Blog

Hyperscaler Spending and Portfolio Risk in 2026

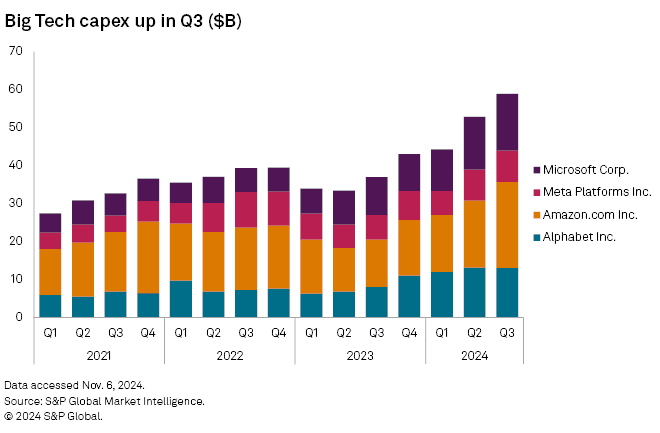

The four largest technology companies in the world — Amazon, Microsoft, Alphabet, and Meta — are on track to spend a combined $725 billion on AI infrastructure in 2026. That figure represents a 77% increase over 2025's already-record $410 billion, and Goldman Sachs projects the number will cross $1 trillion by 2027. For professional investment advisors and portfolio managers, this isn't just a macro data point. It is a direct signal about hyperscaler spending and portfolio risk that needs to be factored into allocation decisions now — before earnings season closes the window.

The Scale of the 2026 AI CapEx Buildout

To understand the full weight of big tech CapEx 2026, it helps to look at each company individually. The spending levels across these four names are not uniform — and the divergences matter for portfolio construction.

Big Tech CapEx 2026 by the Numbers

Here is where each hyperscaler stands heading into the second half of 2026:

Amazon: ~$200 billion — the largest absolute spender, anchored by AWS infrastructure expansion

Microsoft: ~$190 billion — roughly $25 billion attributed to higher memory and component costs driven by AI workload demands

Alphabet (Google): $180–190 billion — guidance raised by $5 billion after Q1 earnings; the company has also resorted to share issuance to raise additional funds

Meta: $115–135 billion — the smallest in absolute terms but the steepest proportional jump, up approximately 81% from $69 billion in 2025

Taken together, these four companies represent the most concentrated infrastructure investment cycle in the history of public markets. For advisors building systematic strategies around AI infrastructure investment risk, this is the central variable.

Why This Cycle Is Different

Previous technology investment cycles — cloud buildout, mobile infrastructure, broadband expansion — were gradual and distributed across many players. This cycle is different for three key reasons:

Concentration: Four companies are driving the overwhelming majority of spend, creating asymmetric exposure in any portfolio with significant large-cap tech weight.

Speed: The 77% year-over-year increase in combined CapEx has outpaced revenue growth, meaning these companies are spending ahead of demonstrated monetization at an unprecedented rate.

Funding mechanisms: At least one major hyperscaler has already turned to equity dilution to fund infrastructure. Others are drawing down cash reserves or increasing debt issuance — all of which carry distinct implications for shareholder value.

As we explored in our earlier analysis of why credit markets are skeptical of the tech rally, bond markets are already pricing in execution risk that equity valuations have not yet acknowledged.

Where the Portfolio Risk Lives

Hyperscaler spending and portfolio risk converge at a specific point: when capital allocation outpaces monetization. We are approaching — and may have already crossed — that threshold.

Free Cash Flow Pressure on Mega-Cap Tech

Free cash flow pressure on mega-cap tech is the most immediate consequence of this spending cycle. CapEx at these levels competes directly with dividends, buybacks, and debt repayment — and it compresses the FCF yields that justify current equity multiples.

Consider the math: when a company's CapEx-to-Revenue ratio rises from 10% to 30–50% — as several hyperscalers are now operating — the cash available for return to shareholders shrinks materially. The market has largely priced these companies on the assumption that AI monetization will accelerate to cover the gap. That assumption is being tested in real time.

Portfolio managers relying on historical FCF models for these names are working with frameworks built for a fundamentally different capital structure. The AI arms race has changed the equation, and it has not changed it slowly.

For a deeper look at how the 30-year Treasury yield environment in 2026 compounds this pressure by raising the discount rate on future earnings, the implications for mega-cap tech multiples are significant.

Shareholder Dilution and the Big Tech Funding Gap

Shareholder dilution in big tech is not a hypothetical risk anymore. At least one major hyperscaler has already issued equity to fund its AI infrastructure buildout — a meaningful shift for companies that have historically returned capital rather than absorbed it.

The key question for portfolio managers is: who follows? If Amazon and Microsoft are spending $190–200 billion each, and if AI monetization timelines extend beyond current projections, the pressure to tap equity markets will grow. Each dilutive issuance reduces earnings per share, compresses return on equity, and shifts the fundamental profile of these businesses from capital-light compounders to capital-intensive infrastructure operators.

This transition — from asset-light to asset-heavy — is something the equity market has been slow to price. Credit markets, as discussed in our analysis of AI barbell portfolio construction for 2026, have been far less forgiving.

