Blog

Hyperscaler Debt Issuance: What Advisors Must Know

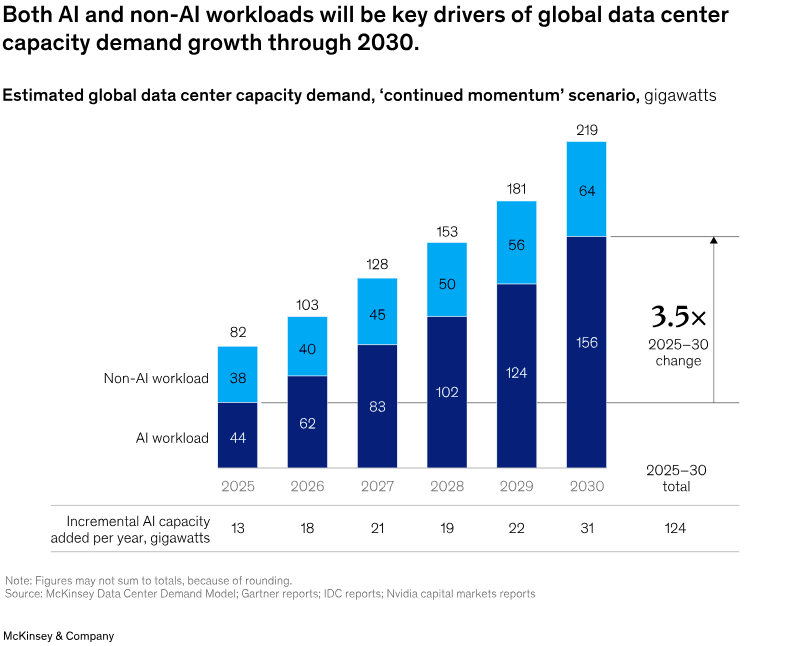

The scale of capital being deployed into AI infrastructure is without precedent in corporate history. The five major hyperscalers — Alphabet, Amazon, Meta, Microsoft, and Oracle — are on track to spend a combined $757 billion in FY2026, with Goldman Sachs projecting that figure could climb toward $1.1 trillion in FY2027. That number is not being funded by free cash flow alone.

Hyperscaler debt issuance has become the financing mechanism of choice for this buildout, and its implications span equity valuations, fixed income spreads, and broader portfolio risk management.

Why Hyperscaler Debt Issuance Is Accelerating

Goldman’s $1.1 Trillion CapEx Projection

Goldman’s revised FY2027 estimate represents a near 45% increase over the current consensus of $920 billion. For context, this would make hyperscaler capital expenditure alone one of the largest single-sector spending events in financial history — surpassing the entire GDP of most developed economies.

This is not discretionary spending. Commitments to AI model providers have locked in demand for computing capacity years in advance. The pipeline is effectively pre-sold, and the capital must follow.

How AI Infrastructure Spending Is Being Financed

With free cash flow increasingly insufficient to fund these commitments, hyperscalers are turning aggressively to debt and equity markets:

Alphabet recently raised approximately $85 billion through equity issuance and private placements

Oracle has signaled plans to raise roughly $40 billion via combined debt and equity in its upcoming fiscal year — even as its free cash flow ran negative $23.7 billion in the prior year

Bank of America raised its hyperscaler debt issuance estimate for 2026 to $175 billion in mid-March, up from $120 billion — and analysts expect further revisions upward

This pace of AI infrastructure spending financed through capital markets creates a structural feedback loop: higher capex demands more debt, which raises interest burden, which pressures free cash flow further. Advisors managing multi-asset portfolios should monitor this loop carefully, particularly given what elevated long-duration yields already mean for discount rates — a dynamic we explored in depth in our analysis of what the 30-year Treasury yield is signaling in 2026.

Equity Dilution Risk in Tech Portfolios

Equity issuance at this scale is a direct dilution event for existing shareholders. When Alphabet raises $85 billion in new equity, every existing share represents a fractionally smaller claim on future earnings. At current valuations — where the S&P 500 trades above 32 times earnings — dilution compounds the pressure from an already thin margin for error.

Portfolio managers running benchmark-relative strategies with heavy technology concentration are particularly exposed — as we have previously documented, the S&P 500 concentration bubble has already loaded many passive and quasi-passive portfolios with tech exposure that is rarely stress-tested against dilution scenarios at this magnitude.

Portfolio Exposure to AI CapEx — What the Numbers Mean

For advisors, the risk embedded in hyperscaler debt issuance is not just about the companies issuing the debt. It is about the second and third-order effects across fixed income and equity allocations.

