Blog

Fixing a Tech Overconcentration Portfolio

When markets sell off sharply in a single sector and only that sector, the problem is rarely the market. It is the portfolio. Tech overconcentration portfolio risk is one of the most persistent and underappreciated structural vulnerabilities in professionally managed accounts today — not because advisors are unaware of diversification, but because modern index construction has quietly done the concentrating for them.

This post breaks down why tech stock overexposure is so common, what equity sector diversification actually requires in practice, and how systematic portfolio risk management can fix concentration before volatility forces the issue.

What Is Tech Stock Overexposure — and Why It's So Common

Tech stock overexposure occurs when a disproportionate share of a portfolio's risk and return is driven by the performance of the technology sector, regardless of how many individual names are held. A client owning 25 different semiconductor and software stocks is not diversified. They are concentrated in a single factor with 25 data points.

The uncomfortable reality is that this condition is almost automatic for any advisor using standard benchmarks or index products without active sector management.

How Index Funds Mask Index Fund Concentration

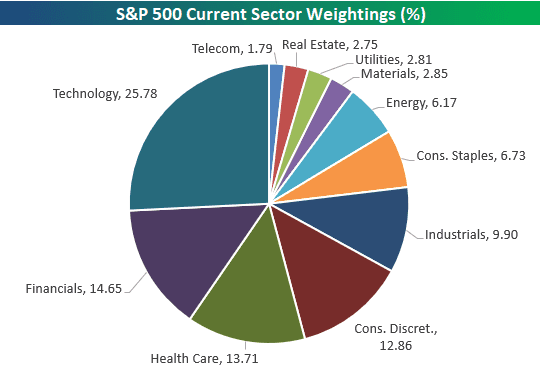

Index fund concentration has become a structural feature of mainstream portfolio construction, not a bug. The S&P 500 — historically considered the gold standard of diversified U.S. equity exposure — now carries a technology weighting approaching 40% when including adjacent mega-cap names. The Nasdaq-100 (QQQ), often used for growth exposure, is even more extreme.

The consequence is that a client holding a blended portfolio of diversified index funds may believe they are broadly exposed to the U.S. economy while actually running a de facto technology sector tilt. When technology underperforms — even briefly — the concentrated drawdown feels inconsistent with what the client was told they owned.

This phenomenon is well-documented in the context of passive index design and market-cap weighting mechanics. For a deeper look at how passive flows amplify these dynamics, our analysis of the S&P 500 concentration bubble outlines the structural mechanisms driving this risk.

The Illusion of Diversification Across 20 Tech Stocks

Holding 20 to 25 technology or semiconductor positions does not reduce sector concentration risk in any meaningful way. If the underlying names share the same macro drivers — AI capex cycles, interest rate sensitivity, earnings multiple compression — they will move together in stress environments regardless of how many tickers are on the screen.

True diversification requires exposure to assets whose return drivers are structurally different. Owning Nvidia, AMD, and a basket of AI infrastructure plays alongside three cloud software names is not diversification. It is a leveraged bet on a single economic theme.

