Blog

Why Does the Stock Market Perform Better After Hours?

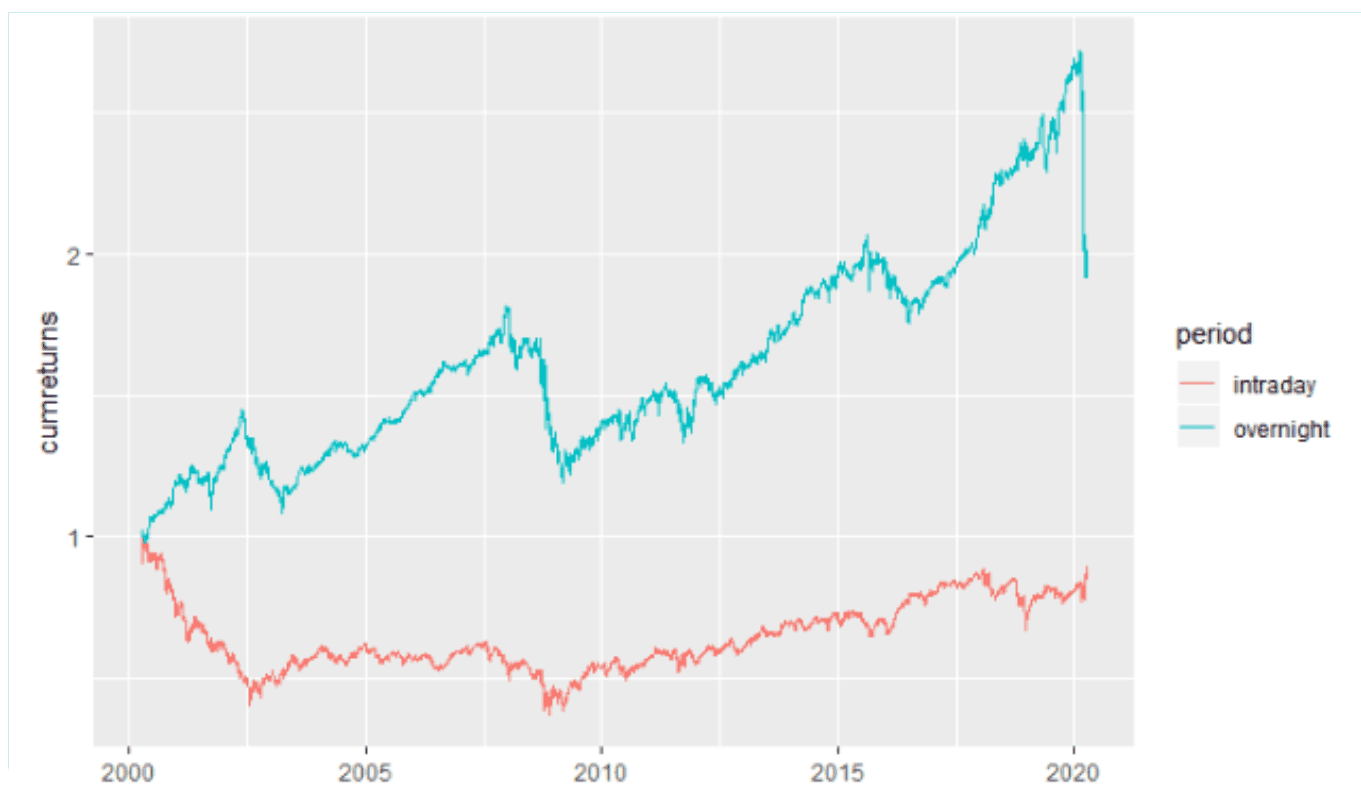

Professional traders have long noticed a curious pattern: much of the market's cumulative return doesn't happen during the regular session. Instead, it accumulates between the closing bell and the next morning's open. For advisors building or stress-testing systematic strategies, understanding why does the stock market perform better after hours is more than academic curiosity — it has direct implications for execution timing, risk exposure, and portfolio construction. This pattern, often tied to broader after-hours trading returns data, has been documented across decades of price history and remains a fixture of market microstructure discussions.

Understanding the Overnight Return Anomaly

The overnight return anomaly refers to the empirical observation that a disproportionate share of equity index gains occurs while markets are closed, rather than during the 9:30 a.m.–4:00 p.m. session. Academic studies going back to the 1990s have shown that if an investor had held a broad index only overnight — buying at the close and selling at the next open — cumulative returns would have vastly outpaced a strategy that held only through the regular session. This is a key reason why does the stock market perform better after hours continues to draw attention from quantitative researchers and portfolio managers alike.