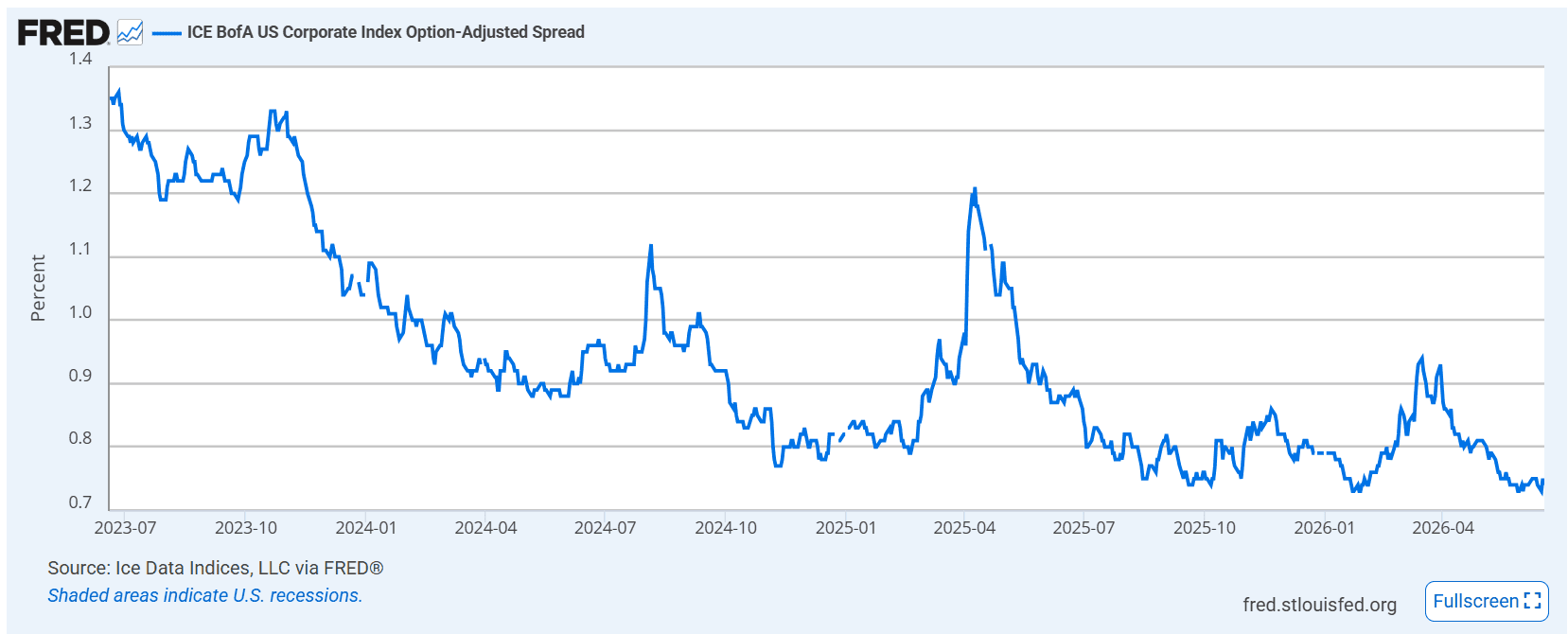

Investment Grade Tech Bonds Under Pressure

Hyperscaler debt overwhelmingly prices into the investment grade tech bonds universe. As issuance volumes surge, several dynamics merit attention:

Supply pressure on existing IG tech holdings as new paper competes for the same buyer base

Spread widening risk if demand does not absorb $175B+ in annual issuance at current tightness

Duration concentration — much of this debt is issued at long tenors, creating embedded sensitivity to the same rate environment already stressing long-duration equity valuations

For fixed income allocators, the investment grade tech bond market is no longer a passive component of a blended portfolio. It is an active expression of a view on AI infrastructure spending and hyperscaler credit quality.

Tech Sector Debt Risk Across Multi-Asset Portfolios

The more subtle problem is double-counting. Many multi-asset portfolios carry tech sector debt risk in both their equity and fixed income sleeves simultaneously — owning both the stock and the bonds of the same hyperscaler. In a stress scenario where AI demand disappoints and hyperscaler revenues compress, both positions move against the portfolio at the same time.

This correlation risk is structurally similar to the concentration dynamics that have distorted broad equity indices — and it is equally under-disclosed.

AI Data Center Financing and the Demand Uncertainty Problem

Here is the variable that makes hyperscaler debt issuance uniquely difficult to model: the demand side is uncertain.

Roughly half of the data center capacity under construction is committed to AI model providers — organizations currently burning tens of billions of dollars annually in operational losses. Recent pricing shifts from subscription-based to usage-based models have introduced additional unpredictability into the demand forecast. If AI adoption scales as projected, this infrastructure becomes strategically indispensable. If it does not, advisors are looking at a stranded asset problem financed with corporate bonds sitting in their clients’ fixed income sleeves.

