Blog

Dollar-Cost Averaging vs Lump Sum: What Advisors Should Know

Dollar-Cost Averaging vs Lump Sum: Framing the Debate for Client Portfolios

Few questions surface more often in client conversations than dollar-cost averaging vs lump sum investing. A client inherits a windfall, liquidates a concentrated position, or simply accumulates cash on the sidelines — and now faces the decision of deploying it all at once or spreading entries over time. The debate isn't new, but it resurfaces every time markets sit near all-time highs, as retail sentiment around “waiting for the dip” makes clear.

For advisors, the more useful framing isn't which method wins in backtests — it's which method a given client can actually stick to without emotional interference, a reactive impulse we address in our guide to making better financial decisions when the news cycle is chaotic.

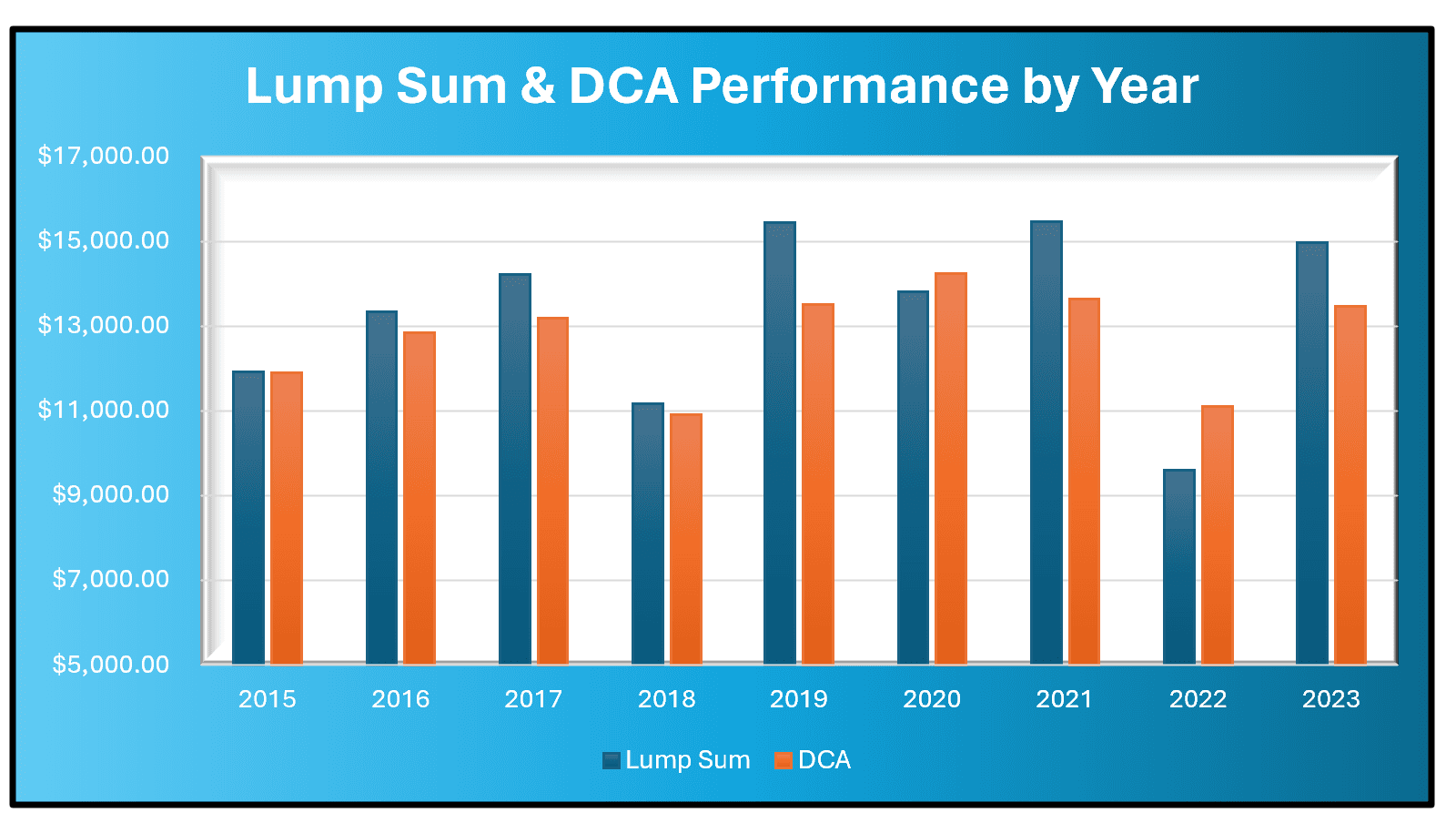

The Case for Lump Sum Investing

The historical data is fairly consistent: putting capital to work immediately tends to outperform phased entry in most rolling periods, simply because markets rise more often than they fall. Delaying exposure means delaying compounding, and the opportunity cost of sitting in cash compounds just as steadily as the market itself.

