Blog

Why Portfolio Managers Need Systematic Sell Signals

Most professional investment processes are asymmetric. Entry decisions pass through screens, committee reviews, valuation models, and position-sizing frameworks. Exit decisions, by contrast, often come down to a conversation — a gut call made under pressure, long after the original thesis stopped applying. This asymmetry is where systematic sell signals earn their place in a professional workflow.

The Exit Discipline Gap in Professional Portfolios

Ask a portfolio manager to defend a new position and you'll get a documented thesis. Ask why a deteriorating holding is still in the book and the answers get softer: “We're waiting for the next print.” “It's already down so much.” “The story hasn't fully broken.”

The gap isn't a competence problem — it's a process problem. Buy-side workflows institutionalize entry discipline while leaving exits discretionary. The result is predictable:

Losers linger. Positions with broken theses stay in portfolios because no rule forces the question — which is why we've argued institutional investors should formally audit their worst performers on a fixed schedule.

Winners get trimmed early. Gains are harvested for psychological comfort rather than strategic reasons.

Exit timing becomes debate-driven. Every sale requires relitigating the original thesis, position by position.

Systematic sell signals close this gap by defining, in advance, the conditions under which a position no longer belongs in the portfolio.

Behavioral Bias in Selling: Why Discretion Fails on the Way Out

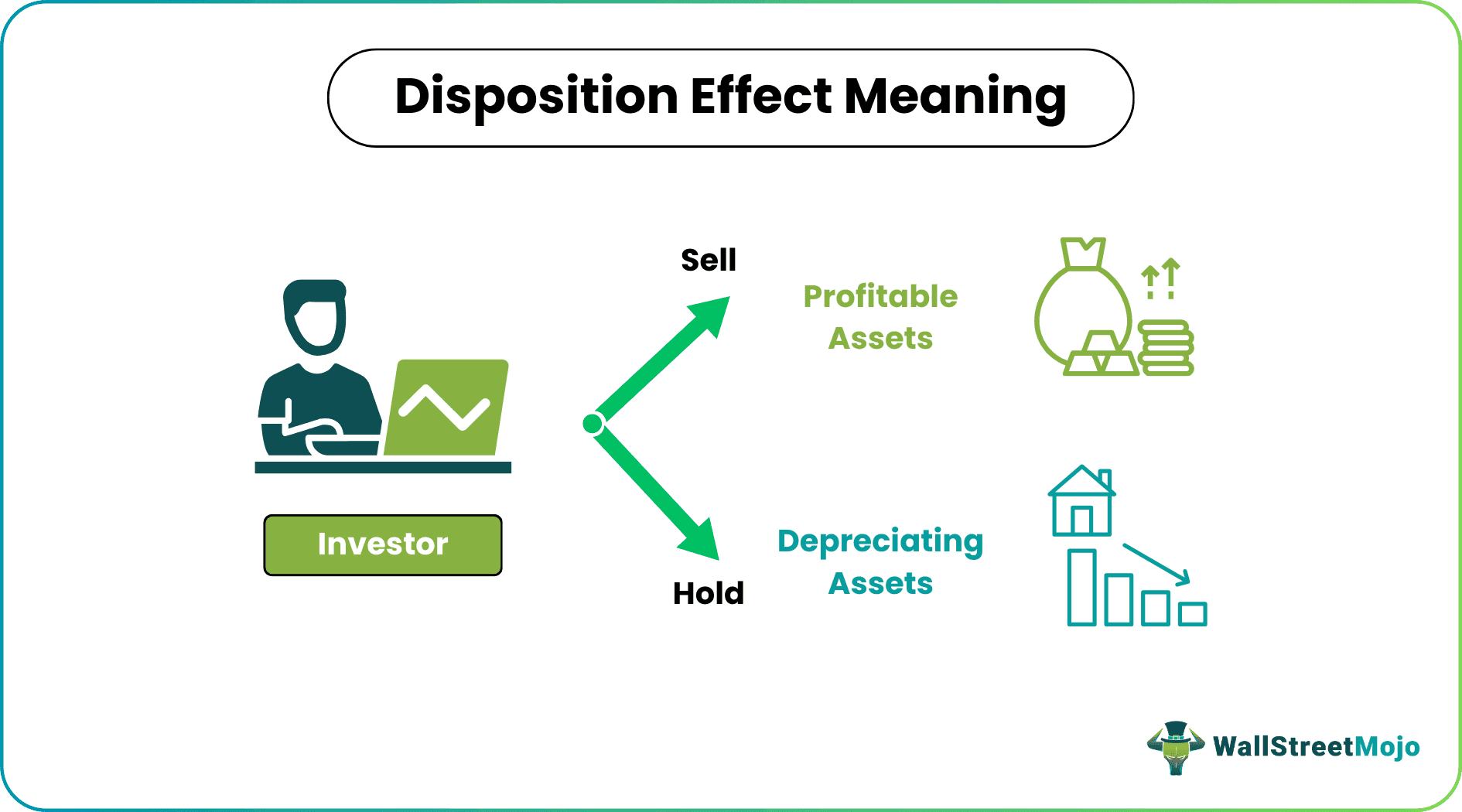

The Disposition Effect and Loss Aversion

The behavioral finance literature has documented for decades that investors — including professionals — systematically sell winners too early and hold losers too long. This disposition effect stems from loss aversion: realizing a loss feels like an admission, so the decision gets deferred.

Behavioral bias in selling isn't an amateur flaw that professionals outgrow; it's a structural feature of discretionary decision-making that survives experience, credentials, and committee oversight.

