Blog

The Fertilizer Shock Investors Are Missing

Since the onset of the conflict with Iran, the investment narrative seems to be dominated singularly by the specter of oil and energy price shocks. This concern has become so pervasive that it appears to have even overtaken the AI infrastructure narrative. Understandably, much of the world’s attention is fixated on the immediate, headline-driven volatility of Brent and WTI. However, one crucial consequence that does not seem to be getting as much coverage, yet is arguably more systemic in its implications, is the profound fracturing of the global fertilizer supply chain.

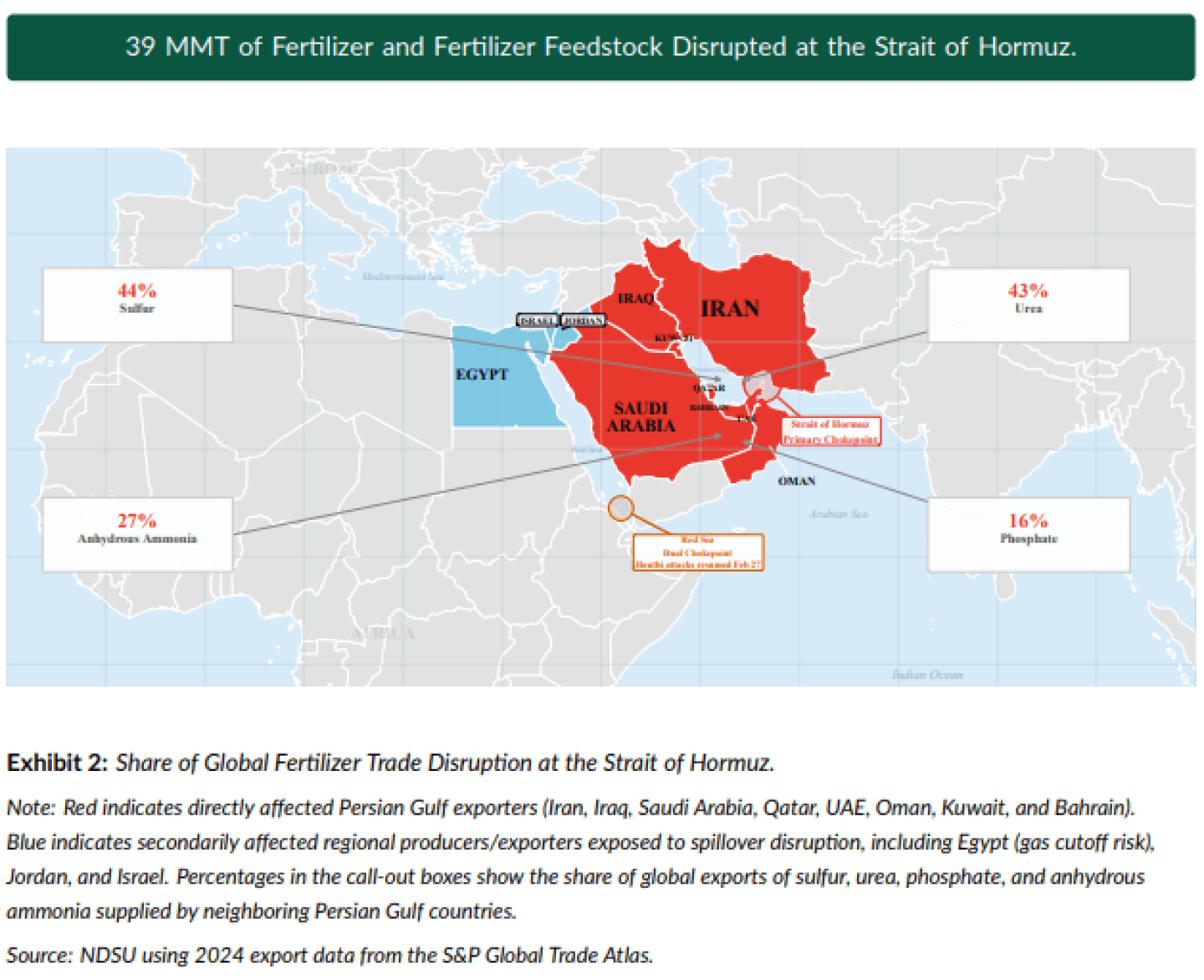

44% of global Sulfur exports and 43% of global Urea exports are channeled through the strait, which makes Hormuz a central artery of the global fertilizer supply chain.