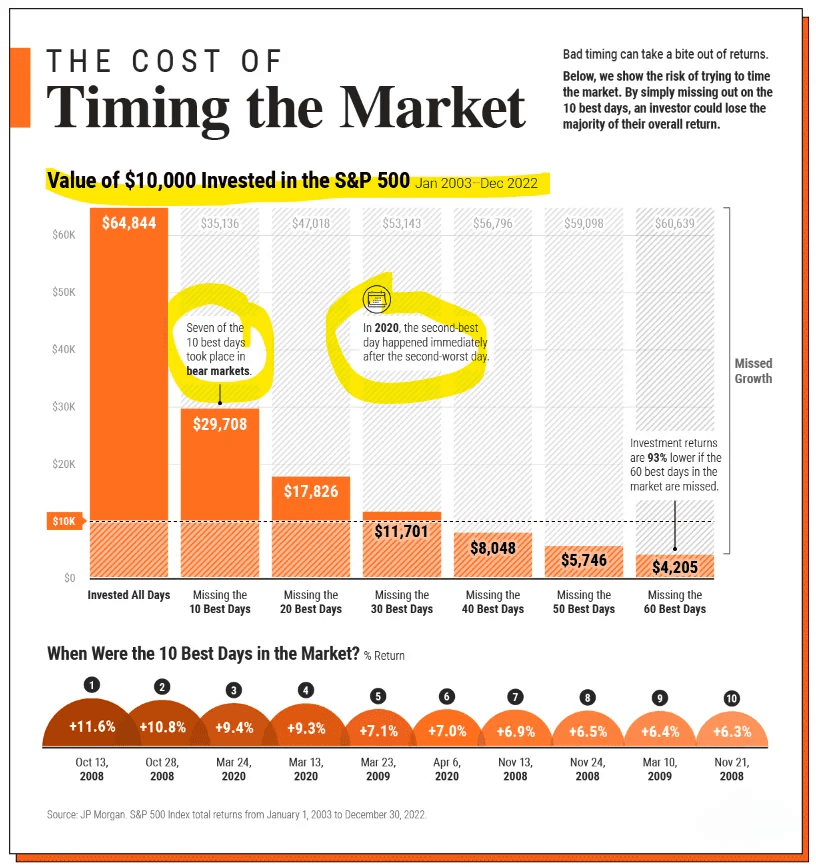

What the Data Says About Time in the Market vs Timing the Market

This is the classic time in the market vs timing the market argument, and it holds up across most long-horizon studies. Investors who attempt to wait for a better entry point frequently miss the strongest recovery days, which cluster unpredictably around volatility spikes. The math favors immediate deployment for clients with long horizons and high risk tolerance. The behavioral reality, however, is a separate question entirely.

The Case for Dollar-Cost Averaging

Lump sum wins on average, but averages don't comfort a client staring at a 12% drawdown three weeks after funding an account. Phased entry exists to solve a human problem, not a mathematical one.

How Cash Drag Erodes Long-Term Returns

The tradeoff is real. Holding back capital to phase into a position creates cash drag — uninvested assets sitting idle while the broader portfolio's target allocation goes unmet. Over long horizons, cash drag can meaningfully reduce total return, particularly in extended bull markets.

Advisors need to weigh this cost transparently rather than defaulting to phased entry as a “safe” choice — the same opportunity-cost math we walk through in our breakdown of whether elevated cash still makes sense at today's yields.

Managing Behavioral Bias in Investing During Volatile Entries

The counterargument is that behavioral bias in investing decisions often outweighs the mathematical edge of lump sum deployment. A client who panics and exits after a single bad week has locked in a worse outcome than one who dollar-cost averaged and stayed the course.

Phased entry is, in many cases, a behavioral hedge more than a return-maximizing strategy — the same cognitive traps we explore in our piece on why institutional investors should systematically audit their worst performers. For advisors, managing these dynamics in client conversations is often the higher-value service.

