Blog

Opportunity Cost of Capital in Today's Market

Why the Risk-Free Rate Belongs in Every Allocation Decision

Every capital allocation decision carries an implicit trade-off. When you commit capital to equities, you are not simply betting on earnings growth — you are also forgoing whatever a risk-free alternative would have returned. That foregone return is the opportunity cost of capital, and it is one of the most consequential variables in portfolio construction. Yet in practice, many advisors treat it as an afterthought rather than a foundational input.

In the current environment, ignoring it is no longer a defensible position.

How Rising Rates Changed the Calculus

For most of the post-2008 period, the opportunity cost of capital was negligible. The Fed held rates near zero, Treasuries yielded almost nothing, and the practical cost of choosing equities over fixed income was minimal. That environment incentivised a decade-long stretch of equity allocation that compressed risk premiums and inflated valuations across asset classes.

That regime has ended. The interest rates and stock market relationship has fundamentally shifted. With the Fed funds rate having moved aggressively off the zero lower bound, short and intermediate-duration Treasuries now offer yields that are genuinely competitive with equity earnings yields.

The opportunity cost of capital has returned with force — and portfolio construction frameworks calibrated for a near-zero rate world need to be updated. For additional context on how this dynamic extends beyond US borders, see our piece on rising bond yields in Asia, which adds another layer of structural headwind to equity valuations.

The zero-rate era did not just suppress the opportunity cost of capital — it also turbocharged thematic narratives, a dynamic we explored in our piece on capitalising on emerging megatrends that remains relevant context today.

The Mechanics of Discounting Future Cash Flows

The opportunity cost of capital is not just a conceptual talking point — it is mechanically embedded in how equities should be valued. Every discounted cash flow model uses a discount rate that incorporates the risk-free rate as its floor. When that floor rises, the present value of future earnings falls, all else equal.

This matters acutely for growth-oriented equities, where a disproportionate share of intrinsic value is derived from cash flows projected years or decades into the future. A 100-basis-point increase in the discount rate has a far larger impact on a stock trading at 40x forward earnings than one trading at 12x. The opportunity cost of capital, in other words, is not a uniform tax on equities — it is a progressive one that hits expensive assets hardest.

When Bonds Start Competing With Stocks

The clearest expression of this dynamic is the earnings yield spread — the difference between the S&P 500's earnings yield and the yield on 10-year Treasuries. For most of the past two decades, that spread was positive and meaningful, providing a tangible return premium for accepting equity risk.

Today, Treasury yields vs equities tell a different story. The spread has turned negative for the first time since the early 2000s, meaning Treasuries are now yielding more than equities on an earnings basis. An advisor who cannot explain to a client or investment committee why they are accepting negative compensation for equity risk — relative to a risk-free alternative — is operating without a coherent framework.

Reading the Signals: Valuation Metrics That Matter Now

The opportunity cost of capital does not exist in isolation. Its implications are amplified or moderated by prevailing market valuation metrics. At present, those metrics offer little comfort.

The Equity Risk Premium Has Turned Negative

The equity risk premium — the excess return investors demand for holding equities over risk-free assets — has compressed to historically anomalous levels, a dynamic we examined in depth in our analysis of the equity risk premium in 2026. When adjusted for current Treasury yields, it has effectively turned negative on a trailing earnings basis. This is not a minor statistical curiosity. A negative equity risk premium means the market is pricing equities as if they carry no additional risk relative to government bonds — a proposition that is difficult to justify given earnings uncertainty, geopolitical risk, and elevated valuations.

Advisors building forward return assumptions into financial plans should treat a compressed or negative equity risk premium as a structural headwind, not a temporary condition to be waited out.

