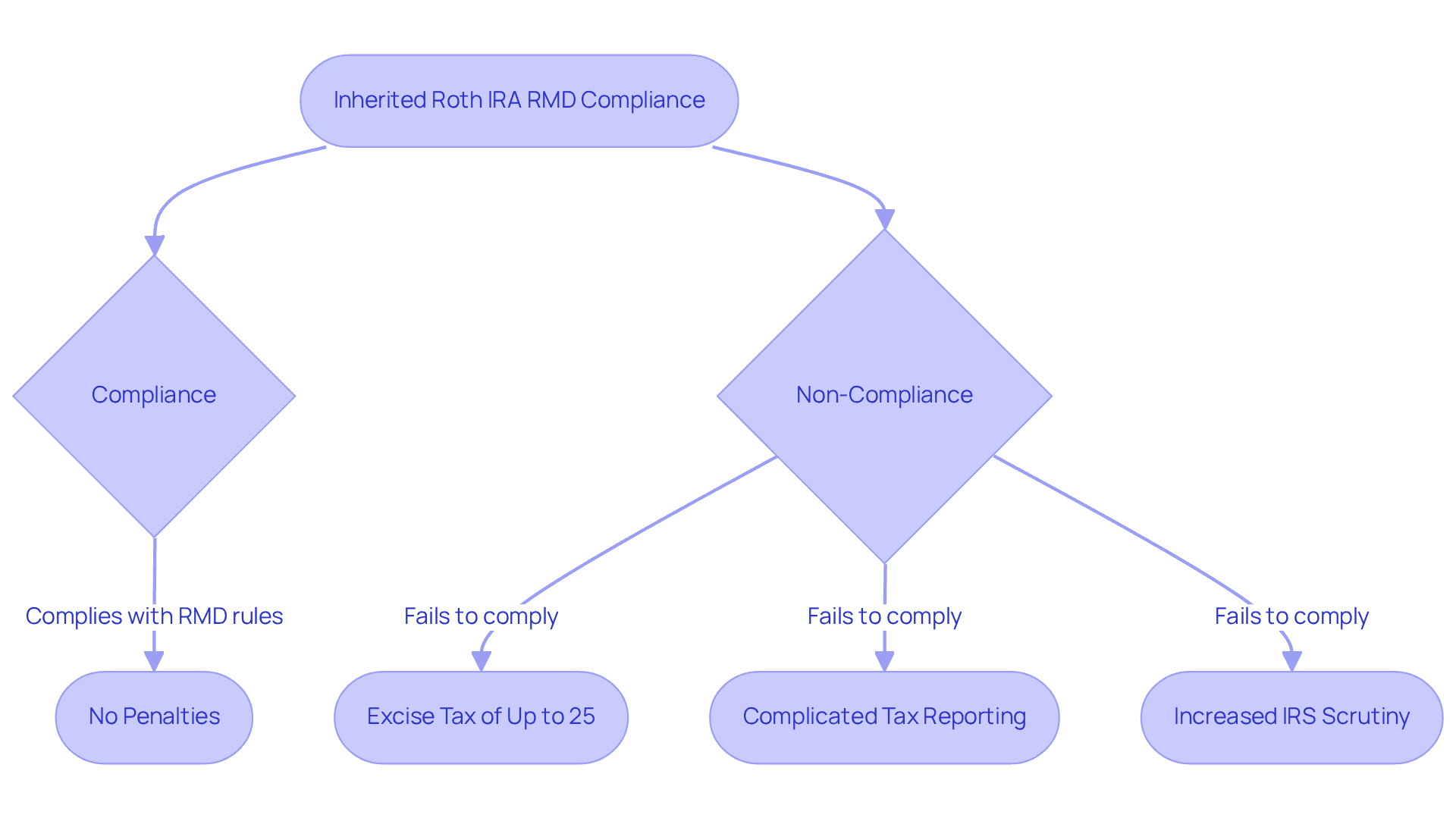

Penalties: Lower Stakes, Higher Oversight

The IRS has softened the blow for mistakes, but the oversight is tighter. The penalty for failing to take an RMD has been slashed from 50% to 25%.

Furthermore, if the error is corrected within a "correction window" (generally two years), that penalty can be further reduced to 10%. While this is a welcome relief, the complexity of modern RMDs means the likelihood of an oversight is higher—making your role as a "gatekeeper" more valuable than ever.

Specific risks to watch out for include:

The Oversight Ripple Effect:

Missing an RMD often triggers a chain reaction. By the time a client realizes they missed a 2024 RMD in 2026, they may have already under-withdrawn for multiple years. Even a "low" 10% penalty becomes expensive when compounded across several accounts.

The Invisibility of Errors:

With the RMD age moving to 73 (and eventually 75), and the exclusion of Roth 401(k)s, many clients lose track of which "bucket" is due and when. Automated systems at large custodians often struggle with these "transition years," leaving the human advisor as the only reliable line of defense.

The Opportunity Cost of Correction:

To qualify for the 10% reduction, the client must act quickly. If they wait for an IRS notice, the discount is off the table. As their advisor, your value lies in discovery—finding the error during an annual review before the IRS finds it for them.

Practical Approaches for Advisors and Clients

When RMDs kick in, they can feel like a forced liquidation of a client's hard-earned strategy. As an advisor, your goal isn't just to "find the cash"—it's to ensure the RMD doesn't disrupt the portfolio’s long-term growth or create unnecessary tax drag.

Many clients reflexively reach for high-yield bonds or "junk" funds to cover RMDs. This is often a mistake. High-yield assets usually lack growth and can be highly sensitive to interest rate spikes. Shifting to dividend aristocrats can be far more useful in this case. This is because, over time, the "Yield on Cost" (the dividend relative to the initial investment) often surpasses static high-yield plays.

As such, growing dividends provide a naturally expanding "cash bucket" that can satisfy a larger portion of the RMD each year without requiring you to sell shares of the underlying stock.

Similarly, clients stand to benefit when holding their lower-growth, income-heavy assets (Bonds, REITs) in their IRA. Since these are the assets being forced out by the RMD anyway, they would essentially be "cleaning out" the slower-growing parts of the portfolio.

Alternatively, they could hold their aggressive growth assets (Tech, Small Cap) in their Roth/Taxable accounts. Since Roths have no RMDs, it would be wise to have the "fastest horses" in the tax-free stable to grow unchecked for as long as possible.

Finally, for clients who don't need the RMD income for living expenses, a Qualified Longevity Annuity Contract (QLAC) may be the smartest way to go. Through this, clients can use up to $210,000 (indexed for 2026) from their IRA to purchase a QLAC. The amount used to buy the QLAC is removed from the total IRA balance used to calculate RMDs. This can significantly lower the annual RMD obligation until age 85, keeping the client in a lower tax bracket during their 70s.

For portfolio managers, amid this complex planning environment, having an automated investment strategy that maximizes fund returns ensures that every decision—from dividend reinvestment to asset reallocation—is executed efficiently and consistently. It allows managers to dynamically capture opportunities in high-yield or growth assets, maintain optimal portfolio exposure, and meet liquidity requirements like RMDs without sacrificing long-term performance. By removing emotional bias and enforcing disciplined, rules-based actions, automation helps portfolios stay on track to achieve superior risk-adjusted returns even during volatile markets.

Book a demo now with Surmount to see how automated strategies can optimize your portfolios, and help you capture maximum returns with minimal manual intervention.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.