Blog

NAND Cycle Investing: Separating Hype from Reality

NAND cycle investing has become one of the most debated topics in professional portfolio management. As AI infrastructure spending accelerates, memory chip suppliers have posted earnings that would have seemed impossible just a few quarters ago. Gross margins have surged. Valuations have re-rated. And institutional capital has followed.

But for portfolio managers and RIAs, the critical question is not whether the current cycle is real. It is whether it is permanent.

What NAND Cycle Investing Actually Means

NAND flash memory is not a platform business. It does not benefit from network effects, switching costs, or proprietary architecture lock-in. It is a commodity memory business that sells storage capacity — measured in exabytes — at prices determined by industry supply and demand dynamics.

That context matters enormously when evaluating current valuations.

Why NAND Is a Commodity Memory Business First

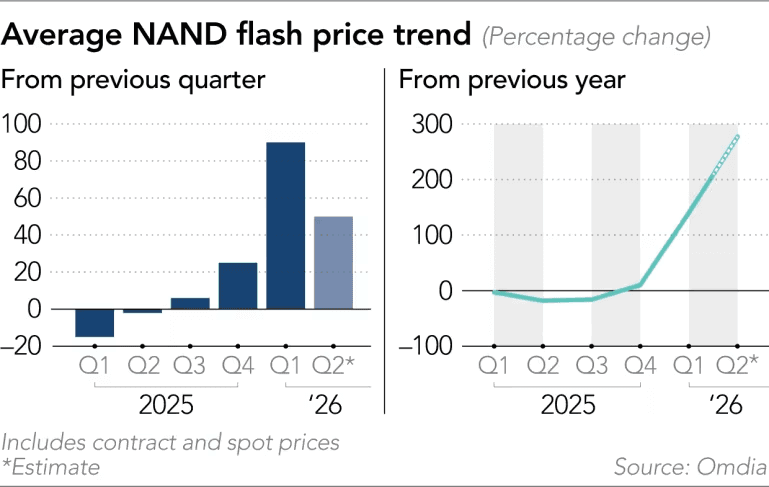

The commodity memory investing framework starts with a simple observation: in NAND markets, margin expansion is almost always a function of pricing power, not operational leverage. When supply is tight and demand is strong, average selling prices per gigabyte rise sharply — and margins follow. When supply normalizes, the process reverses.

This is not a flaw in the business model. It is the business model. As Damodaran's sector margin database consistently shows, hardware businesses revert toward normalized margins once pricing cycles turn.

How the NAND Flash Cycle Creates Profit Illusions

The NAND flash cycle has a well-documented pattern:

Undersupply phase: ASPs rise, margins expand dramatically, earnings surprise to the upside

Peak phase: Capital pours in, capacity expansions are announced, demand elasticity begins appearing in non-hyperscale segments

Normalization phase: Supply catches up, pricing softens, margins compress toward historical averages

The danger for investors is that peak-cycle earnings are often mistaken for structural earnings power — especially when a compelling demand narrative, like AI infrastructure, is layered on top.

Reading the Signals — What the Data Is Telling Us

Experienced portfolio managers know to look past headline revenue growth and focus on the signals that indicate where the cycle actually stands.

Peak Gross Margin as a Late-Cycle Warning

Peak gross margin is one of the most reliable late-cycle indicators in commodity semiconductor investing. When a NAND supplier reports gross margins approaching 80% — levels far above any normalized historical range — the question is not whether to celebrate the result. It is how long it can be sustained.

Margin expansion driven primarily by favorable industry pricing, rather than proprietary platform advantages or architectural differentiation, is inherently cyclical. Valuing a commodity memory business at software-like multiples on peak-cycle gross margins represents a significant category error. This dynamic compounds the broader valuation pressure we outlined in our analysis of the equity risk premium in 2026, where compressed earnings yields leave little margin of safety across the broader technology sector.

NAND Oversupply Risk Is Already in the Demand Data

NAND oversupply risk is not a future forecast. Early indicators are already visible. According to TrendForce's latest NAND flash market research, early warning signs include:

PC and smartphone vendors are reducing product capacities specifically to curb NAND demand

Retail, memory card, and USB drive demand is contracting under pricing pressure

High returns are attracting meaningful new capital expenditure from major producers

This is classic late-cycle commodity behavior. Non-hyperscale buyers — representing roughly 40–50% of total demand — are already responding to elevated prices. For portfolio managers who incorporate leading macro indicators into their process, these demand signals function similarly to the early-warning metrics we covered in our recession indicators framework — visible well before the headline data catches up.

Cyclical vs Structural Earnings — The Core Distinction

The most important analytical distinction in NAND cycle investing is the difference between cyclical and structural earnings. Getting this wrong is how portfolio managers end up holding peak-cycle positions at trough-cycle valuations.

Why Scarcity Is Not the Same as a Moat

Scarcity can generate extraordinary profits. But in semiconductor markets, scarcity rarely translates into permanent profitability unless protected by structural barriers competitors cannot easily replicate.

A genuine moat in memory semiconductors looks like:

Qualification intensity: products deeply embedded in customer hardware roadmaps

Physical constraints: advanced packaging or manufacturing processes difficult to replicate

Consolidated oligopoly: structural supply discipline maintained across a small number of players

Standard NAND flash does not meet these criteria cleanly. Supply discipline in NAND is more a function of capital spending timing than structural market design. As NBER research on commodity price cycles consistently shows, high returns attract supply — and supply eventually clears the premium.