Unlike crude oil, which can be drawn from the U.S. Strategic Petroleum Reserve or rerouted via terrestrial pipelines, there is no "strategic stockpile" for the global fertilizer supply chain. Fertilizer production is geographically concentrated and energy-intensive, meaning that when the Gulf’s export channels choke, the global agricultural system faces an immediate, irreversible decline in nitrogen availability for the critical Northern Hemisphere spring planting season.

For the professional investor, this is the "missing" trade. While the broader market treats this as a transient geopolitical tremor, the underlying mechanics suggest we are entering an era of forced yield suppression. The fertilizer shock is currently being priced as a cyclical commodity fluctuation, but it should be reclassified as a systemic structural failure—one that is set to reshape agricultural margins, exacerbate food commodity inflation, and force a radical reallocation of capital toward input-secure producers.

The Mid-Section: The CapEx Trap and Aging Infrastructure

Even prior to the choking of the Hormuz Strait, the fertilizer industry was already under pressure of a structural capital expenditure (CAPEX) gap that markets have consistently mispriced as a cyclical dip. Now with the main artery of its global supply chain effectively compromised, that gap has widened into a structural chasm.

The market consensus continues to treat fertilizer producers as highly cyclical, beta-heavy plays tethered to the spot price of natural gas. This heuristic is failing. In reality, the industry is currently defined by a prohibitive barrier to entry that is fundamentally disinflationary for the producer’s margins while being inflationary for the end-consumer’s basket.

To understand why this CAPEX gap is a permanent feature rather than a temporary lull, we must look at the trifecta of constraints currently throttling the industry:

Energy-Intensive Moats: The production of synthetic nitrogen via the Haber-Bosch process requires massive, consistent, and low-cost natural gas feedstock. As energy security becomes a national security mandate, new facilities are no longer purely economic projects—they are political ones. The "green-field" lead time for these facilities—from permitting to full-scale production—is now measured in 7 to 10 years, effectively locking out any short-term supply response to price spikes.

Permitting and Geopolitical Friction: The industry is arguably the most scrutinized sector in the world regarding ESG mandates and environmental impact. The regulatory burden to bring a new potash or phosphate mine online is higher today than it has been at any point in the last 40 years. We are seeing a "regulatory exhaustion" where brownfield optimization is the only viable path, and even that is being squeezed by capital allocation shifts toward buybacks over capacity expansion.

Decoupled Depreciation: Industry incumbents are running down their legacy assets rather than reinvesting for growth. When you look at the replacement cost of existing nitrogen and phosphorus infrastructure, it has inflated at a rate far exceeding the S&P 500 capital goods average. The industry is essentially cannibalizing its own future capacity to meet current dividend and buyback expectations, setting the stage for a severe, long-term supply contraction.

For the portfolio manager, this creates a distinct opportunity which involves the divergence between "production capability" and "market valuation." The market is pricing these companies as if they are merely commodity conduits, ignoring the fact that they own the most critical—and non-substitutable—infrastructure in the global economy.

As yield demand continues to climb to feed a growing population, the inability to expand the supply base guarantees that these firms will maintain pricing power well into the next decade.

Redirecting the Food Commodity ETF Narrative: The "Input Blind Spot"

For the past decade, institutional appetite for agricultural exposure has been funneled through broad-based food commodity ETFs (e.g., DBA or similar baskets). These products are designed to track the spot and future prices of grains, sugar, and livestock. However, this approach relies on a dangerous, outdated assumption: that agricultural prices are primarily a function of weather-driven supply and consumer-driven demand.