Why Equity Sector Diversification Is a Portfolio Risk Management Imperative

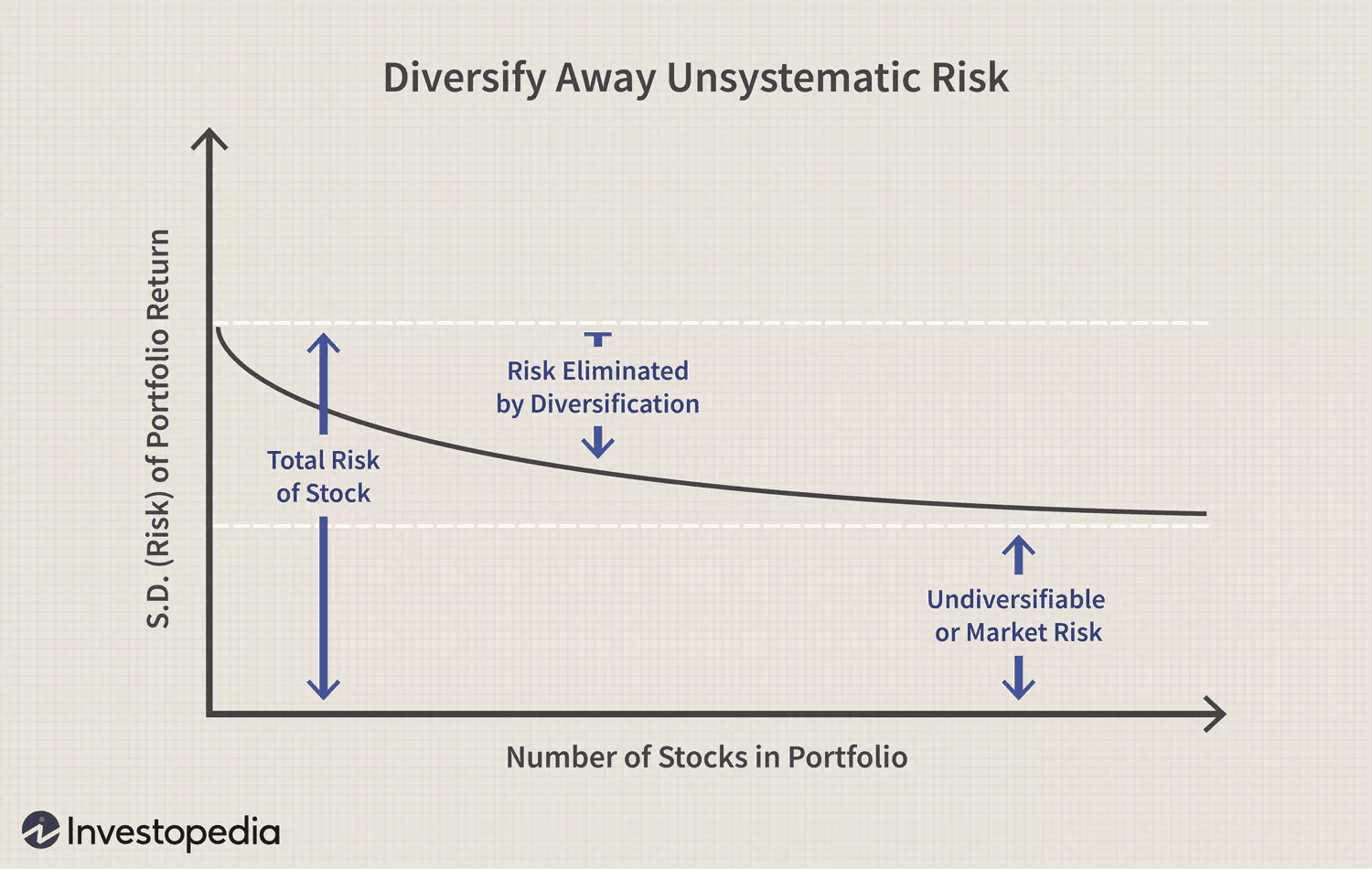

Equity sector diversification is not simply about smoothing returns. It is a portfolio risk management requirement for any advisor operating under a fiduciary standard. Concentrated sector exposure leaves clients structurally overexposed to a single set of macro variables, which violates the principle of risk-appropriate allocation regardless of what the holdings look like on paper.

On days when technology sells off materially, genuinely diversified portfolios demonstrate their value. REITs, healthcare, consumer staples, financials, and energy often hold or advance precisely when high-multiple growth sectors correct. That non-correlation is the point.

What Sector Rotation Strategy Actually Looks Like in Practice

A sector rotation strategy in a professional context is not market timing. It is the systematic alignment of sector weights with underlying economic conditions, valuation signals, and rate environments — and then maintaining that alignment as conditions shift.

In practice, this means:

Mapping portfolio sector weights against benchmark and target allocations on a regular cadence

Identifying where drift has created unintended concentration — particularly in growth and technology sectors after extended bull runs

Systematically rotating into underweighted sectors based on defined signals, not reactive headlines

Documenting the rotation rationale to support fiduciary compliance

The behavioral obstacles that prevent advisors from executing this rotation effectively are substantial.

