Blog

AI Token Economics Investing: What Advisors Must Know

For most of the past decade, enterprise software was one of the most defensible investment categories available to portfolio managers. High gross margins, predictable recurring revenue, and sticky customer relationships made the sector a reliable compounder. That era is being fundamentally stress-tested. AI token economics investing has moved from a niche technical discussion to a central concern for anyone modeling enterprise software positions today. Understanding what is changing — and why it matters for valuation — is no longer optional for serious allocators.

Why AI Token Costs Are Disrupting Software Valuations

The disruption is structural, not cyclical. Historically, enterprise software companies operated with gross margins consistently above 70%, often approaching 80% or higher, because their primary cost was software development — a largely fixed expense that did not scale linearly with revenue. That cost structure is changing.

As software companies integrate large language models and AI agents into their platforms, they are transitioning from software providers into consumers of AI inference capacity. Every query processed, every agent action executed, every automated workflow completed now carries a token cost. That cost hits the income statement directly as cost of goods sold.

The Shift from Seat-Based to Consumption-Based Pricing Model

For two decades, enterprise software was priced per seat. A company with ten thousand employees paid for ten thousand licenses. Revenue was predictable, churn was manageable, and gross margin was structurally protected. The consumption-based pricing model now emerging disrupts all three of those dynamics simultaneously.

Under consumption-based pricing, revenue scales with usage rather than headcount. That introduces variability on both sides of the ledger — revenue can accelerate meaningfully if adoption deepens, but costs scale in tandem. The net effect on margins depends entirely on how efficiently a vendor can procure and deploy inference capacity relative to what it charges customers. For many incumbent SaaS vendors, that equation has not been fully modeled by the market.

How AI Cost Per Token Is Rewriting Enterprise Software COGS

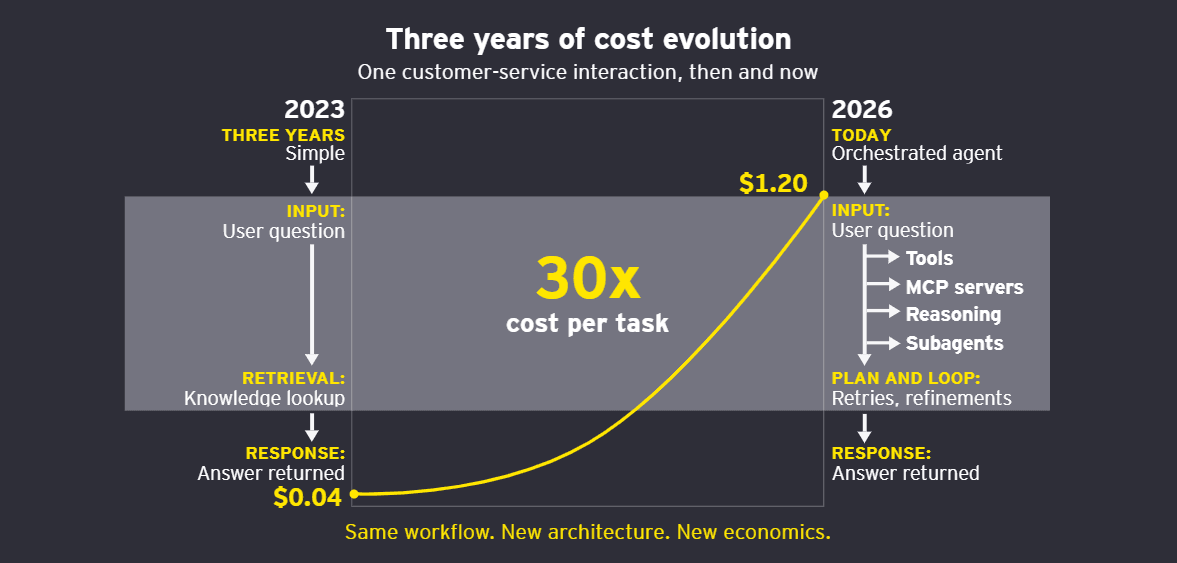

The AI cost per token is the unit of economic analysis that most equity research has been slow to incorporate. Token costs vary meaningfully across model providers and deployment architectures. Vendors running their own fine-tuned models may have structural cost advantages over those routing through third-party APIs at market rates. The implication for portfolio managers is significant: two companies reporting identical gross margin figures today may have very different gross margin trajectories over the next three years, depending entirely on their token cost exposure and pricing power.

Recent commentary from major technology firms has confirmed that token consumption at enterprise scale is more expensive than initial projections suggested — in some cases materially so. This is beginning to surface in enterprise software COGS lines and has direct implications for how software multiples should be underwritten going forward. As we explored in our analysis of S&P 500 concentration risk, the technology sector’s outsized index weight makes margin compression in software a portfolio-level concern, not just a sector one.

SaaS Margin Compression: What the Numbers Are Telling Us

SaaS margin compression is no longer a tail risk scenario — it is appearing in reported figures. The traditional SaaS Rule of 40, which rewarded companies where the sum of revenue growth and free cash flow margin exceeded 40%, is being recalibrated. Inference costs are pulling gross margins down from the 80% range toward a new floor that some analysts are modeling closer to 65–70% for AI-integrated platforms.

Gross Margin Pressure Software Investors Can No Longer Ignore

The gross margin pressure facing software investors is most acute among companies that have aggressively positioned AI as their growth driver without fully demonstrating the unit economics. Investors who underwrite these positions on historical gross margin assumptions are carrying unacknowledged risk. The relevant question is no longer what a company’s gross margin was last year — it is what the gross margin will be when AI-integrated workflows represent the majority of revenue.