We are now operating in a regime where input scarcity—specifically fertilizer—acts as the primary determinant of yield floors.

Why Broad ETFs Are Failing to Capture the "Fertilizer Premium"

Standard commodity ETFs are inherently "Output-Weighted." They provide excellent beta to food price inflation but provide zero exposure to the structural bottlenecks occurring upstream. In a landscape of structurally higher fertilizer costs, the commodity-only approach results in two major flaws for the portfolio manager:

The Margin Compression Mirage: When fertilizer prices spike, the cost-of-production floor rises. If the commodity price moves up, it is often just offset by the rising cost of chemical inputs. Broad ETFs capture the output price but remain blind to the margin compression happening at the farm-gate level.

Sensitivity to "Input Shocks": Broad ETFs are vulnerable to supply-side "shocks" that occur within the fertilizer chain (e.g., natural gas spikes or regional export bans on potash). Because these ETFs are underweight (or completely lacking) in upstream chemical input providers, they fail to benefit from the capital flight into essential inputs that occurs during these disruptions.

A New Framework: Input-Weighted vs. Output-Weighted

Sophisticated portfolios must move beyond the "one-size-fits-all" commodity basket. To truly hedge against the fertilizer shock, managers must recalibrate their exposure to favor the Input-Weighted side of the equation.

First, we must distinguish between "caloric value" and "production value." The value is shifting from the harvest (commodity) to the catalysts (inputs).

Secondly, instead of simply holding a broad food ETF, a more resilient construction involves a barbell strategy: utilizing "input-monopolies" (large-scale fertilizer producers with localized energy hedges) alongside selective short-term commodity futures. This allows the portfolio to capture the pricing power of the fertilizer majors while hedging the margin volatility inherent in the commodities themselves.

Ultimately, if your current agricultural exposure is limited to crop-based ETFs, you are effectively betting on the harvest without owning the fertilizer that makes the harvest possible. In the current regime, the former is a gamble; the latter is essential infrastructure.

Automate Your Edge with Surmount Wealth

Identifying the "Fertilizer Shock" is only half the battle. In a market regime defined by rapid shifts and structural complexity, the greatest risk to a portfolio is not just being wrong—it is being too slow to react.

Traditional portfolio management relies on manual rebalancing and rigid, broad-based exposures that often fail to capture thematic opportunities like the fertilizer bottleneck until the alpha has already been priced out.

From Thesis to Execution

At Surmount Wealth, we believe your investment insights should be actionable at the speed of the market. Whether you are looking to implement a custom "Input-Weighted" agricultural strategy or leverage our sophisticated, prebuilt algorithmic models, Surmount provides the infrastructure to turn your thesis into a live, automated portfolio.

Bespoke Customization: You are not limited to generic ETFs. With Surmount, you can build a custom strategy that targets specific fertilizer-monopoly equities, integrates commodity futures, and applies your own proprietary constraints—all without writing a line of code.

Institutional-Grade Automation: Our platform eliminates the "execution drag" and emotional bias inherent in manual trading. Once your strategy is set, Surmount’s algorithms handle the rebalancing, monitoring, and risk adjustments in real-time, ensuring your portfolio remains perfectly aligned with your thesis as market conditions evolve.

Seamless Integration: We connect directly to your existing brokerage accounts. You don't need to move assets or manage multiple custodians to get institutional-level automation.

Why Wait for the Next Market Shift?

The "Fertilizer Shock" is a structural shift, not a passing trend. Sophisticated managers are already moving away from broad commodity beta toward targeted, input-focused strategies. The question is: Is your portfolio built to capitalize on this, or is it trapped in legacy instruments?

Don’t just watch the shift—automate your participation in it.

[Book a Demo with Surmount Wealth Today]