Market Timing Risk and Sequence of Return Risk in Either Approach

Both approaches carry exposure to market timing risk, just at different points in the process. Lump sum investors bear it upfront: a poorly timed entry ahead of a correction can take years to recover from. DCA investors bear it in a different form — sequence of return risk during the accumulation window, where early losses before full deployment can permanently reduce the compounding base.

Neither method eliminates risk; each simply redistributes it differently across time — a dynamic we unpack further in our analysis of why rebalancing matters more than market forecasts. This is precisely why the dollar-cost averaging vs lump sum decision should be treated as a risk-allocation exercise, not a binary “better/worse” choice.

Why Systematic Investing Matters More Than the Method You Choose

The deeper issue advisors face isn't DCA versus lump sum — it's execution consistency. Systematic investing removes the emotional variable that undermines both strategies when applied manually. A client who commits to a six-month phased entry but pauses buying during a dip because it “feels wrong” has abandoned the strategy at the exact moment it was designed to work.

Rules-Based Investing as a Bridge Between DCA and Lump Sum

This is where rules-based investing becomes valuable. A pre-defined schedule — triggered by calendar intervals, price thresholds, or volatility bands — enforces the discipline that manual execution often lacks, echoing the case we make in The Hidden Cost of Advisor Optionality for reducing discretionary decision points. Systematic investing frameworks can also blend the two approaches: a partial lump sum deployment paired with scheduled entries for the remainder, executed automatically regardless of short-term sentiment.

Conclusion: Choosing (and Executing) the Right Approach for Each Client

There's no universal answer to dollar-cost averaging vs lump sum — the right choice depends on the client's time horizon, liquidity needs, and capacity to tolerate short-term drawdowns without deviating from plan. What matters more than the method itself is whether it's executed consistently. A sound strategy inconsistently applied often underperforms a mediocre one that's followed to the letter.

Automate Any Entry Strategy with Surmount Wealth

Deciding between dollar-cost averaging and lump sum is only half the equation — the other half is execution. Manual rebalancing, discretionary re-entry timing, and client hand-holding during volatile weeks all introduce the exact behavioral risk this piece has been discussing.

Surmount Wealth's automation infrastructure lets advisors deploy either strategy — or a hybrid of both — as a fully rules-based, automated portfolio rebalancing framework layered directly onto existing brokerage accounts. No fund transfers. No custom code. Just professional-grade strategy logic, running on schedule, immune to sentiment.

Hypothetical Strategy Illustration: Consider a concept like a “Volatility-Scaled Entry Monitor” — a systematic framework that could scale capital deployment inversely to a volatility index, committing larger tranches during calmer periods and smaller, more frequent tranches during elevated volatility. This is a hypothetical concept for illustrative purposes only, not an actual Surmount Wealth strategy or investment recommendation, but it demonstrates the kind of thesis that automation makes executable without daily discretionary oversight.

Why advisors are automating entry and rebalancing strategies with Surmount:

Remove emotional decision-making from every trade execution

Apply institutional-grade, rules-based investing logic to client accounts without transferring assets

Test hypothetical entry strategies against historical data before deploying capital

Scale a single strategy thesis across multiple client accounts simultaneously

Maintain full transparency and auditability for every automated decision

Whatever thesis you're building for clients — phased entry, lump sum with rebalancing bands, or something more complex — Surmount Wealth can help you automate it with precision.

Book a demo today and see how systematic execution can strengthen your client strategy conversations.

This strategy illustration is hypothetical and for educational purposes only. It does not constitute investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. All investment strategies involve risk of loss.

FAQ: Dollar-Cost Averaging vs Lump Sum

Is lump sum better than dollar-cost averaging?

Historically, lump sum investing outperforms dollar-cost averaging in most rolling periods, since markets rise more often than they fall. But dollar-cost averaging vs lump sum is also a behavioral question, not just a mathematical one.

What causes cash drag in portfolios?

Cash drag happens when capital sits uninvested while waiting to be phased into the market, missing potential compounding. It's the primary cost of a slow, staged entry strategy.

Does DCA reduce market timing risk?

Dollar-cost averaging reduces the impact of a single poorly timed entry but introduces its own form of market timing risk during the accumulation window. Neither approach eliminates timing risk entirely.

Why use systematic investing over manual entry?

Systematic investing removes emotional decision-making from execution, which often undermines both DCA and lump sum strategies when applied manually. Rules-based execution stays consistent regardless of sentiment.

How does rules-based investing help with entries?

Rules-based investing enforces a pre-defined schedule or threshold for capital deployment, removing hesitation and inconsistency from the process. It can also blend both strategies automatically.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.