This is not uniform across the sector. Companies that own proprietary data, control their own inference infrastructure, or have pricing power sufficient to pass token costs to customers are positioned materially differently than those competing on feature parity while absorbing inference costs at market rates. The broader implications for tech equity valuation are something we examined in our analysis of rebalancing SaaS exposure in the agentic era, where the seat-based pricing model faces its most direct structural challenge.

Given technology’s outsized index weight, margin deterioration in software does not stay contained at the sector level for long.

Rethinking Software Valuation Multiples in the Token Era

Software valuation multiples were built on a specific set of assumptions about margin durability. Price-to-sales multiples in the 10x to 20x range made sense when 80% gross margins implied substantial operating leverage as the business scaled. Those assumptions are now contingent — contingent on how successfully each vendor navigates the token cost structure embedded in their AI roadmap. As we explored in our analysis of the equity risk premium in 2026, compressed valuations leave little margin for error when a sector’s cost structure shifts unexpectedly.

Seat-Based vs Usage-Based Pricing: A Valuation Framework for Advisors

The seat-based vs usage-based pricing transition is the single most important variable in software valuation today. Seat-based models offer revenue predictability but face existential pressure as AI agents reduce the number of human seats required. Usage-based models offer TAM expansion potential but introduce revenue volatility and COGS variability that traditional DCF models are not designed to handle cleanly.

A practical framework for advisors requires modeling three scenarios for any software holding: first, a base case where the company successfully transitions to consumption-based pricing with margins stabilizing at a new, lower equilibrium; second, a bear case where token costs outpace pricing power and margins compress structurally; and third, a recovery case where inference costs decline industry-wide — a real possibility as model efficiency improves — allowing margins to partially recover. Weighting these scenarios by probability, rather than anchoring to historical margin profiles, produces a materially different valuation output. Anchoring to historical margin profiles when the cost structure has fundamentally shifted is a textbook example of the kind of recency bias we examined in our framework for advisors under client pressure — and one of the more costly analytical errors in a repricing environment.

What This Means for Portfolio Construction

AI token economics investing requires a more granular approach to software exposure than the sector-level allocations that worked in the prior decade. Not all software companies face equal token cost exposure. Not all are equally positioned to pass those costs through. And not all will succeed in expanding TAM fast enough to offset near-term margin headwinds.

Portfolio managers who treat software as a monolithic category — buying the sector on valuation dips without differentiating on COGS structure — are taking on analytical risk that is unlikely to be compensated. The enterprise software COGS analysis that was once a secondary diligence item is now central to the investment case. Layering this analysis alongside broader macro signals — the kind we outlined in our recession indicators framework — gives portfolio managers a more complete picture of where software names sit within a deteriorating demand environment.

Conclusion

The shift from seat-based software economics to token-driven consumption models is real, ongoing, and not yet fully reflected in consensus estimates across the sector. For portfolio managers, the opportunity is not to avoid enterprise software — it is to hold it more precisely, with a clearer view of which companies can sustain margins in a token-cost environment and which cannot. That distinction is where the alpha in AI token economics investing will be found over the next several years.

Automate Your AI Token Economics Thesis with Surmount Wealth

Understanding the margin dynamics of AI token economics is the analytical edge. Executing on it — systematically, without emotional interference, across every relevant position — is where most advisors fall short.

Surmount Wealth’s automated trade strategy platform was built for exactly this problem. Whether you want to deploy a prebuilt strategy or encode a fully custom thesis, Surmount gives you the infrastructure to act on your highest-conviction ideas automatically.

To illustrate the concept, consider a hypothetical strategy — the Token Margin Monitor. (Hypothetical example for illustrative purposes only; not a live strategy or investment advice.)

Signal: Tracks quarterly gross margin trends across a defined basket of AI-integrated software companies, flagging positions where COGS as a percentage of revenue expands beyond a set threshold

Action: Automatically reduces exposure to flagged positions and rotates toward software names demonstrating stable or improving token-cost efficiency

Rebalancing: Rules-based triggers execute without manual intervention, removing the hesitation gap between signal and portfolio action

Risk overlay: Position sizing caps prevent overconcentration in any single name undergoing a pricing model transition

This is one example of what is possible. Surmount’s platform supports prebuilt strategies covering a wide range of market dynamics, as well as fully custom builds for advisors with a developed thesis.

👉 Book a Demo with Surmount Wealth — and see how your software valuation framework can run on autopilot.

FAQ: AI Token Economics Investing

What is AI token economics?

AI token economics refers to the cost structure behind large language model usage, where every AI-driven action consumes tokens that carry a direct expense. For software companies, this cost flows straight into COGS and compresses gross margins.

How do token costs affect software margins?

As software vendors integrate AI into their platforms, inference costs increase COGS in ways the traditional seat-based model never did. This creates gross margin pressure that legacy valuation frameworks do not fully capture.

What is consumption-based pricing in SaaS?

Consumption-based pricing charges customers based on usage rather than per seat. It expands TAM potential but introduces revenue variability and ties vendor profitability directly to token cost efficiency.

Why are software valuation multiples being repriced?

Multiples built on 80% gross margin assumptions are no longer reliable when AI inference costs are structurally elevating COGS. Advisors need scenario-based models rather than historical margin anchors.

How should advisors position for this shift?

Differentiate software holdings by token cost exposure and pricing power. Companies with proprietary data, own inference infrastructure, or strong pass-through pricing are structurally better positioned than those absorbing token costs at market rates.