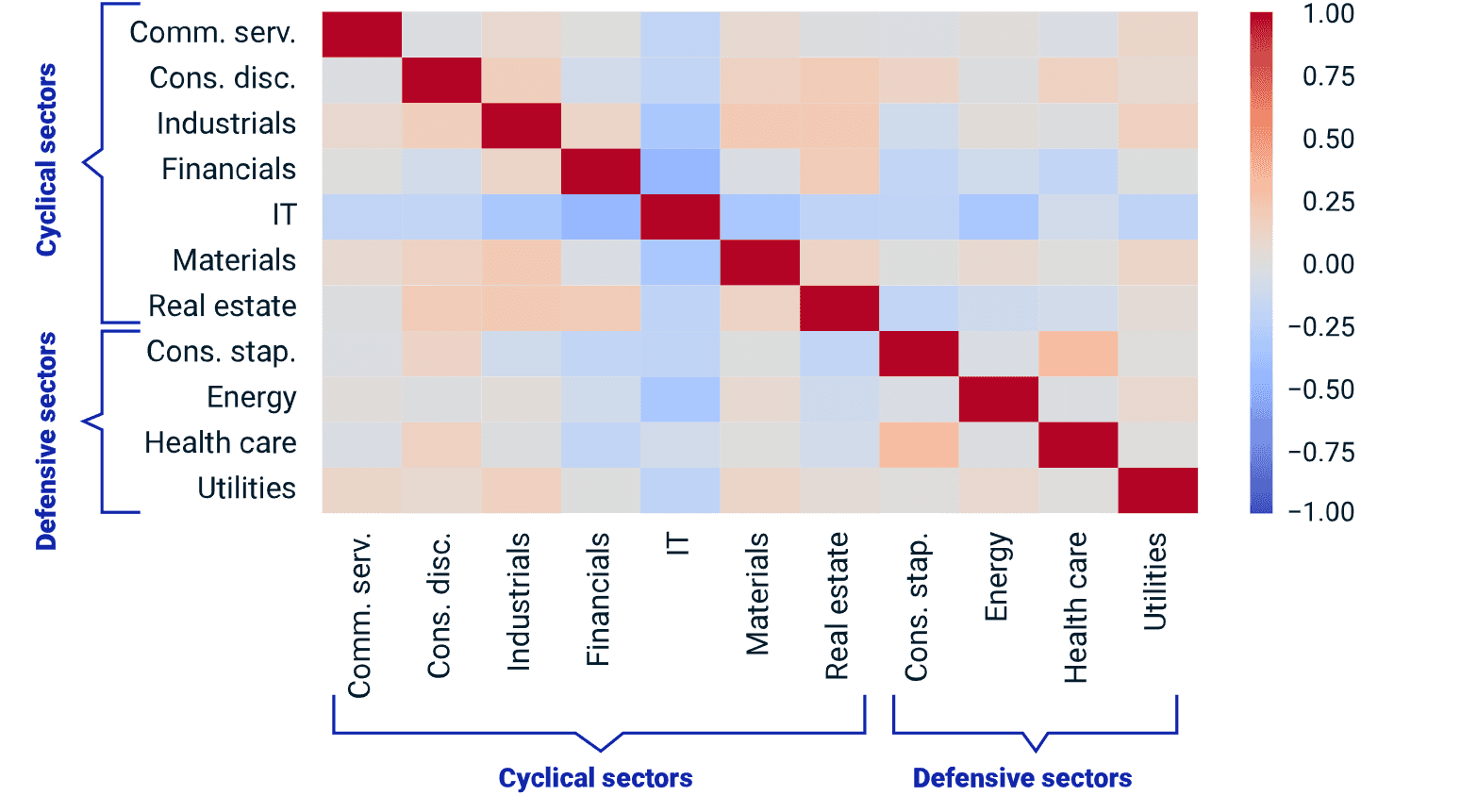

Which Sectors Provide Real Non-Correlated Exposure

Not all diversification is equal. The sectors most likely to provide genuine non-correlation with technology in a risk-off or rate-sensitive environment include:

Healthcare: Driven by demographic demand, pricing power, and regulatory cycles — largely independent of AI capex sentiment

Consumer Staples: Defensive earnings streams with pricing power that hold value in inflationary or recessionary environments

Energy: Commodity-driven return profile with low correlation to growth equity factors

REITs: Income-oriented, rate-sensitive, and structurally distinct from growth equities — though correlation may increase in high-rate regimes

Financials: Benefit from steepening yield curves and credit cycle expansion — often inversely correlated to tech in valuation compression environments

The allocation weightings that achieve genuine risk reduction will vary by client objective, time horizon, and existing exposure. The point is that these sectors provide return drivers that technology cannot replicate.

How to Rebalance Without Abandoning Your Tech Thesis

Reducing a tech overconcentration portfolio does not require exiting technology entirely. Most advisors have clients with meaningful embedded gains in tech positions and a legitimate long-term thesis on AI infrastructure, semiconductor cycles, or software compounding. Sector diversification is about risk management within a thesis, not abandonment of it.

The practical framework involves three steps:

Quantify the concentration: Measure the actual sector weight of every position including index funds. Many advisors are surprised by the true technology exposure once indirect holdings are included.

Define target allocations: Set explicit sector weight ranges aligned with the client's risk profile and investment policy statement. These targets should be documented and defensible.

Build systematic rebalancing triggers: Rather than making discretionary adjustments, define the conditions under which the portfolio will rotate — drift thresholds, valuation signals, or calendar-based reviews.

For a comprehensive framework on rebalancing frequency and threshold design, see our post on portfolio rebalancing best practices — particularly the section on how automation removes execution lag from the rebalancing process.