Intraday vs. Overnight Stock Returns: What the Data Shows

Comparing intraday vs. overnight stock returns reveals a persistent asymmetry. Historical backtests on major indices show overnight sessions contributing the bulk of long-term price appreciation, while intraday sessions have, over some multi-decade periods, been roughly flat or even negative on a cumulative basis. This doesn't mean intraday trading is worthless — volatility, liquidity, and price discovery still happen predominantly during the day — but it does reframe how return sources should be attributed within a portfolio.

Close-to-Open Returns vs. Open-to-Close Performance

Breaking this down further, close-to-open returns — the price movement between one day's close and the next day's open — have historically outperformed open-to-close returns on a cumulative basis for many broad indices. This is a distinct signal from simple day-over-day price change, and it's precisely why does the stock market perform better after hours is treated as its own line of inquiry rather than folded into general volatility research. Isolating close-to-open returns allows analysts to separate overnight information effects from intraday trading dynamics.

What Drives the Overnight Risk Premium

Several structural explanations have been proposed for the overnight risk premium embedded in these returns.

Earnings Releases, News Flow, and Order Imbalances

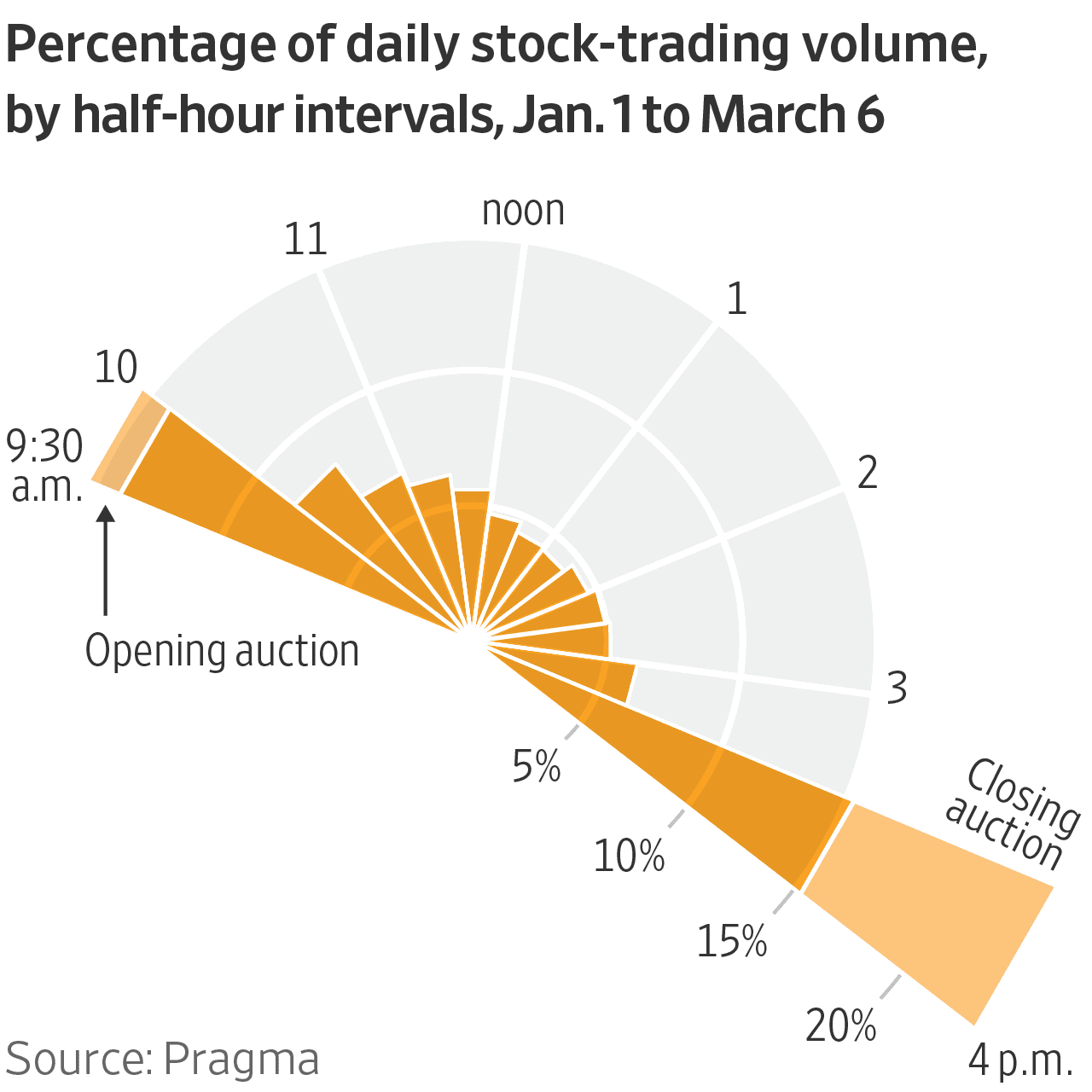

A large share of corporate earnings announcements, macroeconomic data releases, and material news occurs outside regular trading hours. This concentration of information flow can create systematic after-hours trading returns as markets digest news before the next open, often resulting in gap-driven price adjustments that resolve before intraday trading fully absorbs the information.