The demand uncertainty is compounded by a hardware obsolescence dynamic that gets little attention — and sits alongside a broader macro backdrop in which rising sovereign yields globally are already tightening the conditions under which this debt is being issued, as we examined in our recent piece on rising bond yields in Asia and what they mean for US investors. GPUs — which represent approximately 40% of data center build costs — have realistic useful lives of two to three years for mission-critical workloads, far shorter than the five to six year depreciation schedules hyperscalers are currently booking.

This means maintenance and replacement costs are being systematically understated, which in turn flatters the free cash flow projections underpinning these debt offerings.

How Advisors Should Be Repositioning Now

Given these dynamics, a few positioning principles are worth building into portfolio frameworks:

Audit fixed income sleeves for IG tech bond concentration — quantify how much of the credit portfolio is effectively a leveraged bet on AI infrastructure demand

Stress-test equity positions for dilution scenarios — model EPS impact if major hyperscalers issue another 10–15% of current share counts over the next 24 months

Monitor AI data center financing news as a leading indicator — debt issuance announcements and spread movements in hyperscaler paper are forward-looking signals on capital market stress, much like the freight and credit delinquency signals we outlined in our recession indicators framework for portfolio managers

Revisit equity risk premium assumptions — at 32x earnings, the implied equity yield already sits below current risk-free rates; additional leverage at the corporate level makes that math worse

Build systematic rules around AI capex thresholds — encode rebalancing triggers around defined debt-to-EBITDA levels or credit spread thresholds rather than making discretionary adjustments

Conclusion

Hyperscaler debt issuance at $175 billion and rising is not simply a corporate finance footnote. It is a portfolio-level event with real implications across equity dilution risk, investment grade bond spreads, and multi-asset correlation. Advisors who treat AI infrastructure spending as an equity story only are missing half the exposure sitting inside their clients’ portfolios.

The demand assumptions underpinning this debt are untested at scale. The GPU replacement cycle is faster and more expensive than depreciation schedules suggest. And the capital markets are being asked to absorb a volume of new issuance that has no modern precedent in a single sector.

The advisors best positioned are those who have already encoded these variables into their portfolio frameworks — systematically, not reactively.

Automate This Thesis With Surmount Wealth

Understanding the risk embedded in hyperscaler debt issuance is one thing. Acting on it — consistently, at the right time, across every client portfolio — is the harder problem.

That is exactly what Surmount Wealth is built for. Surmount is an AI-driven automated investing platform that lets advisors and portfolio managers build, test, and deploy rules-based trade strategies directly on existing brokerage accounts — no fund transfers, no coding required.

Consider a hypothetical strategy — the “CapEx Debt Monitor” (illustrative concept only, not a live strategy or investment advice):

A rules-based allocation model that systematically tracks hyperscaler debt issuance volumes, investment grade tech bond spreads, and free cash flow deterioration signals across the five major hyperscalers. When issuance volume crosses a defined threshold or spreads widen beyond a set parameter, the strategy:

Automatically trims equity exposure to the highest-capex hyperscalers

Reduces IG tech bond duration in fixed income sleeves

Rotates into short-duration, value-tilted alternatives

Re-enters positions systematically when spread conditions normalize

Executes across client accounts with zero manual intervention

Why advisors choose Surmount:

Prebuilt strategy library — deploy proven frameworks immediately

Fully custom strategies — encode any proprietary thesis, including the dynamics discussed in this post

No fund transfers required — strategies run on your clients’ existing brokerage accounts

Backtesting included — validate before deploying live capital

Scalable across your entire book — one strategy, every client, executed simultaneously

Stop letting your best research sit in a document. Turn it into a live, automated strategy.

► Book a Demo with Surmount Wealth Now

FAQ: Hyperscaler Debt Issuance

What is hyperscaler debt issuance?

It refers to bond and equity offerings by major cloud and AI infrastructure companies used to finance data center buildouts. Volumes are projected to exceed $175 billion in 2026 alone.

Why does AI capex financing matter to advisors?

It creates simultaneous equity dilution risk and investment grade bond supply pressure — a double exposure most multi-asset portfolios are carrying without explicitly pricing it in.

How does equity dilution risk affect tech portfolios?

When hyperscalers issue new shares at scale, existing shareholders hold a smaller claim on future earnings — compounding the problem at already elevated valuations above 32x earnings.

What is tech sector debt risk?

It is the credit and spread risk embedded in investment grade bonds issued by large technology companies. Surging issuance volumes make this an active portfolio risk, not passive fixed income exposure.

How can advisors hedge AI infrastructure spending risk?

By building systematic, rules-based rebalancing triggers around capex announcements, credit spread levels, and free cash flow signals — rather than making reactive discretionary adjustments after conditions shift.