AI Arms Race Portfolio Positioning for RIAs

Understanding the risk is necessary. Acting on it systematically is the real challenge. AI arms race portfolio positioning requires advisors to move beyond passive large-cap tech exposure and toward frameworks that account for capital intensity, monetization timing, and earnings-season volatility.

There are several structural approaches worth evaluating:

Reduce unhedged concentration: Portfolios with outsized passive tech exposure via major indices carry more hyperscaler risk than many advisors have explicitly modeled.

Rotate toward AI beneficiaries, not just architects: The energy infrastructure, industrial, and logistics sectors that support AI operations are increasingly attractive relative to the hyperscalers themselves. This is consistent with the global diversification thesis we outlined earlier in 2026.

Stress-test FCF assumptions: Run sensitivity analysis on FCF models underpinning hyperscaler positions, particularly under scenarios where CapEx remains elevated and revenue growth moderates.

Build rules-based triggers: Systematic strategies that define rebalancing conditions in advance are more reliable than discretionary judgment during fast-moving earnings cycles.

Hyperscaler Earnings Risk Heading Into Q2

Hyperscaler earnings risk is particularly acute in the near term. With CapEx guidance being raised — not lowered — and with equity analysts watching monetization metrics closely, Q2 earnings reports carry elevated binary risk for portfolios concentrated in these names.

The pattern to watch is straightforward:

CapEx guidance rises → FCF expectations fall → multiple compression risk increases

Revenue growth disappoints relative to CapEx → monetization gap widens → credit spread pressure follows

Equity dilution is announced → EPS estimates revised downward → shareholder dilution compounds multiple risk

Each of these scenarios is plausible given what has already been disclosed publicly. Advisors who have not stress-tested their hyperscaler exposure for Q2 earnings are carrying unquantified tail risk — a dynamic that mirrors the liquidity pressure we outlined in our analysis of rising bond yields in Asia and its knock-on effects for US equity markets.

Conclusion

Hyperscaler spending and portfolio risk are no longer separable topics. The $725 billion AI CapEx buildout of 2026 is reshaping the capital structure, earnings profile, and risk dynamics of the largest positions in most institutional portfolios. Big tech CapEx 2026 has introduced AI infrastructure investment risk at a scale that passive exposure alone cannot manage. For RIAs and portfolio managers, the path forward runs through systematic frameworks — not reactive discretion — and through diversified income sources that reduce dependence on mega-cap tech cash flows, as we explored in our guide to alternative income strategies.

Automate Your CapEx Risk Thesis With Surmount Wealth

Identifying the risk in hyperscaler spending is one thing. Building a disciplined, automated response to it is another — and that is exactly what Surmount Wealth is built for.

Surmount Wealth is an AI-driven automated investing platform that allows professional advisors and self-directed investors to create, backtest, and fully automate institutional-grade strategies directly on top of existing brokerage accounts. No fund transfers. No coding required.

Consider a hypothetical strategy we call the "Hyperscaler CapEx Pressure Monitor" (illustrative concept only — not a live strategy or investment advice): a rules-based allocation model that tracks CapEx-to-Revenue ratios, FCF yield compression signals, and earnings guidance revisions across the four major hyperscalers. When the model detects rising capital intensity without corresponding revenue acceleration, it automatically rotates exposure toward AI infrastructure beneficiaries — energy, industrials, and logistics — and away from the architects. When monetization signals improve, it scales back in. No hesitation. No second-guessing. Just thesis execution.

Here is why leading advisors are bringing their macro theses to Surmount:

Automate any thesis: Turn CapEx signals, FCF thresholds, and earnings triggers into rule-based entry and exit conditions — no spreadsheets required

Prebuilt institutional strategies: Access a library of data-driven models ready for immediate deployment across brokerage accounts

Full customization and control: Unlike black-box robo-advisors, Surmount gives you the logic — the platform handles the execution 24/7

Broker-agnostic integration: Connect seamlessly to Interactive Brokers, Alpaca, and other supported brokers without complex account transfers

Backtesting built in: Validate your strategy against historical data before committing capital — institutional rigor without institutional overhead

Stop letting your best research sit idle in a model. Put it to work.

👉 Book a Demo with Surmount Wealth Today and see how automation can turn your CapEx risk thesis into a systematic, scalable edge.

FAQ: Hyperscaler Spending and Portfolio Risk

What is hyperscaler spending in 2026?

The four major hyperscalers — Amazon, Microsoft, Alphabet, and Meta — are collectively on track to spend approximately $725 billion on AI infrastructure in 2026, up 77% from the prior year.

How does big tech CapEx create portfolio risk?

When capital expenditure outpaces revenue growth and free cash flow, it compresses FCF yields, pressures earnings multiples, and can trigger shareholder dilution — all of which affect portfolios with concentrated mega-cap tech exposure.

What is AI infrastructure investment risk?

It is the possibility that hyperscaler CapEx commitments will not generate proportional returns on invested capital, creating a monetization gap that current equity valuations have not yet priced in.

How should RIAs position for hyperscaler earnings risk?

Stress-test FCF assumptions, reduce unhedged concentration in passive tech indices, and consider rotating toward AI infrastructure beneficiaries using systematic, rules-based rebalancing frameworks.

Does shareholder dilution affect big tech valuations?

Yes. Equity issuance to fund CapEx reduces earnings per share and return on equity, shifting these companies from capital-light compounders to capital-intensive operators — a profile change that typically warrants multiple compression.