Why Deteriorating Positions Get a Pass

Discretionary exits fail for reasons beyond loss aversion:

Narrative attachment. The manager who wrote the original thesis is rarely the most objective judge of its death.

Sunk cost creep. Time and reputation invested in a position raise the psychological price of selling.

Asymmetric scrutiny. New buys face investment committees; stale holds face no one.

These pressures compound under client scrutiny — a dynamic we unpacked in our framework on recency bias in portfolio management. A codified exit rule removes the position-by-position negotiation entirely. The rule decided months ago; the manager merely executes.

Corporate Action Signals: When the Company Tells You First

Some of the most reliable exit triggers don't come from price charts — they come from the company's own filings, the same disclosures where earnings quality analysis separates durable results from consensus-beat theater. Corporate action signals often telegraph distress before the narrative catches up:

Reverse stock splits executed to maintain listing compliance, rather than for strategic uplisting, historically cluster among companies in structural decline.

Repeated dilution following reverse splits — the split-dilute-split cycle — signals a business funding operations through its own shareholders.

Authorized share increases without corresponding capital plans frequently precede that dilution.

Reading Distress in Reverse Splits and Dilution Patterns

The professional error isn't ignorance of these patterns — most managers know them. The error is treating each occurrence as a fresh debate.

When a compliance-driven reverse split lands in a portfolio holding, the question shouldn't be “is this one different?” It should already be answered by a rule written before emotions and client optics entered the room. That's the difference between knowing a signal and systematizing it.

Rules-Based Selling: Building an Exit Strategy for Portfolio Managers

An exit strategy for portfolio managers should meet the same evidentiary standard as any entry model. Rules-based selling starts with a framework:

Define the trigger objectively. “Deteriorating fundamentals” is a debate; “compliance-driven reverse split announcement” is a rule.

Validate against full datasets. Delisted and acquired companies must be included — testing exit signals only on surviving stocks builds survivorship bias directly into the conclusion.

Establish base rates, not anecdotes. Every heuristic has memorable exceptions. The question is whether the odds justify the rule across hundreds of occurrences.

Pre-commit the response. Full exit, staged reduction, or watchlist demotion — decided in advance, not at the moment of stress.

Review the rule, not the position. Periodic evaluation happens at the framework level, insulating individual exits from narrative pressure.

This is where most heuristics circulating in market commentary fall short: they're asserted, not tested — a gap we examined in detail in our two-stage momentum exit strategy framework, where academic exit models routinely break down against live execution realities. Professional adoption of systematic sell signals requires the testing infrastructure to separate folklore from validated edge.

From Framework to Execution: Automated Exit Rules

A validated rule that requires a human to notice the trigger, overcome hesitation, and place the trade is only half a system. Automated exit rules close the loop — monitoring positions continuously, detecting trigger conditions, and executing without the delay that discretion reintroduces, the same always-on posture we recommend for macro recession indicators. The behavioral research is clear that the moment of execution is precisely where discipline breaks down. Automation makes the rule self-enforcing.

Conclusion

The sell side of portfolio management remains the least systematized part of most professional workflows — and the most behaviorally compromised. Systematic sell signals convert exit decisions from recurring debates into pre-committed rules: objectively defined, validated against complete datasets, and executed without hesitation. Managers who codify their exits don't just avoid the dilution spirals and slow-motion thesis failures that discretion tolerates. They free their attention for the work that actually benefits from judgment.

Automate Your Exit Discipline with Surmount Wealth

Surmount Wealth gives advisors and portfolio managers the infrastructure to turn exit rules into executing strategies — no coding, no fund transfers, no manual monitoring.

Prebuilt strategy library built on institutional-grade, rules-based logic

Custom strategy creation to codify any thesis — including the exit frameworks discussed above

Backtesting tools to validate signals before capital is at risk

Automated execution directly within existing brokerage accounts

Hypothetical Strategy Illustration: The “Exit Trigger Monitor”. Imagine a strategy that continuously scans holdings for pre-defined distress signals — compliance-driven reverse splits, dilution filings, authorized share increases — then executes staged exits automatically the moment a trigger fires. No hesitation, no relitigating, no behavioral drag. (This is a hypothetical illustration for educational purposes only. It does not represent an existing Surmount product and is not investment advice.)

Your entry process is systematic. Your exits should be too.

► Book a Demo with Surmount Wealth Now

FAQ: Systematic Sell Signals

What are systematic sell signals?

Systematic sell signals are pre-defined, rules-based conditions that trigger a position exit — such as a compliance-driven reverse split or a valuation threshold — removing discretionary judgment from the sell decision.

Why do discretionary exits underperform?

Behavioral bias in selling — chiefly the disposition effect — causes managers to hold losers too long and trim winners too early. Rules-based selling removes that hesitation entirely.

How do corporate action signals work?

Corporate action signals use company filings — reverse splits, dilution events, authorized share increases — as objective exit triggers that often telegraph distress before price action confirms it.

When should portfolio managers automate exits?

Once an exit rule is validated against full datasets — including delisted companies — automated exit rules ensure it executes instantly, without the behavioral drag of manual implementation.

What makes a sell rule valid?

A valid rule is objectively defined, tested against survivorship-bias-free data, supported by base rates rather than anecdotes, and paired with a pre-committed response.

Related

Get Started

Experience the full power of our SaaS platform with a risk-free trial. Join countless businesses who have already transformed their operations. No credit card required.

FAQs

How can this impact my business?

How long does an this take to implement?

Will we need to make changes in our teams?

Still have a question?

Get in touch with our team.