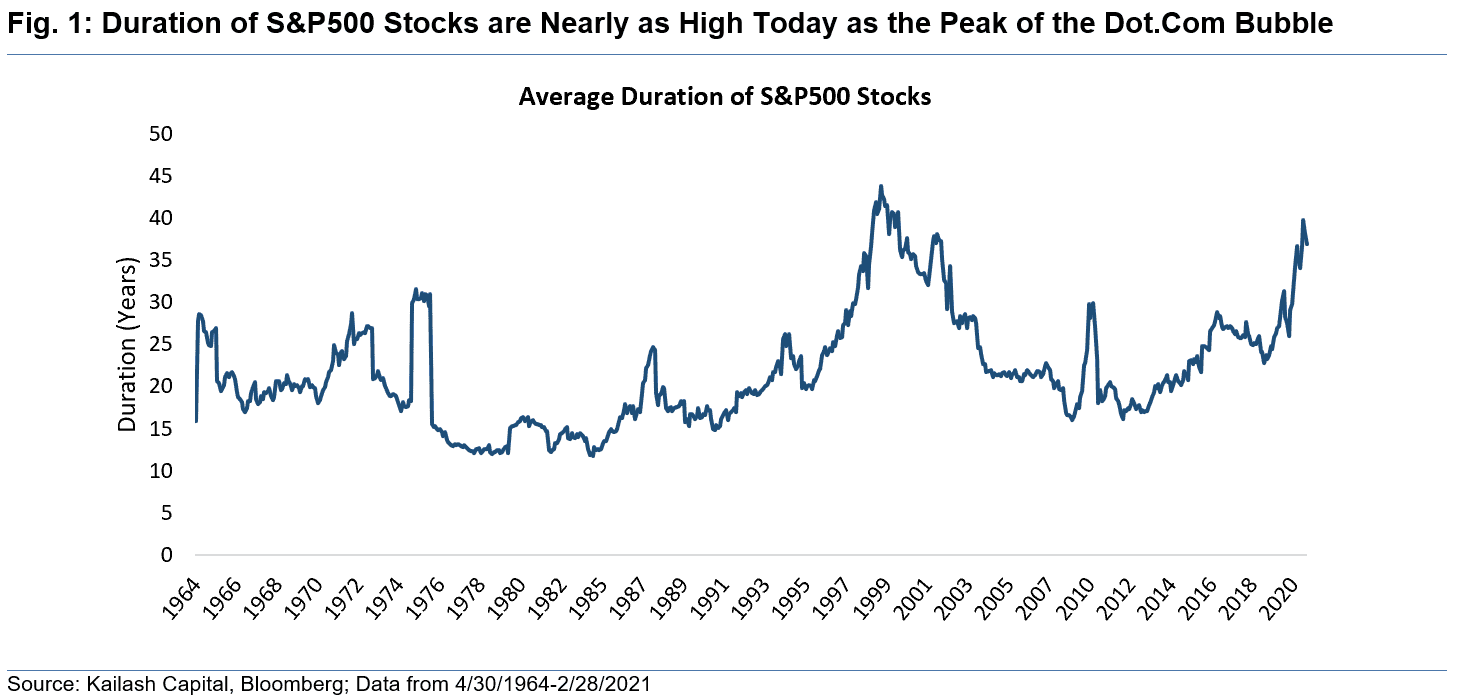

What CAPE and the Buffett Indicator Are Telling Us

Two of the most reliable long-run market valuation metrics — the Cyclically Adjusted P/E ratio (CAPE) and the Market Cap-to-GDP ratio — are both signalling elevated risk. CAPE is currently near levels last seen during the dot-com peak. The Market Cap-to-GDP ratio sits above 2x, a level with no meaningful historical precedent outside of the current cycle.

Neither metric is a timing tool. But both are robust predictors of long-run forward returns. Portfolios initiated at current valuation levels have historically delivered subpar returns over the subsequent decade. When these market valuation metrics are paired with a negative equity risk premium and elevated opportunity cost of capital, the aggregate signal is consistent: expected forward returns from equities are structurally compressed. For a rigorous treatment of ERP estimates across historical cycles, Aswath Damodaran's annual equity risk premium data at NYU Stern is the most widely cited institutional reference.

Translating Macro Insight Into Portfolio Action

Understanding the opportunity cost of capital is necessary but not sufficient. The harder question for practising advisors is how to act on it systematically within a portfolio allocation strategy.