Institutional Order Flow and Overnight Positioning

Overnight positioning by institutional investors — including index rebalancing, mutual fund settlement mechanics, and risk-management flows executed near the close — may also contribute to the pattern. Some researchers point to systematic buying pressure at the open tied to retirement account contributions and passive fund inflows — flows that also help explain why staying disciplined through volatile stretches tends to reward patient allocators, often queued for execution at standardized times.

Is This a Persistent Anomaly or a Statistical Artifact?

A fair question for any advisor evaluating this pattern: is it durable, or is it an artifact of a specific sample period? The honest answer is mixed. While the overnight risk premium has appeared across multiple decades and multiple markets, its magnitude has varied significantly by regime — a reminder that, as we've argued elsewhere, disciplined process tends to outperform reactive timing decisions, and transaction costs, bid-ask spreads, and tax treatment can erode much of the theoretical advantage for anyone attempting to trade it directly and frequently.

Systematic Overnight Trading: From Observation to Strategy

For advisors interested in incorporating this research into client portfolios, the practical challenge isn't identifying the anomaly — it's operationalizing it. Systematic overnight trading requires disciplined, rules-based execution rather than discretionary timing — and, as discretionary decision points tend to erode client outcomes, removing manual judgment from the process is often the point, not a compromise, since the effect is measured in aggregate over long holding periods, not captured through occasional manual trades.

Building an Overnight Drift Strategy Within a Portfolio

A theoretical overnight drift strategy might involve systematically entering positions near the close and exiting near the next open, applied across a diversified basket rather than single names, with rules governing position sizing, rebalancing frequency, and drawdown limits. Backtesting such an overnight drift strategy against varying market regimes — including decisions around rebalancing frequency — is essential before considering any live implementation.

Conclusion

The evidence behind why does the stock market perform better after hours is compelling but nuanced. Overnight sessions have historically contributed an outsized share of long-term equity returns, driven by information flow, order imbalances, and institutional positioning mechanics. For advisors, the real value lies not in chasing the anomaly manually, but in understanding it well enough to evaluate whether a systematic, backtested approach fits a given client's risk profile and mandate.

Automate Your Market Thesis with Surmount Wealth

Understanding an anomaly like overnight drift is one thing. Building, testing, and executing on it — consistently, without emotional override — is another challenge entirely.

Surmount Wealth lets advisors and portfolio managers take theses like this one and turn them into disciplined, automated strategies layered directly onto existing brokerage accounts, with no fund transfers and no need to code from scratch.

Illustrative Concept: The "Overnight Gap Monitor"

(Hypothetical strategy for illustration purposes only. Not an existing Surmount product, a live strategy, or investment advice.)

A rules-based framework that could, in theory, address the dynamics discussed above:

Systematically identifies close-to-open positioning opportunities across a diversified equity basket

Applies pre-set position sizing and volatility-adjusted exposure limits

Executes entries and exits on a consistent schedule, removing manual timing decisions

Incorporates drawdown thresholds and rebalancing rules to manage overnight risk

Fully backtestable across historical regimes before any live deployment

This is a hypothetical illustration, not investment advice or a recommendation — but it reflects the kind of thesis-to-execution pipeline Surmount Wealth is built for. Whether you're exploring overnight effects, sector rotation, or a proprietary signal of your own, our platform lets you apply institutional-grade automation to systematic overnight trading and any other thesis you already believe in.

Ready to see how your own thesis could be systematized? Book a demo with Surmount Wealth today and explore what automated, rules-based execution could look like for your practice.

Book a Demo with Surmount Wealth →

FAQ: Why Does the Stock Market Perform Better After Hours?

What is the overnight return anomaly?

It's the pattern where equity gains concentrate in overnight sessions rather than regular trading hours, a well-documented overnight return anomaly in academic research.

Why do stocks gain more overnight?

Earnings releases, macro data, and institutional order flow concentrated outside market hours help explain why does the stock market perform better after hours.

How reliable are close-to-open returns?

Close-to-open returns have historically outperformed intraday sessions, but magnitude varies by regime and can be eroded by trading costs.

Can advisors trade overnight drift directly?

Direct manual trading is impractical due to costs; a backtested, rules-based overnight drift strategy is the more viable approach.

Is the overnight risk premium permanent?

The overnight risk premium has persisted across decades, but its size fluctuates, so it shouldn't be treated as a fixed, guaranteed edge.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.