Automated Portfolio Rebalancing as a Systematic Solution

Manual rebalancing at scale is operationally difficult and behaviorally unreliable. Advisors managing 100+ client accounts cannot realistically monitor sector drift across every portfolio in real time. The result is that concentration builds undetected until a correction makes it visible.

Automated portfolio rebalancing addresses this by encoding the rebalancing logic into a rules-based system that monitors portfolios continuously, flags drift against defined targets, and executes trades when thresholds are breached — without requiring discretionary intervention at each step.

This is not a passive set-it-and-forget-it approach. The rules require thoughtful construction. But once built, they remove the execution inconsistency and emotional override that cause most discretionary rebalancing frameworks to fail in practice.

For context on why this consistency matters for both performance and compliance, our piece on portfolio diversification strategies outlines the structural case for maintaining allocation discipline through full market cycles.

Conclusion

A tech overconcentration portfolio is not a reflection of poor judgment. It is a reflection of how modern index construction, passive inflows, and a multi-year technology bull market have quietly shifted exposure for advisors and clients who were not actively managing sector weights. The correction does not require dramatic portfolio surgery. It requires a systematic framework for measuring concentration, defining targets, and automating the rebalancing process that enforces those targets regardless of market noise.

Advisors who build that infrastructure now are not abandoning their technology thesis. They are protecting their clients from the volatility that any concentrated sector will eventually deliver.

Automate Your Sector Diversification Thesis With Surmount Wealth

Understanding the mechanics of tech overconcentration portfolio risk is the analytical step. Acting on it — systematically, consistently, across every client account without execution lag or behavioral override — is the operational challenge most advisors have not solved.

That is exactly what Surmount Wealth is built for. Surmount is an AI-driven automated investing platform that lets portfolio managers and RIAs build, backtest, and deploy fully rules-based trade strategies directly on existing brokerage accounts. No fund transfers. No coding required.

Hypothetical Strategy Illustration: The Sector Balance Monitor

The following is a hypothetical strategy concept for illustrative purposes only. It does not represent an existing Surmount product and is not investment advice.

Imagine a rules-based strategy — call it the Sector Balance Monitor — designed to systematically address the dynamics discussed in this post:

Concentration trigger: When the technology sector weight in a portfolio breaches a defined ceiling (e.g., 40%), the strategy flags a rebalancing event and begins rotating capital into underweight sectors based on pre-set priority rules

Volatility signal: When 30-day realized volatility in the technology sector exceeds a defined threshold, the model accelerates defensive rotation into healthcare, consumer staples, and short-duration income exposures

Drift monitoring: The strategy continuously tracks sector weights against target allocations, executing trim-and-rotate sequences when any sector drifts beyond the defined tolerance band

Re-entry logic: As technology valuations normalize or volatility compresses, the model systematically rebuilds tech exposure back toward target weight — ensuring the client remains invested in the thesis without carrying excess concentration risk

Why Leading Advisors Are Choosing Surmount:

Automate any thesis: Turn sector allocation targets and rebalancing signals into live, rules-based strategies without writing a single line of code

Prebuilt strategy library: Deploy proven institutional frameworks across client accounts immediately

Full customization: You define the logic, the thresholds, and the sector targets — Surmount handles execution 24/7

Broker-agnostic: Connects seamlessly to existing accounts including Interactive Brokers and Alpaca

No fund transfers required: Strategies run directly on your existing brokerage infrastructure

Scalable across your entire book: One strategy, every client, executed simultaneously without manual intervention

Don't let your best research sit in a risk report. Turn it into a live, automated strategy.

Book a Demo with Surmount Wealth →

FAQ: Tech Overconcentration Portfolio

What is a tech overconcentration portfolio?

It is a portfolio where technology-sector exposure — including indirect holdings through index funds — drives the majority of risk and return, regardless of how many individual positions are held.

How does index fund concentration happen?

Market-cap weighting causes index funds to allocate heavily to large-cap technology names. As tech valuations rise, their share of the index grows automatically, increasing portfolio concentration without any active decision by the advisor.

What sectors reduce tech stock overexposure?

Healthcare, consumer staples, energy, REITs, and financials provide return drivers that are structurally distinct from technology. They tend to hold value or advance during periods of growth-sector correction.

How often should sector rebalancing occur?

Rules-based rebalancing triggered by defined drift thresholds consistently outperforms calendar-only approaches. Automated portfolio rebalancing removes the execution lag and behavioral bias that undermine discretionary schedules.

Can I diversify without selling my tech positions?

Yes. Sector diversification strategy can be implemented by deploying new capital into underweight sectors while trimming only the positions with the largest embedded gains or lowest conviction — preserving the core tech thesis while reducing concentration risk.