Building a Framework for Risk-Adjusted Reallocation

A disciplined response to elevated opportunity cost does not require a binary shift out of equities. It requires a recalibration of the portfolio allocation strategy that reflects the new risk/reward environment. Advisors looking for a practical starting point can draw on the principles outlined in building a resilient investment strategy for uncertain times, which translates directly to the current rate environment.

In practical terms, this recalibration means several things. First, fixed income deserves a more serious role in portfolio construction than it did in the zero-rate era. Short to intermediate Treasuries now offer risk-adjusted returns that are genuinely competitive, and they do so without the valuation uncertainty embedded in equities. The earnings yield data from the Federal Reserve's FRED database provides the most reliable ongoing benchmark for tracking this spread.

Second, within equities, duration matters. High-multiple growth stocks carry the greatest sensitivity to changes in the opportunity cost of capital. Tilting toward lower-multiple, cash-generative businesses reduces that sensitivity without requiring a full exit from equities.

Third, systematic rebalancing rules — rather than discretionary judgment — are the most reliable way to enforce discipline when market conditions shift. This kind of disciplined reallocation is grounded in the same foundational logic as Modern Portfolio Theory — optimising the risk/return trade-off rather than chasing nominal returns in isolation. Risk-adjusted returns over a full cycle are far more dependent on process than on forecasting accuracy. The CFA Institute's framework on discount rates and equity valuation provides a rigorous grounding for advisors who want to formalise this approach in client-facing materials.

Conclusion

The opportunity cost of capital is not a new concept, but its practical relevance has rarely been higher. With Treasury yields competing directly with equity earnings yields, CAPE near historic highs, and the equity risk premium in negative territory, the case for a business-as-usual allocation to equities is difficult to make on first principles.

For investment advisors and portfolio managers, the obligation is not to predict what the market will do — it is to ensure that every allocation decision is made with full awareness of what is being given up. That is what a rigorous application of the opportunity cost of capital demands.

Automate Your Allocation Thesis With Surmount Wealth

Understanding that the opportunity cost of capital has shifted is one thing. Building a portfolio that systematically responds to it is another.

That is exactly what Surmount Wealth's automated trade strategies are designed to do. Whether you want to deploy a prebuilt strategy or build something custom around your specific allocation thesis, Surmount gives you the infrastructure to move from insight to execution — consistently, without emotional drag, and across your entire client book.

Consider a hypothetical strategy — call it the Rate-Adjusted Equity Allocation Model (RAEA) — built around the dynamics discussed in this blog. The strategy would monitor the earnings yield spread between the S&P 500 and 10-year Treasuries in real time. When the spread compresses below a defined threshold, it would automatically reduce equity duration exposure — trimming high-multiple growth positions — and rotate into short-duration Treasuries and lower-multiple value equities. When the spread widens and the equity risk premium recovers to historically compensated levels, it scales back into equities systematically. No hesitation. No committee. No lag.

Note: The RAEA is a hypothetical strategy presented for illustrative purposes only. It does not represent a live or available product.

This is just one example of what is possible on the platform. If you are managing portfolios in this environment and still executing allocation shifts manually, you are leaving both precision and time on the table. Book a demo with Surmount Wealth today and see how automation can turn your macro framework into a disciplined, repeatable edge.

FAQ: Opportunity Cost of Capital

What is opportunity cost of capital?

It is the return foregone by choosing one investment over a risk-free alternative. In portfolio construction, it sets the minimum acceptable return threshold for any allocation.

Why does it matter for equity allocation now?

Treasury yields now rival equity earnings yields, meaning the opportunity cost of capital for holding equities has risen sharply. Portfolios that ignore this are accepting uncompensated risk.

How do interest rates affect stock valuations?

Higher interest rates increase the discount rate used in equity valuation models, reducing the present value of future cash flows — particularly for high-multiple growth stocks.

What is the equity risk premium today?

The equity risk premium has turned negative in several market segments, meaning equities are no longer compensating investors for the additional risk they carry over Treasuries.

Can opportunity cost of capital be automated?

Yes — platforms like Surmount Wealth allow advisors to build rules-based strategies that automatically respond to changes in yield spreads and valuation signals, removing execution lag and emotional bias.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.