AI Hardware Cycle Hype vs. Defensible Earnings Power

The AI hardware cycle has created a powerful narrative overlay on top of commodity memory economics. Selling into AI infrastructure is real and meaningful. But it does not automatically elevate a commodity supplier into a structurally advantaged franchise.

The distinction matters for semiconductor cycle risk assessment:

High-bandwidth memory tied to GPU architecture has genuine qualification barriers

Standard NAND sold into data centers benefits from AI demand but remains subject to standard commodity pricing dynamics

Long-term supply agreements improve revenue visibility but do not eliminate the underlying economics of contract renegotiation

This dynamic compounds the broader concentration risk we outlined in our analysis of the S&P 500 concentration bubble — where passive capital flows have continued to amplify exposure to the same handful of AI-adjacent names.

How Portfolio Managers Should Approach Memory Chip Valuation

Sound memory chip valuation in a peak-cycle environment requires normalizing earnings through the cycle rather than capitalizing current margins as permanent. The CFA Institute's research on earnings normalization in cyclical industries provides a well-established framework. A disciplined process includes:

Identify normalized gross margin: What has this business earned through a full cycle, excluding peak-cycle pricing anomalies?

Stress-test revenue assumptions: What does revenue look like if ASPs revert toward historical averages?

Apply a cycle-appropriate multiple: Peak-cycle earnings deserve a discount to normalized earnings multiples, not a premium

Monitor demand elasticity signals: Non-hyperscale buyer behavior often leads the cycle turn by several quarters

Applying this framework to current NAND valuations reveals meaningful downside in scenarios where gross margins normalize — even in a structurally more favorable demand environment driven by AI storage growth. As we examined in our piece on rising bond yields in Asia, a significant share of global memory chip production is concentrated in a single region, adding macro fragility on top of cyclical pricing risk.

Conclusion

NAND cycle investing rewards discipline over narrative. The current environment — elevated margins, AI demand tailwinds, long-term supply agreements — is genuinely better than prior cycles. But better does not mean permanent. Portfolio managers who treat peak gross margin as a new baseline, rather than a cyclical high-water mark, are taking on valuation risk that the current price does not adequately compensate.

Separating cyclical earnings from structural earnings power is not a bearish exercise. It is the foundation of sound semiconductor cycle risk management — and the difference between capturing a cycle and being trapped by one.

Automate Your Semiconductor Thesis With Surmount Wealth

Understanding the NAND cycle is one thing. Acting on it systematically — without emotional override, execution lag, or inconsistent implementation across client accounts — is another challenge entirely.

That is exactly what Surmount Wealth is built for. Surmount's platform allows portfolio managers and RIAs to build, backtest, and deploy fully automated, rules-based trade strategies — either from a library of prebuilt models or configured from scratch around any investment thesis.

Hypothetical Strategy Illustration: The NAND Cycle Monitor

The following is a hypothetical strategy concept for illustrative purposes only. It does not represent an existing Surmount product and is not investment advice.

Imagine a strategy built around exactly the dynamics discussed in this post — call it the NAND Cycle Monitor. The strategy tracks a rules-based set of cycle indicators:

Gross margin thresholds: When reported NAND gross margins breach a defined ceiling (e.g., 75%), the model flags peak-cycle risk and begins reducing long exposure in commodity memory names

Demand elasticity signals: When non-hyperscale demand data shows contraction, the model accelerates the rotation into defensive or short-duration positions

Supply response triggers: When major producers announce capex expansions above a defined threshold, the model initiates a systematic de-risking sequence

Normalization re-entry: As margins compress toward historical averages and valuations reset, the model scales back into memory exposure systematically

Why Leading Advisors Are Choosing Surmount:

Automate any thesis: Turn cycle signals into live, rules-based strategies without writing a single line of code

Prebuilt strategy library: Deploy proven institutional models immediately across client accounts

Full customization: You define the logic; Surmount handles the execution 24/7

Broker-agnostic: Connects seamlessly to existing accounts including Interactive Brokers and Alpaca

No fund transfers required: Strategies run directly on your existing brokerage infrastructure

Don't let your best research sit in a report. Turn it into a live strategy.

Book a Demo with Surmount Wealth →

FAQ: NAND Cycle Investing

What is NAND cycle investing?

NAND cycle investing is the practice of positioning around the boom-bust pricing dynamics of NAND flash memory markets, accounting for supply, demand, and margin normalization across the cycle.

How does the NAND flash cycle affect margins?

During undersupply phases, average selling prices per gigabyte rise sharply, pushing gross margins well above normalized levels. When supply catches up, margins compress back toward historical averages.

Is AI demand enough to sustain peak gross margin?

Not necessarily. AI-driven hyperscaler demand supports pricing but does not eliminate commodity memory economics. Non-hyperscale demand destruction and supply response remain powerful normalizing forces.

What signals indicate NAND oversupply risk?

Early warning signs include non-hyperscale buyers reducing product capacities, retail memory demand contracting under pricing pressure, and major producers announcing significant capex expansions.

How should advisors normalize memory chip valuation?

Apply a through-cycle gross margin assumption rather than capitalizing peak earnings. Stress-test revenue against historical ASP ranges and apply a cycle-appropriate multiple to avoid overpaying at the top.